Oil prices edged higher on Wednesday on the prospects for stronger global economic growth amid increased COVID-19 vaccinations and a report that crude inventories in the United States, the world’s biggest fuel consumer, fell.

Brent crude futures for June rose by 16 cents, or 0.3 per cent, to $62.90 a barrel by 0657 GMT while U.S. West Texas Intermediate crude for May was up 14 cents, or 0.2 per cent, to $59.47.

The International Monetary Fund (IMF) in its April 2021 World Economic Outlook (WEO) presented Tuesday projected a six percent growth for the global economy in 2021, moderating to 4.4 percent in 2022, while the estimated growth for Sub-Saharan Africa, at 3.4 percent, with South Africa at 3.1 percent. and Nigeria’s economy, another oil producer to grow by 2.4 percent in 2021.

This is in effect which means that the global economy is recovering, in addition to the spread of vaccination, are the push for the oil price which had plunged in 2020.

But optimism about talks between the United States and Iran over Iran’s nuclear programme and an impending increase in supply by major oil producers capped gains.

“Optimism on the global economic outlook boosted sentiment in the crude oil market,” analysts from ANZ bank wrote in a note on Wednesday.

Prices were buoyed as data on Tuesday showed U.S. job openings rose to a two-year high in February while hiring picked up. This followed earlier data showing improvement in the services sectors in the U.S. and China.

The International Monetary Fund said on Tuesday unprecedented public spending to fight COVID-19 would push global growth to 6% this year, a rate unseen since the 1970s.

Optimism on a wider rollout of vaccines also boosted prices with U.S. President Joe Biden moving up the COVID-19 vaccine eligibility target for all American adults to April 19.

U.S. crude oil stockpiles fell more than expected in the week ended April 2, while fuel inventories rose, according to three market sources, citing American Petroleum Institute (API) figures ahead of government data on Wednesday.

Oil production in the U.S. is expected to fall by 270,000 barrels per day (bpd) in 2021 to 11.04 million bpd, the Energy Information Administration (EIA) said on Tuesday, a steeper decline than its previous monthly forecast for a drop of 160,000 bpd.

Iran and world powers held what they described as “constructive” talks on Tuesday and agreed to form working groups to discuss potentially reviving the 2015 nuclear deal that could lead to Washington lifting sanctions on Iran’s energy sector and increasing oil supply.

Oil prices dropped earlier this week after the Organization of the Petroleum Exporting Countries (OPEC) and allies, known as OPEC+, agreed to gradually ease oil output cuts from May.

