IMF warns against Central Bank fiscal deficit financing

The International Monetary Fund (IMF) has warned again on Thursday that Central Banks’ continued fiscal deficit financing may backfire leading to high inflation levels and distortions in the monetary policy process.

With widening fiscal needs, and limited finance, a few sub-Saharan African countries tapped their central banks in 2020 to help fund their crisis spending, including Democratic Republic of the Congo, Ghana, Mauritius, Nigeria, South Sudan, Uganda.

The IMF foresees that some of these countries may have little choice but to look to this source of funding once again if the Covid-19 pandemic persists.

It, therefore, warns that “Direct central bank lending to the government may jeopardise the former’s long-term effectiveness and undermine its commitment to contain inflation, with potential longer-term costs for the most vulnerable segments of the population.

“Countries should use such financing only as a last resort, and if used, it should be on market terms, time-limited, and with an explicit repayment plan over the medium term. Repeated monetization would de-anchor inflation expectations and add to pressure on the currency,” the fund noted in its 2021 Regional Economic Outlook for Sub-Saharan Africa.

Explaining further in a mailed note to BusinessDay, Abebe Aemro Selassie, Director of the IMF’s African Department who addressed a press conference on Thursday to discuss the report noted that “their assessment suggests that there are alternatives, and possibly cheaper, forms of financing beyond the Central Bank, including from the domestic financial market.

“Going forward, it would be essential to keep enhancing domestic revenue mobilisation, which should be accompanied by further improvement of public finance management practices—so that financing needs will be predictable and appropriately incorporated in the government’s debt management programs. “

The IMF is further of the view that Nigeria’s economic rebound would depend on bold steps to mobilise the desperately needed domestic revenues, reforms in the energy sector, as well as policies to create liquidity in the foreign exchange markets.

Nigeria’s economy contracted by 1.92 percent in 2020 and according to the IMF, is expected to grow by 2.5 percent in 2021—boosted by higher oil values and production and a broad-based recovery in the non-oil sectors.

During the virtual press conference, Selassie painted the gloomy picture of a slow and fragile recovery for economies in the SSA region and was cautiously optimistic for Nigeria which exited a recession with just 0.11 percent growth.

Over the medium term, the global shift to greener energy will continue to weigh on oil production – Nigeria’s largest revenue earner – while non-oil growth will likely remain sluggish if there is no determined effort to address the country’s long-standing structural weaknesses, including infrastructure and human-capital bottlenecks, and weak policies and governance, the fund noted in the report.

Responding to a BusinessDay question on reasons behind IMF ambitious 2.5 percent growth projection for Nigeria, Selassie explained: “We are seeing quite a lot of countries recovering this year simply by virtue of the fact that economic activities which had by design been held back through the containment measures countries needed to adopt had picked.

“It is now going to be, hopefully, provided that the pandemic continues to remain under control, economic activities should rebound and that will give stronger growth outcomes this year in many cases.

“But this is different from saying that, the fundamental drivers of growth over the medium to long term have been improved in a dramatic way allowing stronger growth, that’s a point I would stress in the case of Nigeria, really ensuring that the country enjoys and unleashes its tremendous potential requires reforms in three areas in our view.”

Selassie noted first and foremost, that Nigeria would need to create more fiscal space through domestic revenue mobilisation to pay for investments in health, education, in infrastructure which it desperately needs.

Secondly, energy sector reforms would be paramount as the cost of doing business spikes on account of the inefficiencies in the energy sector, power supply interruptions. He pointed to “the famous recourse to the use of highly inefficient, harmful generators, used up and down in the country,” adding that getting power supply, policies to make sure that Nigeria resolves this problem once and for all, is also paramount.”

Thirdly, he suggested, “macroeconomic policy calibration, including creating deep and liquid foreign exchange markets would be really important.”

Meanwhile, at 3.4 percent, and supported by improved exports and commodity prices, along with a recovery in both private consumption and investment, Sub-Saharan Africa would be the world’s slowest-growing region in 2021, with limits on access to vaccines and policy space holding back the near-term recovery, according to the fund.

Per capita output is not expected to return to 2019 levels until after 2022—and in many countries, per capita incomes would not return to pre-crisis levels before 2025.

The IMF is concerned that while recovery in advanced economies would be driven largely by the extraordinary level of policy support, including trillions in fiscal stimulus and continued accommodation by central banks, this is generally not an option for countries in sub-Saharan Africa.

“If anything, most entered the second wave with depleted fiscal and monetary buffers. In this context, and despite a more buoyant external environment, sub-Saharan Africa will be the world’s slowest-growing region in 2021.”

“Looking ahead, the region will grow by 3.4 percent in 2021, up from 3.1 percent projected in October, and supported by improved exports and commodity prices, along with a recovery in both private consumption and investment,” it noted in the report.

Other key uncertainties include the availability of external finance, political instability, and the return of climate-related shocks, such as floods or droughts. More positively, an accelerated vaccine rollout—or a swift, cooperative, and equitable global distribution—could boost the region’s near-term prospects.

IMF suggests that the first priority is still to save lives. “This will require added spending, not only to strengthen local health systems and containment efforts but also to ensure that the logistical and administrative prerequisites for a vaccine rollout are in place.

The next priority is to do whatever is possible to support the economy, however, this would require restoring the health of public balance sheets.

Going forward, the general challenge for policymakers would be to create more fiscal space, through domestic revenue mobilization, prioritisation and efficiency gains on spending, or perhaps debt management.

The fund estimates that to recover ground lost during the crisis, sub-Saharan Africa’s low-income countries face additional external funding needs of $245 billion over 2021–25, to help strengthen the pandemic response spending and accelerate income convergence.

