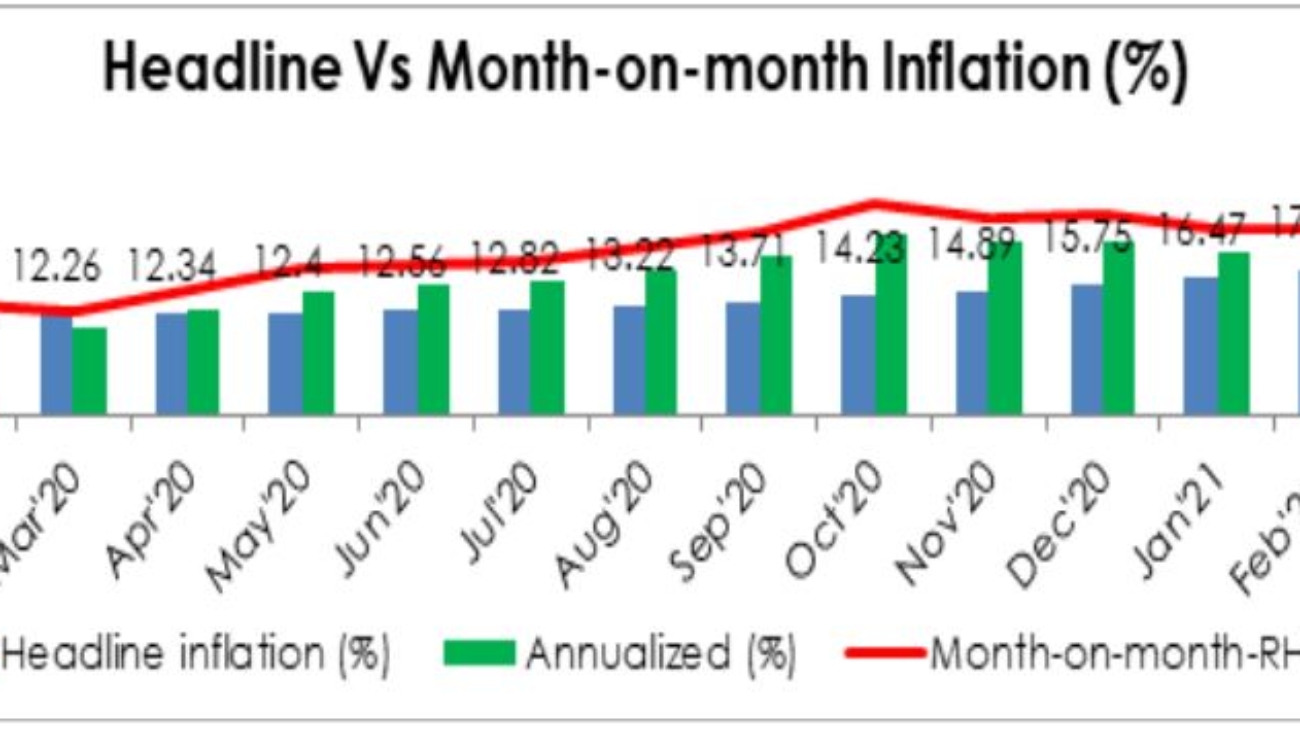

We are estimating a sharper increase in headline inflation to 17.27% for February 2021 up from 16.47% in January. If this happens, it will be the 18th consecutive monthly increase in Nigeria’s inflation rate. It will also be the highest level in 46-months.

READ ALSO: AXA Mansard empowers female business owners

Inflation is moving further away from the upper band of the CBN’s 6- 9% target. It is likely to impede output growth. Real GDP growth increased marginally by 0.11% in Q4’20 after two consecutive quarters of negative growth.

In the last two months, we have seen a divergence between the direction of month-on-month and annual inflation due to the base year effects and supply shocks. The month-on-month inflation is estimated to remain relatively flat at 1.49% (19.47% annualized) in February.

We have also seen the impact of high- powered money and the massive borrowing of the FGN via the CBN. The impact of the crowding out of private investors from the public debt market by the CBN printing money is now playing out in higher price inflation.

Food and core sub-indices to increase

We expect the food and core sub-indices to move in tandem with the headline inflation. Food price pressures will remain the primary driver of inflation, rising to 21.98% in February. The impact of the recent blockade of food supply from the Northern states to the south-west is unlikely to reflect in the February inflation numbers.

However, the impact will be felt in the month of March. Core inflation (inflation fewer seasonalities) is also projected to cross the 12% threshold to 12.02% in February due to exchange rate pressures and higher logistics costs. The impact of higher transport fares will be more potent in March.

Inflation expectations more to the upside: Tighter monetary policy stance likely in H2’21

Expectations, which is the basis for policy formulation is more to the upside due to supply shocks emanating from the food blockade and heightened insecurity, exchange rate pass-through effect and higher energy and logistics costs.

Recently, the naira has been allowed to crawl up to N411.63/$ at the I&E window, whilst hovering around N480- N482/$ at the parallel market. This coupled with the periodic dilemma on the adjustment of PMS price will continue to increase production costs and push up commodity prices.

The persistent rise in inflation increases the chances of a tighter monetary policy stance albeit in H2’21. The CBN has indicated that it is unlikely to change its accommodative stance in the near term.

The MPC committee will continue to monitor the impact of recent policies and stimulus on economic growth while using orthodox tools to mop up liquidity and contain inflationary pressures.