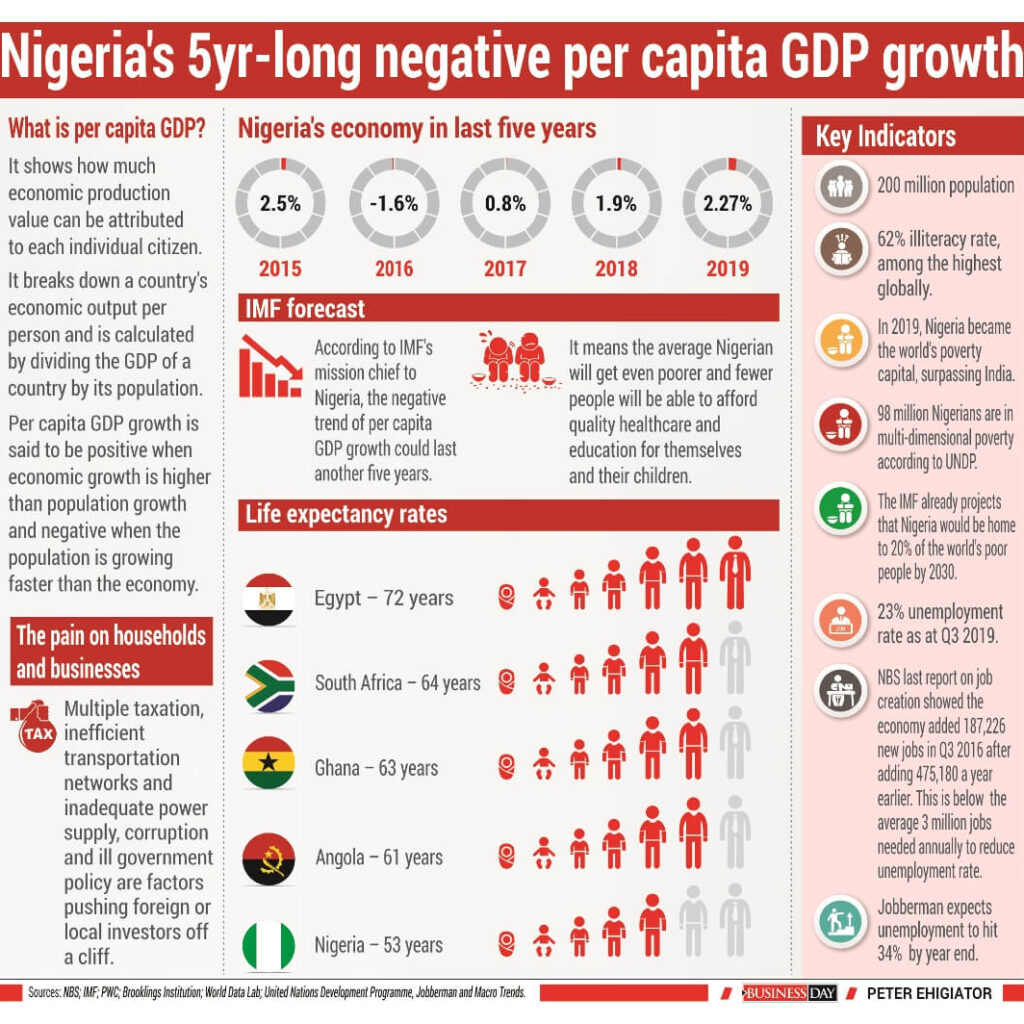

Five straight years of negative Per Capita GDP growth is unprecedented in Nigeria, at least, since the turn of democracy in 1999. But that is what has happened between 2015 and 2019.

For many Nigerians, connecting the dots between five years of an economy not expanding as fast as population is not so straightforward, not with an illiteracy rate of 62 percent, one of the highest globally.

What is unmistakeable, however, is the pain those five years of negative Per Capita GDP has wrecked on households and businesses, whether they understand what is happening or not.

Take the case of Jide Ibrahim (not real name) for example. Ibrahim’s highest qualification is a Bachelor’s degree in Human Kinetics from the Lagos State University (LASU). He worked at Woolworth, a South African clothing retailer, which closed its three stores in Nigeria in 2013.

It is been seven years and he is yet to pin down another job. His lack of job has forced some changes. He has had to move away from his two-bedroom apartment somewhere in Ikorodu to living with a friend in a one-bed apartment almost the size of a telephone booth within the same area.

When asked how he felt when he was laid off, he heaped the blame on Woolworth, saying the company unfairly asked people to leave after milking Nigeria dry.

“These foreign companies just use you and dump you,” Ibrahim said.

Little did he know that his lay off was no fault of Woolworth, but of the high cost of operating a business in Nigeria, which sucked the life out of the South African retailer and sent it scrambling back from where it came.

Hear what Woolworth’s CEO, Ian Moir, said about the exit at the time: “When an investment no longer generates viable returns, difficult decisions have to be made to contain costs.”

High rental costs and duties and complex supply chain processes made trading in Nigeria highly challenging, according to Moir.

Woolworth’s 18-month foray into Nigeria is peculiar for a company that has been operating in South Africa for decades – since 1931 in fact – and has operations in various African countries and elsewhere. The remaining 59 stores in 11 African countries were not affected by the Nigeria decision.