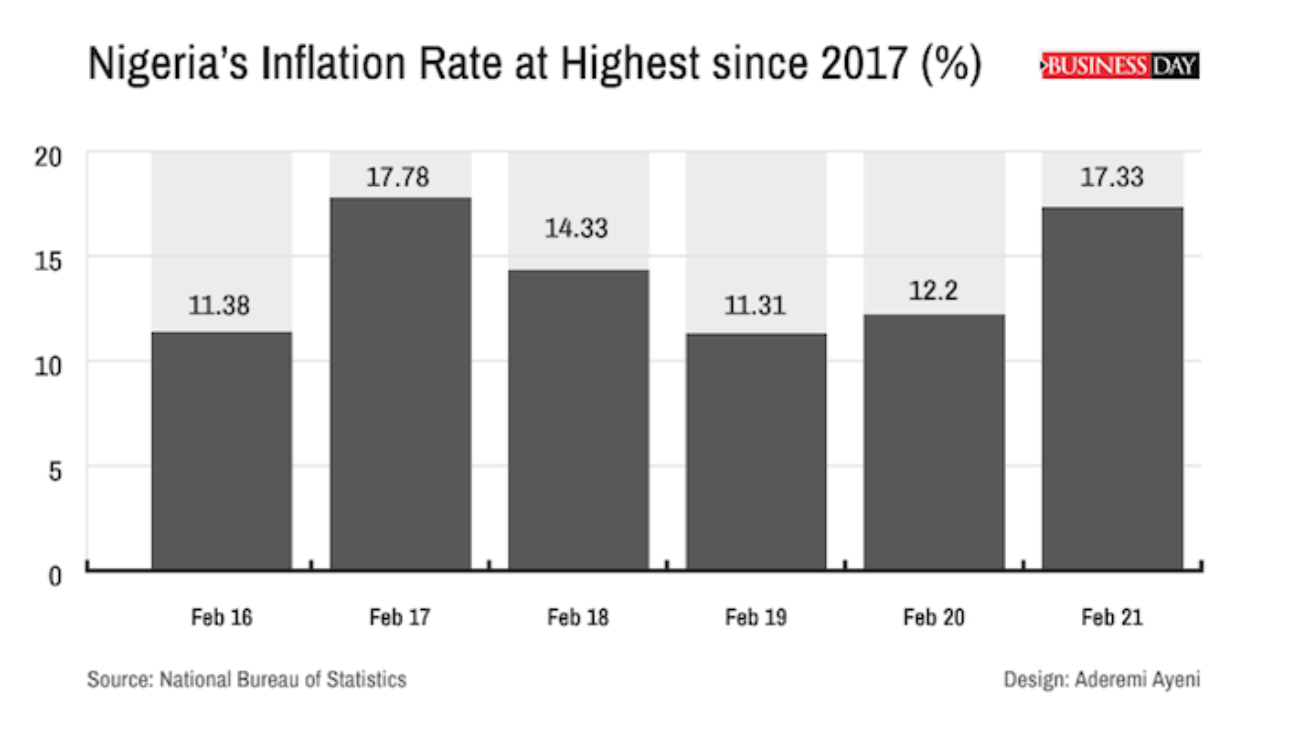

Inflation is the general rise in the prices of goods and services over time. The “inflation rate” is the rate at which the change in prices happens; this is usually expressed in percentages over time.

Alice Abegunde, a mother of three teenagers, does not understand the reason behind the constant increase in the price of rice, her children’s favourite food.

“Every time I go to the market, they have added to the price of rice,” Abegunde, 44, a resident of Lagos State, says.

While Abegunde might not be able to connect the dot and blame the rice sellers for the rise in price, Emeka Johnson could, he knew times were going to be hard as inflations numbers kept rising and resolved to save more and spend less.

What Johnson does not know is that he is constantly losing money because the value of his money drops as inflation rises.

What is inflation?

It is the general rise in the prices of goods and services over time. The “inflation rate” is the rate at which the change in prices happens; this is usually expressed in percentages over time. For instance, if inflation goes up 10 percent than last year, it means purchases will cost 10 percent more than they did last year.

Basically, inflation reduces the value or usefulness of money; the higher inflation rises, the less your money is worth, in real terms as time goes by. Therefore, it is about your purchasing power, that is, how much your money can buy.

What causes inflation?

There are reasons why prices rise. First, when everyone suddenly develops a taste for beef, the price of beef will rise. This follows a basic law in economics that, higher demand for a product will push up its price. This is also called demand-pull inflation.

What this means is that when the demand for goods and services in the economy exceeds the economy’s ability to produce them, their short supply places upward pressure on prices and gives rise to inflation.

Another reason prices rise is that the cost of producing goods and services increases. Companies would usually respond to higher cost of production by increasing the price they sell their products; they do this to cover the extra cost they incurred while producing. This is known as cost-push inflation.

How is inflation measured in Nigeria?

Every month we hear news about new inflation rate or data but have you ever wondered how it is calculated? Nigeria uses a well-known indicator called the Consumer Price Index (CPI), which measures the average change over time in prices of goods and services consumed by people every day.

In Nigeria, the CPI is calculated by the National Bureau of Statistics (NBS) and published every month. To calculate CPI, the NBS gets people to collect prices for thousands of items that an average Nigerian consumer buys such as food, prescription drugs, rent, petrol and many others. These items are grouped into categories called baskets. Every month, the NBS calculates the price changes of each item from the previous month and aggregates them to work out the rate for the CPI basket.

This was the highlight of the second edition of Digital Identity Matters, a thought leadership webinar series for driving conversations on contemporary issues in identity tech.

The event was sponsored by VerifyMe Nigeria, a leading identity verification and Know-Your-Customer (KYC) technology company, in partnership with Tech Cabal, a future-focused publication that speaks to African innovation and technology in depth.

Panellists included: Esigie Aguele, co-Founder/CEO, VerifyMe Nigeria, Bayo Adesanya, Chief Digital Officer, AXA Mansard and Adia Sowho, Chief Executive Officer, Thrive Agric. Tunji Andrews, co-Founder, Awabah moderated the discussion.

Speaking on the theme: Why Insurance is Important for the Growth of Nigeria’s Digital Economy, Aguele disclosed that the Nigerian insurance market has a $100 billion potential and can become one of the biggest sources for internally generated revenue if properly harnessed.

He said: “Insurance penetration in Nigeria is currently at about 1%. For a population of 200 million people, we only contributed $1 billion to Gross Domestic Product (GDP) last year. South Africa, which has a third of Nigeria’s population, has a penetration of 17 percent and a GDP contribution of $50 billion. It is obvious that stakeholders must put in efforts to ensure that insurance is available to more people to grow the digital economy.

Before Okonjo Iweala, No woman has ever been elected governor in Nigeria since independence in 1960, whereas in the United States, 43 women have served or are serving as the governor of a US state and three women have served or are serving as the governor of an unincorporated US territory, underscoring Nigeria’s poor record at gender equality.

Although Ngozi Okonjo-Iweala’s win as the first woman and African director-general of the World Trade Organisation (WTO) serves as an inspiration for women, it does not translate to Nigeria making much progress on gender equality.

According to the United Nations Children’s Fund (UNICEF), gender equality means that women and men, and girls and boys, enjoy the same rights, resources, opportunities, and protections.

“While we draw up lessons and inspiration from her, I doubt that it would suddenly change our gender ranking globally because she is just one person,” said Motunrayo Alaka, executive director at Wole Soyinka Centre for Investigative Journalism.

Alaka said that the country is doing very poorly in terms of intention to change the status quo.

According to data from a 2020 Global Gender Gap Index by the World Economic Forum (WEF), Nigeria ranked 128th out of 153 countries.

The report which measures the progress made towards gender parity also showed that out of the four indicators – economic, education, health, and political empowerment – used to benchmark the ranking, Nigeria improved in economic empowerment index, while the rest regressed.

Fabia Ogunmekan, executive secretary, Women in Successful Careers (WISCAR), said that Okonjo-Iweala’s win would inspire more women to succeed.

“I believe that we will see the ripple effect of what she has achieved in the near future, as institutions will leverage her story as a case study for how women in the workplace can achieve career longevity and success in their chosen fields of endeavour,” Ogunmekan said.

Globally, women and girls represent half of the world’s population and, therefore, also half of its potential. And it is believed that women now play a very vital role in human progress and have a significant place in society.

However, gender equality in Nigeria is constrained by cultural practices which elevate patriarchy to an absurd degree.

This is why a gender equality bill, designed to eradicate gender inequality in politics, education, and employment, has been marooned in the national assembly for close to 10 years.

“Okonjo-Iweala’s win is supposed to improve our march to gender equality but in a society like ours, it is not certain,” said Tinu Mabadeje, a nonviolence training consultant. “We just hope that this will convince our leaders that women can do as well as men if given the right opportunities.”

Prior to independence, and even before the advent of colonial rule, the role of a woman in society had significantly changed as Nigeria had an admirable array of women who had done great, inspiring deeds and even conquered territories.

Glaring examples were Margaret Ekpo, a women’s rights activist and a social mobiliser who was a pioneering female politician in the country’s First Republic and a leading member of a class of traditional Nigerian women activists, many of whom rallied women beyond notions of ethnic solidarity.

There was Funmilayo Ransome-Kuti, a teacher, political campaigner, women’s rights activist, traditional aristocrat, and the first woman to drive a car. Her political activism led to her being described as the doyen of female rights in Nigeria. She was also regarded as ‘The mother of Africa’.

In recent times, the example of Oby Ezekwesili, who served first as minister of solid minerals and later as minister of education under the Obasanjo presidency, is instructive. Ezekwesili also served as the vice-president of the World Bank’s Africa division from May 2007-May 2012 and was a 2018 nominee for the Nobel Peace Prize.

Non-profits are borne out of the need to impact society, which like any other venture requires a well-established system of consistent funding. However, for smaller ones despite the promise of genuine impact, they face a plethora of challenges ranging from lack of structure, inexperience, and financial mismanagement. Here are some ways small non-profit leaders can improve their funding efforts.

Define Core Objectives: We are living in an unprecedented time, so why should anyone want to give to your organization? An important thing to do before soliciting external help is to do an honest appraisal by examining the objectives and needs of your organization. Why are you pursuing this cause? Who will benefit from it? What is your budget? What are your needs? When do you need resources? Having answers to these questions helps you put things in perspective. You will know who your potential supporters are and be able to start the conversations that will create an emotional connection. While on this, be sure to pay attention to their needs and how your organization can help meet them. Understand their priorities. Communicate your good works and never forget to express gratitude. Your sponsors should know how their help has allowed your organization to accomplish its mission.

Set up a team: Smaller non-profits do not have the luxury of recruiting professionals to manage fundraising efforts, but they can capitalize on the shared passion of like-minded volunteers who have some experience and will donate their skills and time. By forming teams within this group, not only will they will multiply efforts through ideas, knowledge sharing and network exchange; commitment, accountability, leadership and the much-needed support for cloudy days are examples of what teamwork can yield. Delegate and assign leaders who would be responsible for key activities including planning and budgeting, donor and sponsor engagement, operations and logistics management, and other tasks that will place the organization in face of the right audience through marketing. As much as possible, non-profits leaders should engage with volunteers. While some may not have fundraising experience, they can donate other complementary skills. For instance, you would need them to put the word out there or help with event set up or even sell tickets. And even in uncertain times, studies have shown that volunteers who cannot offer their time and skill are more willing to help financially.

Leverage on social media: Social media makes it easier for grassroots organizations to access a wider audience interested in community-based projects from all parts of the world, but effective and consistent communication, publicity, and using the right tools make this happen. There are legitimate crowdfunding websites that allow many people to contribute to causes or projects that appeal to them. A popular example is GoFundMe. There’s Global Giving and Causes by Facebook. These websites can collect secure donations efficiently by collaborating with prominent payment companies. Now that transaction processing has been taken care of, small nonprofits should focus on driving the right messaging. It is also important not only for them to have an online presence, using suitable social media channels to enhance visibility while pushing appropriate content will produce user reaction from even potential donors.

Recession has in the last few years become something of a buzz word in Nigeria to describe the harsh economic conditions in the country and its resultant effect on the income, spending power and businesses of the people.

However, by definition, a recession happens when a country’s GDP falls in two consecutive quarters, while the Gross Domestic Product (GDP) simply means the measure of goods and services produced in a country over a period of time.

Last year, the economy contracted by 3.62 percent in the third quarter of 2020, indicating that two consecutive quarters of negative growth had been recorded in 2020 following the previous decline by 6.1 percent in the second quarter.

Officially, this meant that Nigeria’s economy slipped into recession and for the second time in four years as oil prices plunged in the midst of the COVID-19 pandemic.

Recessions are usually characterized by falling incomes, weakened sales and production as well as a drop in the confidence levels of investors. Consequently, this leads to an aversion for risk and often a tendency to err on the side of safety.

The interesting fact, however, remains that recessions often give way to recoveries soon after. In the light of this, with the right strategy, a recession might not necessarily be a bad time to invest.

These few tips will be useful in helping you create your personal investment strategy.