Since that time, Woolworth has expanded to 64 stores and is in 13 African countries.

Woolworth’s experience is not unique; several companies have had to close shop in Nigeria due to the country’s difficult business environment.

Though strides have been made to improve the business environment, the country sits at a lowly 131 of 180 countries surveyed by the World Bank.

Challenges from tax multiplicity to inefficient transportation networks and lack of adequate power have been unbearable to businesses. Over regulation and corruption in government are also chief culprits in pushing businesses, foreign or local, off the cliff.

This shows Ibrahim’s anger should be channelled towards the Nigerian government, which has failed to create an enabling environment for businesses to succeed.

On the evidence of the declining flows of FDI into the country since 2014 and tales of woes by local businesses, the government has not been able to significantly improve the business environment.

Since 2008, when Nigeria attracted a record $8 billion FDI following a wave of privatisation, the country got $3 billion on average between 2009 and 2015, and $1 billion a year since then, according to the NBS, effectively trailing smaller peers like Ghana.

Considering the size of Nigeria’s population, a billion dollars works out to $5 per head.

Foreign companies are not the only businesses to have walked out on Nigeria, even local companies have struggled.

The Manufacturers Association of Nigeria (MAN) said about 272 firms were forced out of business in 2016 alone, 50 of which were manufacturing companies, amid stifling government regulation. The manufacturers say that led to 180,000 job losses in the period.

Surely, Ibrahim and the over 20 million Nigerians without jobs, should hold the government more accountable for the damage done to their lives by bad policies. The lack of jobs has helped poverty thrive.

Nigeria, home to 87 million poor people, became the world’s poverty capital in 2019, overtaking India, according to a Brooklings Institution report.

Another set of statistics by the World Data Lab estimates that 90 million Nigerians live under $1.90 a day, while the United Nations Development Programme reported that 98 million Nigerians were in multi-dimensional poverty.

Yet the pain of a floundering economy growing slower than population also shows it is no respecter of persons. The rich have perhaps suffered just as much.

Take Aliko Dangote, Nigeria’s richest man, who doubles as the continent’s wealthiest person. Dangote is no longer worth half as much as he was in 2014.

Despite remaining the richest African for almost a decade, his fortune is down a staggering 72 percent to $7 billion from $25 billion in 2014, according to Forbes data.

What is Per Capita GDP and why is it important?

At its most basic interpretation, Per Capita GDP shows how much economic production value can be attributed to each individual citizen. It breaks down a country’s economic output per person and is calculated by dividing the GDP of a country by its population.

Per Capita GDP growth is said to be positive when economic growth is higher than population growth and negative when the population is growing faster than the economy.

The per capita metric is a popular measure of the standard of living, prosperity, and overall well-being in a country. A high Per capita GDP indicates a high standard of living while a low one indicates that a country is struggling to supply its inhabitants with everything they need.

Luxembourg, a small European country surrounded by Belgium, France and Germany, has the highest GDP per capita globally with $113,196 as at 2019, according to IMF data.

Switzerland ($83,716) and Norway ($77,975) make up the top three countries with the highest GDP per capita.

On the flip side, war-torn South Sudan ($275), Burundi ($309) and Eritrea ($342) make up countries with the lowest Per Capita GDP in the world. Nigeria ranks 138 with $2,222, behind Ghana with $2,223.

Five years of negative Per capita GDP

Nigeria’s relatively low Per Capita GDP, which paints a dim picture of the living standards in the country, has been worsened by five straight years of contraction.

The last time Nigeria had a positive Per Capita GDP was in 2014, as the economy has struggled since a lengthy collapse in global oil prices that began in mid-2014. When not contracting, the economy has grown at a tepid 2 percent rate compared to average population growth rate of 2.6 percent.