Avoid Panic One big mistake investors make in times of recession is to make panic-induced decisions and follow an inclination to liquidate investments in favour of cash. This could, however, mean that you box yourself into a “corner” which could eventually produce hefty losses once the economy begins to recover. This is especially for people who have a stock-based investment portfolio.

Also, patiently wait to get dividends for your existing investments and resist the urge to sell in panic. Carefully Inject Funds into Investments When a market is fraught with volatility and investor fear, it can be extremely difficult to time trades perfectly and properly predict when prices are likely to rise or fall.

The way to work around this is to find a personal saving pattern that works for you and then carefully identify investments that appear worthwhile to inject your saved resources into.

This can help you save money and also, significantly increases your purchasing power as prices are usually low at these times.

It may also be a good time to take advantage of low prices and get bargain deals especially in industries that have been hard hit by the recession but have clear potential to bounce back strongly.

Take a Peek In taking on new investments in this period, especially with direct investment like shares, always take a peek into the financial records as well as the business and operational models of the companies you are considering for investment.

Industries and companies that cater to basic human survival needs are a good bet in this regard because they can often expect to experience minimal upheavals even in a recession.

There is Nothing Wrong with Being Safe Investing in safety nets such as bonds and mineral resources such as gold can be a great way to store up value, as their performance is often unaffected by market forces.

This can help you diversify your portfolio properly and ensure you are not entirely reliant on how the stock market pans out. I leave you with the words of the American businessman, MichealNesmith “Behind every dark cloud, there is usually rain”.

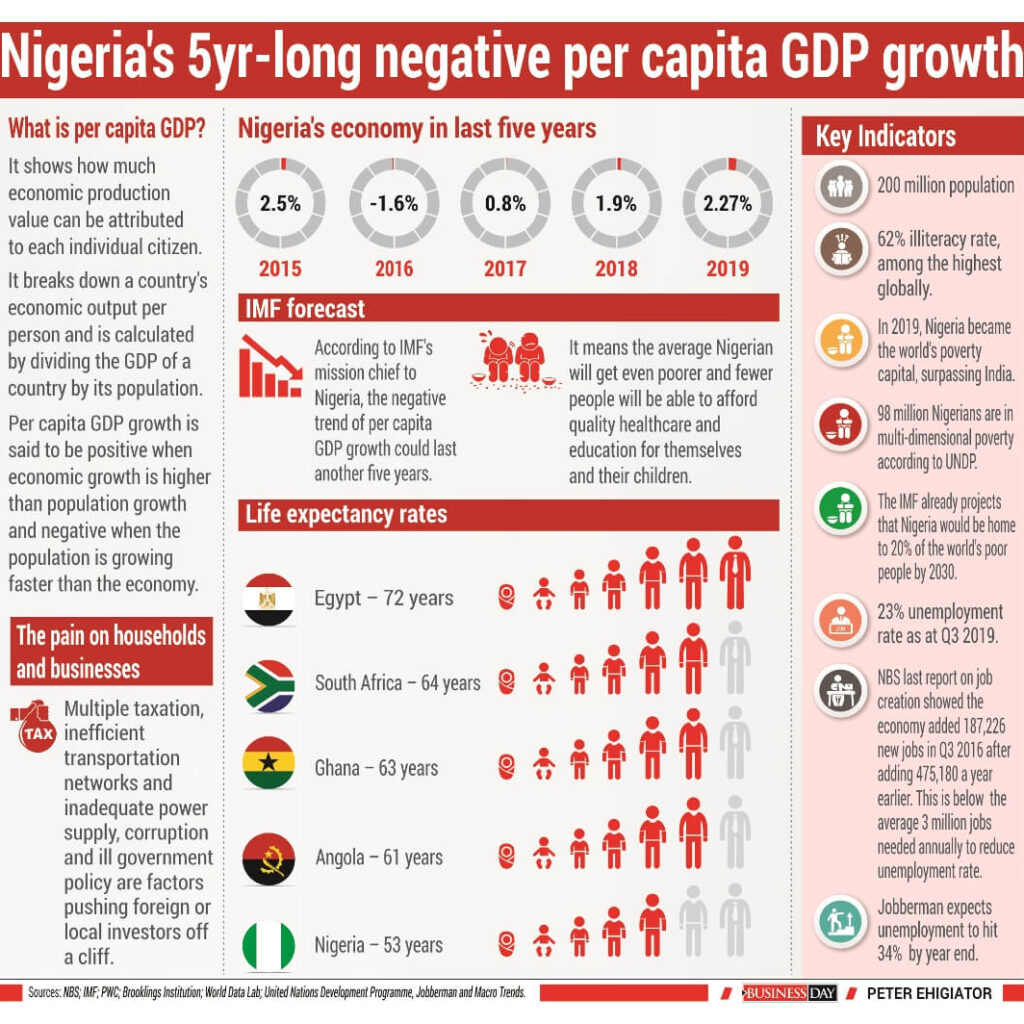

Five straight years of negative Per Capita GDP growth is unprecedented in Nigeria, at least, since the turn of democracy in 1999. But that is what has happened between 2015 and 2019.

For many Nigerians, connecting the dots between five years of an economy not expanding as fast as population is not so straightforward, not with an illiteracy rate of 62 percent, one of the highest globally.

What is unmistakeable, however, is the pain those five years of negative Per Capita GDP has wrecked on households and businesses, whether they understand what is happening or not.

Take the case of Jide Ibrahim (not real name) for example. Ibrahim’s highest qualification is a Bachelor’s degree in Human Kinetics from the Lagos State University (LASU). He worked at Woolworth, a South African clothing retailer, which closed its three stores in Nigeria in 2013.

It is been seven years and he is yet to pin down another job. His lack of job has forced some changes. He has had to move away from his two-bedroom apartment somewhere in Ikorodu to living with a friend in a one-bed apartment almost the size of a telephone booth within the same area.

When asked how he felt when he was laid off, he heaped the blame on Woolworth, saying the company unfairly asked people to leave after milking Nigeria dry.

“These foreign companies just use you and dump you,” Ibrahim said.

Little did he know that his lay off was no fault of Woolworth, but of the high cost of operating a business in Nigeria, which sucked the life out of the South African retailer and sent it scrambling back from where it came.

Hear what Woolworth’s CEO, Ian Moir, said about the exit at the time: “When an investment no longer generates viable returns, difficult decisions have to be made to contain costs.”

High rental costs and duties and complex supply chain processes made trading in Nigeria highly challenging, according to Moir.

Woolworth’s 18-month foray into Nigeria is peculiar for a company that has been operating in South Africa for decades – since 1931 in fact – and has operations in various African countries and elsewhere. The remaining 59 stores in 11 African countries were not affected by the Nigeria decision.

Since that time, Woolworth has expanded to 64 stores and is in 13 African countries.

Woolworth’s experience is not unique; several companies have had to close shop in Nigeria due to the country’s difficult business environment.

Though strides have been made to improve the business environment, the country sits at a lowly 131 of 180 countries surveyed by the World Bank.

Challenges from tax multiplicity to inefficient transportation networks and lack of adequate power have been unbearable to businesses. Over regulation and corruption in government are also chief culprits in pushing businesses, foreign or local, off the cliff.

This shows Ibrahim’s anger should be channelled towards the Nigerian government, which has failed to create an enabling environment for businesses to succeed.

On the evidence of the declining flows of FDI into the country since 2014 and tales of woes by local businesses, the government has not been able to significantly improve the business environment.

Since 2008, when Nigeria attracted a record $8 billion FDI following a wave of privatisation, the country got $3 billion on average between 2009 and 2015, and $1 billion a year since then, according to the NBS, effectively trailing smaller peers like Ghana.

Considering the size of Nigeria’s population, a billion dollars works out to $5 per head.

Foreign companies are not the only businesses to have walked out on Nigeria, even local companies have struggled.

The Manufacturers Association of Nigeria (MAN) said about 272 firms were forced out of business in 2016 alone, 50 of which were manufacturing companies, amid stifling government regulation. The manufacturers say that led to 180,000 job losses in the period.

Surely, Ibrahim and the over 20 million Nigerians without jobs, should hold the government more accountable for the damage done to their lives by bad policies. The lack of jobs has helped poverty thrive.

Nigeria, home to 87 million poor people, became the world’s poverty capital in 2019, overtaking India, according to a Brooklings Institution report.

Another set of statistics by the World Data Lab estimates that 90 million Nigerians live under $1.90 a day, while the United Nations Development Programme reported that 98 million Nigerians were in multi-dimensional poverty.

Yet the pain of a floundering economy growing slower than population also shows it is no respecter of persons. The rich have perhaps suffered just as much.

Take Aliko Dangote, Nigeria’s richest man, who doubles as the continent’s wealthiest person. Dangote is no longer worth half as much as he was in 2014.

Despite remaining the richest African for almost a decade, his fortune is down a staggering 72 percent to $7 billion from $25 billion in 2014, according to Forbes data.

What is Per Capita GDP and why is it important?

At its most basic interpretation, Per Capita GDP shows how much economic production value can be attributed to each individual citizen. It breaks down a country’s economic output per person and is calculated by dividing the GDP of a country by its population.

Per Capita GDP growth is said to be positive when economic growth is higher than population growth and negative when the population is growing faster than the economy.

The per capita metric is a popular measure of the standard of living, prosperity, and overall well-being in a country. A high Per capita GDP indicates a high standard of living while a low one indicates that a country is struggling to supply its inhabitants with everything they need.

Luxembourg, a small European country surrounded by Belgium, France and Germany, has the highest GDP per capita globally with $113,196 as at 2019, according to IMF data.

Switzerland ($83,716) and Norway ($77,975) make up the top three countries with the highest GDP per capita.

On the flip side, war-torn South Sudan ($275), Burundi ($309) and Eritrea ($342) make up countries with the lowest Per Capita GDP in the world. Nigeria ranks 138 with $2,222, behind Ghana with $2,223.

Five years of negative Per capita GDP

Nigeria’s relatively low Per Capita GDP, which paints a dim picture of the living standards in the country, has been worsened by five straight years of contraction.

The last time Nigeria had a positive Per Capita GDP was in 2014, as the economy has struggled since a lengthy collapse in global oil prices that began in mid-2014. When not contracting, the economy has grown at a tepid 2 percent rate compared to average population growth rate of 2.6 percent.

The economy grew 2.5 percent in 2015 before contracting by 1.6 percent in 2016. As oil prices recovered, the economy turned the corner on its first recession in a quarter of a century by growing 0.8 percent in 2017 and a 1.9 percent growth in 2018. In 2019, the economy grew 2.27 percent, capping five years of an economy that didn’t grow fast enough to create new opportunities for a rapidly growing population.

Make it another five years

Prior to the COVID-19 pandemic, the IMF predicted that income per head will continue falling for another three years until at least 2023.

However, with the pandemic, that forecast is grimmer. The trend of negative Per Capita GDP growth could last another five years, according to Jesmin Rahman, the International Monetary Fund’s (IMF) mission chief to Nigeria. That is worse than the initial projection.

“We are going to see the contraction in real Per Capita GDP pick up in the next five years,” Rahman says.

Rahman says it could take Nigeria at least three years before the economy grows at the modest 2 percent rate at which it expanded in 2019 prior to the COVID-19 pandemic.

Another five years of Per Capita GDP contraction is a painful squeeze for a country with gross domestic product per capita of just $2,222, meaning Nigerians will get even poorer than they are now for another five years as their incomes continue to shrink and the economy bleeds jobs.

It means more Nigerians will fall into a poverty pit. The IMF already projects that Nigeria would be home to 20 percent of the world’s poor people by 2030.

Another painful stretch of negative per capita GDP growth also means fewer people will be able to afford quality education for themselves and their children.

For instance, premium primary education alone in Lagos, Nigeria’s commercial capital, could cost anything between N700,000 ($1,944) to N1 million per annum ($2,777). That works out to an average of $2,360 (N849,600), higher than Nigeria’s per capita GDP of $2222.

Fewer people will also be able to afford quality healthcare in a country where the average life expectancy is just 53 years. Only four countries in the world have lower life expectancy rates and they are Sierra-Leone, Chad, Lesotho and Central Africa republic.

South Africa’s life expectancy is 63 years, at par with Ghana’s but lower than the World average of 70 years, according to United Nations World Population data.

Countries like Hong Kong, Japan, Singapore and have an average life expectancy of 83 years.

The job-seeker in Nigeria will also have fewer jobs to compete for with an even larger population of job seekers. Ibrahim may struggle to find a job for another five years.