The economy grew 2.5 percent in 2015 before contracting by 1.6 percent in 2016. As oil prices recovered, the economy turned the corner on its first recession in a quarter of a century by growing 0.8 percent in 2017 and a 1.9 percent growth in 2018. In 2019, the economy grew 2.27 percent, capping five years of an economy that didn’t grow fast enough to create new opportunities for a rapidly growing population.

Make it another five years

Prior to the COVID-19 pandemic, the IMF predicted that income per head will continue falling for another three years until at least 2023.

However, with the pandemic, that forecast is grimmer. The trend of negative Per Capita GDP growth could last another five years, according to Jesmin Rahman, the International Monetary Fund’s (IMF) mission chief to Nigeria. That is worse than the initial projection.

“We are going to see the contraction in real Per Capita GDP pick up in the next five years,” Rahman says.

Rahman says it could take Nigeria at least three years before the economy grows at the modest 2 percent rate at which it expanded in 2019 prior to the COVID-19 pandemic.

Another five years of Per Capita GDP contraction is a painful squeeze for a country with gross domestic product per capita of just $2,222, meaning Nigerians will get even poorer than they are now for another five years as their incomes continue to shrink and the economy bleeds jobs.

It means more Nigerians will fall into a poverty pit. The IMF already projects that Nigeria would be home to 20 percent of the world’s poor people by 2030.

Another painful stretch of negative per capita GDP growth also means fewer people will be able to afford quality education for themselves and their children.

For instance, premium primary education alone in Lagos, Nigeria’s commercial capital, could cost anything between N700,000 ($1,944) to N1 million per annum ($2,777). That works out to an average of $2,360 (N849,600), higher than Nigeria’s per capita GDP of $2222.

Fewer people will also be able to afford quality healthcare in a country where the average life expectancy is just 53 years. Only four countries in the world have lower life expectancy rates and they are Sierra-Leone, Chad, Lesotho and Central Africa republic.

South Africa’s life expectancy is 63 years, at par with Ghana’s but lower than the World average of 70 years, according to United Nations World Population data.

Countries like Hong Kong, Japan, Singapore and have an average life expectancy of 83 years.

The job-seeker in Nigeria will also have fewer jobs to compete for with an even larger population of job seekers. Ibrahim may struggle to find a job for another five years.

Data from Jobberman, which recruits mainly white-collar employees and does not track those looking for non-skilled, blue-collar work, sees unemployment in the nation of more than 200 million soaring to 34 percent by the end of the year from 23 percent in 2019.

Other estimates suggest that the unemployment rate could hit 50 percent by 2021. The country’s unemployment rate quickened to a more than six-year high of 23 percent in 2019, the last time the NBS measured the rate.

Rising unemployment and higher inflation has meant the country’s misery index has deteriorated to be almost at par with failed countries from Syria to Lebanon.

As it stands, over 22 million employable Nigerians are out of work and another 15 million are underemployed. There’s little hope that the country can generate sufficient jobs for its people who are forecast to reach 400 million by 2050.

The last time the Nigerian Bureau of Statistics (NBS) published data on job creation it showed the economy added 187,226 new jobs in the third quarter of 2016 after adding 475,180 a year earlier.

As Nigerians get poorer over the course of the next five years, it may also mean more companies, especially small businesses, are at risk of failing as falling consumer purchasing power leads to a reduction in sales and revenues.

Though there is paucity of data on the failure rate among Nigerian start-ups, the one available estimate given by a Nigerian bank Stanbic IBTC claimed that over 80 percent of Nigerian start-ups fail within their first five years.

That will get worse if the economy continues to underperform population growth for another five years.

What experts say is the way out for sluggish economic growth

Jesmin Rahman

Rahman is IMF mission chief to Nigeria. She recommended a raft of fiscal policies that lift per capita GDP growth in Nigeria during a recent webinar hosted by the American Business Council.

Here is what she said: Nigeria has always been to me a fascinating country with huge potential; there’s nothing it doesn’t have. Nigeria has a huge population, and natural resources, yet this is a country that when you compare to its peers on social indicators and living standards, it is not where it should be.