Data from Jobberman, which recruits mainly white-collar employees and does not track those looking for non-skilled, blue-collar work, sees unemployment in the nation of more than 200 million soaring to 34 percent by the end of the year from 23 percent in 2019.

Other estimates suggest that the unemployment rate could hit 50 percent by 2021. The country’s unemployment rate quickened to a more than six-year high of 23 percent in 2019, the last time the NBS measured the rate.

Rising unemployment and higher inflation has meant the country’s misery index has deteriorated to be almost at par with failed countries from Syria to Lebanon.

As it stands, over 22 million employable Nigerians are out of work and another 15 million are underemployed. There’s little hope that the country can generate sufficient jobs for its people who are forecast to reach 400 million by 2050.

The last time the Nigerian Bureau of Statistics (NBS) published data on job creation it showed the economy added 187,226 new jobs in the third quarter of 2016 after adding 475,180 a year earlier.

As Nigerians get poorer over the course of the next five years, it may also mean more companies, especially small businesses, are at risk of failing as falling consumer purchasing power leads to a reduction in sales and revenues.

Though there is paucity of data on the failure rate among Nigerian start-ups, the one available estimate given by a Nigerian bank Stanbic IBTC claimed that over 80 percent of Nigerian start-ups fail within their first five years.

That will get worse if the economy continues to underperform population growth for another five years.

What experts say is the way out for sluggish economic growth

Jesmin Rahman

Rahman is IMF mission chief to Nigeria. She recommended a raft of fiscal policies that lift per capita GDP growth in Nigeria during a recent webinar hosted by the American Business Council.

Here is what she said: Nigeria has always been to me a fascinating country with huge potential; there’s nothing it doesn’t have. Nigeria has a huge population, and natural resources, yet this is a country that when you compare to its peers on social indicators and living standards, it is not where it should be.

Per capita income used to be $7,000 in mid-1980s since then it has gyrated in sync with oil prices. There are quite a few challenges Nigeria needs to tackle if this course is to be altered. At the current population growth rate of 2.6%, Nigeria’s population is projected at 400 million by 2050. The labor force is growing very rapidly much of which is getting absorbed in either the informal sector or not employed at all. Informal sector wages are very low. Basic literacy among the young population is also very low. Six of out ten out of school children are Nigerians so these are very sobering statistics.

When you look at poverty rate, it is around 40% and given the population projection, by 2030, the World Bank estimates that a fifth of the world’s poorest will be housed in Nigeria. When you add regional dimension, the situation is even scarier because you will the concentration of all of these low statistics in one part of the country.

To turn Nigeria’s population into human capital so the economy grows, Nigeria needs strong job growth and investment in social indicators; education, health and some of the very basic services.

My colleagues in the IMF did a basic estimate of how much it would cost the country to reach the SDGs and they came up with 18% of GDP which would come largely from government even though donor community would help. This reemphasises the importance of growth because without stronger growth to raise revenues, and without those revenues, it would be hard to provide for these very basic and much needed things.

The second challenge is to reduce the dependence on oil. In some ways the Nigerian economy has achieved diversification. Oil only counts for 10% of GDP and 1% of employment so you can say that’s a kind of diversification but the non-oil economy depends heavily on the oil prices through direct and indirect linkages and oil also accounts for 50% fiscal revenues and over 80% of exports. Oil is also important for FX inflows even though remittances help. Because of this, in order to have any form of meaningful diversification, Nigeria needs to move on these fronts as well: diversify fiscal revenues and exports in addition to diversifying GDP base.

Nigeria’s DNA is oil and unless diversification is seen on both fiscal and external fronts, this perception is unlikely to change and this perception needs to change if we are to avoid the big cycles.

Charles Robertson

Robertson, the global chief economist at Renaissance Capital, during a Financial Times summit as far back as 2018, said the country needs to grow by between 4-5 percent for per capita GDP to stop contracting.

“As Nigeria has grown at 2 per cent per capita since 1992, our medium-term base should be at least 4-6 per cent GDP growth,” Robertson said.

But Nigeria cannot match the 4-6 per cent per capita GDP growth of industrialising countries because adult literacy at 60 per cent is too low and electricity consumption is under half the minimum required level for sustained industrialisation, according to Robertson.

“To push headline GDP growth to 6.5-8.5 per cent would require an adult literacy campaign, a trebling of electricity consumption and a doubling of investment to GDP,” Robertson said.

John Ashbourne

Ashbourne, a senior emerging markets economist at economic consulting Capital Economics also shared the following views during the FT summit.

“The government needs to unlock private sector investment by improving the business environment and encouraging participation in the non-oil sector.

The country also desperately needs better infrastructure and reforms to the state-dominated oil sector.”

Razia Khan

Razia Khan, chief Africa economist at Standard Chartered bank also had these to say: “Nigeria has all the necessary building blocks to achieve much faster growth. With its low base, youthful population and scale, a growth rate exceeds the rate of population growth should be easily achievable.

“It needs to develop more institutions that are more resilient than tends to be the case in typical resource economies, for example a tax base independent of oil and a banking sector that can meet the borrowing needs of the private sector. Nigeria has failed to make a transition away from being an oil economy.”

Olusegun Omisakin

Omisakin is the Chief Economist and Director of Research & Development at the Nigerian Economic Summit Group (NESG). His views are as follows: “The effects of COVID-19 pandemic on global health and socio-economic conditions will remain for the foreseeable future.

“For Nigeria, economic policies have to remain broadly expansionary to hasten recovery. Implementation of the Medium-Term National Development Plans (MTNDP) and Nigerian Economic Stimulus Plan (NESP) will quicken the recovery in 2021.

“More focus should also be on improving the business environment through reforms.”

The year 2020 has seen tremendous shifts and changes in the way we work. Technology and innovation are creating new opportunities as well as challenges. For more than a decade, we’ve built a culture around the idea that work is outcomes based, not anchored to a specific place or time. While every industry and business are different, a segment of employees have shifted to remote work and businesses have had to rethink their operating models and organisational structures. Flexible working has jumped from being a pipeline goal to being part of our daily grind in a matter of a few months. As we all head to the dining table or study for yet another day ‘in the office’, remote working technologies are being put to the test in a serious way – and all businesses are impacted.

Working from home is not new. The connected office has long been a critical enabler of the modern era’s distributed workforce, bringing productivity and experience boosters. In fact, in many countries in Emerging Africa, like Nigeria, Kenya, Tanzania etc., ICT has played a big role in driving the economy forward through the rapid growth of IT investment. Remote working has been one of the partial solutions to address connectivity challenges, address the needs of millennial workers, as well as encouraging women to be part of the workforce while having flexible careers.

Today, the ability to work remotely is business critical and presents certain challenges for organisations of all sizes. But adapting to the new normal is a collaborative effort, calling for unity between the c-suite, IT departments and third-party technology experts.

The question is: are organizations ready to handle and prepare for a long-term stint of remote working across the entire workforce – and will they rise to evolving needs when it comes to keeping their business successful?

Empowering productivity: While challenging, this is also a massive opportunity for businesses to demonstrate their agility – and for those lacking agility, to prioritise it. There is no doubt that this seismic shift will test both security and infrastructure, but flexible working can boost productivity too. As the workforce settles into their home office, there are considerations that need to be made in terms of security – keeping applications safe in the data centre and protecting end-point data – supporting network traffic and enabling increased flexibility. While each business will experience these to varying degrees, every business should be carefully thinking through their value chain. It’s therefore critical for organisations to support their employees with the right connectivity and tools that are essential to drive productivity and collaboration.

Data must be protected from the end point to the data centre: By increasing the number of devices connected to the network, the challenge will be managing and processing the additional data. To completely overhaul existing current networks is unrealistic for most medium businesses, as this not only takes time but is a drain on resources. Instead, edge computing can help to process data while limiting the impact on the enterprise cloud by only sending selected data. A recent study from the consulting firm, Deloitte, showed an alarming rise in the number of cyber and ransomware attacks against individuals and organisations and is only increasing, now that the home workforce is connecting remotely to their organisations systems. For any business, cyber-attacks can be devastating as the ability to recover is curbed by a lack of resources.

Seamless, scalable remote working solutions: Thanks to software defined workspaces, employees can access the tools and apps they need on any device. This keeps the day-to-day business rolling, ensuring the playing field is levelled in terms of accessibility and updates. As businesses adjust to the all-in working from home demands, they may find that consumption and ‘as-a-service’ solutions on-premise will help – particularly with economics and the short turn-around they have been faced with. For example, “Virtual Desktop Infrastructure” (VDI) provides secure, high-performance access for critical users while the “Hybrid Cloud” can scale data center resources.

In conclusion, every organisation needs to adapt to the changing expectations of the workforce in order to thrive, and ten years out, businesses that successfully achieve digital workplace transformations will be at an advantage over businesses struggling with legacy systems, massive amounts of data and workforces unprepared for change. Ultimately, by empowering remote workforces, organisations can unlock creativity, productivity, increase job satisfaction and most importantly learn to collaborate in new and improved ways – bringing to fruition the next wave of human led, technology-underpinned progress.

The saying, ‘desperate times call for desperate measures’ isn’t new to most people, including Nigerian policymakers. But a situation where the Nigeria monetary authority, the Central Bank of Nigeria (CBN), seems to imply it has little idea of the ravaging impact of the COVID-19 pandemic on Nigerian economy, leaves a sour taste in the mouth and makes one wonder how it can put desperate measures in place.

Often times, Nigerian policymakers have enacted policies that have conflicted with the country’s reality due to their poor perception or understanding of what the true state of the economy is.

To the surprise of most economists, the CBN stated clearly in a note published on its website that it expects Nigeria’s economic growth to decline by a meagre 1.03 percent. This is at variance with the thinking among analysts, economists, international bodies and even Nigeria’s Ministry of Finance.

The International Monetary Fund (IMF) in June revised further downward to 5.4 percent their economic contraction expectation for Nigeria from 3.4 percent. Zainab Ahmed, Nigeria’s Finance Minister, projected that the country would contract between 4 to 8.9 percent.

This begs the question as to what parameters the CBN’s optimism is based. We cannot but wonder whether the CBN has opted for ‘walk by faith’ rather than ‘by sight’ in what is glaring to all.

CBN’s second quarter outlook of seems to point to an almost certain possibility that Nigeria’s economy is headed for a V-shaped recovery after plunging quarter-on-quarter by 0.64 percent to 1.87 percent in Q1 2020.

This also creates a misleading illusion of Nigeria’s resistance to the COVID-19 pandemic. Hence, the question: Is the CBN insinuating a contraction by 1.03 percent is the worst impact the pandemic has on economic activities in Nigeria?

Given that the negative effects of the pandemic was felt more in the second quarter of this year, the CBN’s outlook is, at best, a wish and not realistic as factors that will support its optimistic stance are missing.

Nigeria’s Purchasing Managers Index (PMI) which is a leading indicator providing valuable insights into the state of the Nigerian economy in general and the manufacturing sector in particular, provides a picture of what the Nigerian reality is.

The PMI reading for Q2 2020 was below 50, signifying manufacturers and non-manufacturers pessimism on the state of the economy and this signals a contraction.

It was no longer business as usual for the Nigerian manufacturing sector which contributes over $30 billion to the GDP. COVID-19 induced disruptions in business supplies, fall in household demands etc, coupled with foreign exchange scarcity, took a toll on manufacturers in the last quarter. Many had to lay off staff while some cut salaries.

Worsened by rising inflation which has caused consistent weakening in households purchasing power amid job losses, many manufacturers and non-manufacturers , especially manufacturers of non-essential commodities, will see sales drop and profit margin shrink.

Also, Nigeria risks another year of underperforming budget as price of oil is yet to recover to levels above $60 witnessed in January 2020. As a result, the FG had to cut down its revenue expectation by 36.4 percent to N5.16 trillion.

Therefore, we employ the Nigerian authorities and policy makers to remain factual and realistic when reviewing and giving outlook for the economy. We hope that this will help drive policies and actions that will suggest the level of work that must be done in line with current reality.

We believe that CBN’s outlook is unrealistic given how its FX demand management activities and reluctance to unify Nigeria’s exchange rates have stifled business operations and driven away foreign investors from our markets.

Nigeria’s journey to recovery calls for desperate measures and we urge the CBN to start this by providing clarity on Nigeria’s FX rate position and how it hopes to clear dollar-demand backlog.

We are making a mistake building walls than bridges. Beyond singing Wyclef’s Diallo; beyond screaming “I can’t breathe” in solidarity of George Floyd comes a reality. When it comes to marginalization in the 21st Century, playing Malcolm and Martin Luther King is played out. The same goes for shouting Biafra on the streets of Aba before Operation Python or screaming Aluta like Sowore as if it’s 1993 again in his Unilag prime. Mere protests around marginalization if not in your small campuses remain a temporary solution to a permanent problem. Tribes and race battles aren’t about accents and colors. Leave that for Language classes and Fine Art lessons. It’s about economics and power. If you don’t crack that code, you’re screaming in a vacuum!

Protest especially when it overstays its welcome will always be hijacked. This is same for every cycle of black protest mainly against racial profiling, xenophobia, police brutality, and inequality in the justice systems. Racism is more socio-economics. In other words, blacks in America need to step up their game. We can do much more than Ferguson Protests and Trayvon Martin’s memories. We can do more than remember slavery, complain of racism, and also begin to hate other people as we do ourselves. Beyond noise, what’s the strategy?

No one really respects you if they don’t think you have a backup

Being organised is everything. On the streets where the likes of Floyd die for an alleged 20 fake dollar bill crime, the Chinese, Indian and Italian gangs are bloodier than black gangsters (which by my view are even exaggerated in movies and Hip Hop). However, no one touches them recklessly. This is because they know that if they do, there are organised systems and people who will fight for them. It may even become an international issue as they come from a community that is powerful. This is one of the most powerful concepts. But let’s be real, there’s no real power without unity and progress. This means finance also.

You rarely can go far without a strong culture

Everybody has a culture. It is defined as a way of life. The truth is, some cultures are stronger than others. Culture is not biological, it is social, and this means it is not genetic but acquired through learning and passed through interactions and into generations. The Jews have one of the strongest cultures, that even though Christianity came from their background, they still embrace Judaism. The Arabs, Chinese and Japanese are where they are because they haven’t allowed any drastic European trend from eating up their core. I suspect that Africa after all its initial hoax will embrace gay laws and the LGBT community eventually than others, especially as it becomes “cooler”.

Keep watching. Black culture has a strong porous affinity for the material and short termed as against any other race. Therefore, the differences in development between say the white and a black society has nothing to do with superior intelligence but that of consumerism as against production. The reason why the white society is what it is today is due to the default stronger culture they were created with which involves the zeal to produce for exploration, innovation and adventure. The African default culture is different and lacks these three features. The African culture values tradition so much that they don’t give room for changes, improvement and innovation.

We are consumers, we rarely produce

Looking away from the window to the mirror, you’d see that something must be wrong with blacks and Africans at large. In America, they are the ones that spray money at strip clubs. In Nigeria we spray money at parties, we flaunt wealth more on IG and use “giveaways” to gain unnecessary attention. In this minimalist movement era, we still bask in the complexities of retail consumerism than any other race. While we rarely produce, we are the biggest customers of luxury and consumer products. Beyond being customers, we need more black owned businesses. We need not just individual wealth but an interdependence of our own empires. We need our own ecosystems.

Beyond raw materials and commodity trading, we need processes and processing. Take for example, Cote d’ Ivoire sells off Cocoa and then imports Chocolate. Sierra Leon sells off Diamond and then imports Jewellery. Even Nigeria, we sell off Crude oil and imports petrol!

Materialism creates consumerism. It’s a wild goose chase where the things you strive to own ends up owning you. Too many people in Africa spend money they don’t have to buy the things they don’t need, just to impress the people they don’t like. Most times, those people don’t even care.

Bitterness and resentment surround us

Nothing good is attracted to misery. I tell people, confront what you don’t like and let it go. Don’t keep spilling your misery on other people’s happiness. I get upset when Blacks hold grudges from 200+ years ago of slavery. That’s too deep for a progressive mind. Some people even blame it for their own personal backwardness, even if laziness and their personal ignorance was the cause. I hate it when the best and award-winning black movies always have to be tied to slavery. Media isn’t helping, because if you keep telling the same old story, you’ll keep living the same old life.

I can relate to marginalisation, for I come from the Eastern part of Nigeria. I am Igbo, we fought a very bitter Civil war In Nigeria to liberate Biafra. It didn’t work, and till this day, we have been marginalised. I totally agree. But what has politics done for the areas like say the North East whom their leaders have been on top, are they really living more in wealth, peace or prosperity than us? My point is, the past may either make you bitter or better. We may be politically irrelevant, but if we took out any atom of bitterness and faced what we have, our economic brilliance, creativity, wisdom and entrepreneurial spirit, we can collaborate more, we can buy back everything we lost and more, including power and that freedom if we still need it. Let’s build something tangible like the Jews have done, other things like power will align. It is just the principles of life. So, face your work, at least you have one.

Things can either drain or inspire you. Blacks are seen as violent, they hold grudges in the most undiplomatic way (they call it being real), but spending your time in holding a grudge or bitterness of heart is like drinking a cup of poison and expecting the enemy to die. It disrupts grace and inner peace. And both is needed as the octane to move forward. Blacks and any tribe that feels it is being discriminated against needs to move further, ahead.

Drop the grudge, pick up excellence

The best way to fight any form of discrimination is excellence. I stumbled upon a macro economic data; there is only 3 black CEOS in the Fortune top 500 companies. That’s less than 1 percent. But maybe that number will go up if we got more educated and stopped being more of entertainers. Or at least do something so well that they can’t find your replacement. Definitely, we all need connections to get into the big room. So, it seems. But the truth is, a man’s gift can make room for him. Be so good, that when you walk into any room, you won’t need an introduction. With this one, let me Cite Obama. He once stated, “there’s no black male my age, who’s a professional, who hasn’t come out of a restaurant and is waiting for their car and somebody didn’t hand them their car keys,” Obama once told People magazine.

His wife, First Lady Michelle Obama, added that her husband had also once been mistaken for a waiter at a black-tie party and someone rudely asked him for a coffee. Another one asked that he please gets them a glass. On both occasions, he didn’t take offense. He just smiled. Well, that was before he became president. Now, does anyone want to try the same stunt on him. Even then, he wasn’t offended more than he was inspired. He had a better plan to stand up. That plan was to allow his excellence to do that for him. Excellence is the best way to fight discrimination. In your journey to building black excellence, especially through business, I look forward to working with you.