Per capita income used to be $7,000 in mid-1980s since then it has gyrated in sync with oil prices. There are quite a few challenges Nigeria needs to tackle if this course is to be altered. At the current population growth rate of 2.6%, Nigeria’s population is projected at 400 million by 2050. The labor force is growing very rapidly much of which is getting absorbed in either the informal sector or not employed at all. Informal sector wages are very low. Basic literacy among the young population is also very low. Six of out ten out of school children are Nigerians so these are very sobering statistics.

When you look at poverty rate, it is around 40% and given the population projection, by 2030, the World Bank estimates that a fifth of the world’s poorest will be housed in Nigeria. When you add regional dimension, the situation is even scarier because you will the concentration of all of these low statistics in one part of the country.

To turn Nigeria’s population into human capital so the economy grows, Nigeria needs strong job growth and investment in social indicators; education, health and some of the very basic services.

My colleagues in the IMF did a basic estimate of how much it would cost the country to reach the SDGs and they came up with 18% of GDP which would come largely from government even though donor community would help. This reemphasises the importance of growth because without stronger growth to raise revenues, and without those revenues, it would be hard to provide for these very basic and much needed things.

The second challenge is to reduce the dependence on oil. In some ways the Nigerian economy has achieved diversification. Oil only counts for 10% of GDP and 1% of employment so you can say that’s a kind of diversification but the non-oil economy depends heavily on the oil prices through direct and indirect linkages and oil also accounts for 50% fiscal revenues and over 80% of exports. Oil is also important for FX inflows even though remittances help. Because of this, in order to have any form of meaningful diversification, Nigeria needs to move on these fronts as well: diversify fiscal revenues and exports in addition to diversifying GDP base.

Nigeria’s DNA is oil and unless diversification is seen on both fiscal and external fronts, this perception is unlikely to change and this perception needs to change if we are to avoid the big cycles.

Charles Robertson

Robertson, the global chief economist at Renaissance Capital, during a Financial Times summit as far back as 2018, said the country needs to grow by between 4-5 percent for per capita GDP to stop contracting.

“As Nigeria has grown at 2 per cent per capita since 1992, our medium-term base should be at least 4-6 per cent GDP growth,” Robertson said.

But Nigeria cannot match the 4-6 per cent per capita GDP growth of industrialising countries because adult literacy at 60 per cent is too low and electricity consumption is under half the minimum required level for sustained industrialisation, according to Robertson.

“To push headline GDP growth to 6.5-8.5 per cent would require an adult literacy campaign, a trebling of electricity consumption and a doubling of investment to GDP,” Robertson said.

John Ashbourne

Ashbourne, a senior emerging markets economist at economic consulting Capital Economics also shared the following views during the FT summit.

“The government needs to unlock private sector investment by improving the business environment and encouraging participation in the non-oil sector.

The country also desperately needs better infrastructure and reforms to the state-dominated oil sector.”

Razia Khan

Razia Khan, chief Africa economist at Standard Chartered bank also had these to say: “Nigeria has all the necessary building blocks to achieve much faster growth. With its low base, youthful population and scale, a growth rate exceeds the rate of population growth should be easily achievable.

“It needs to develop more institutions that are more resilient than tends to be the case in typical resource economies, for example a tax base independent of oil and a banking sector that can meet the borrowing needs of the private sector. Nigeria has failed to make a transition away from being an oil economy.”

Olusegun Omisakin

Omisakin is the Chief Economist and Director of Research & Development at the Nigerian Economic Summit Group (NESG). His views are as follows: “The effects of COVID-19 pandemic on global health and socio-economic conditions will remain for the foreseeable future.

“For Nigeria, economic policies have to remain broadly expansionary to hasten recovery. Implementation of the Medium-Term National Development Plans (MTNDP) and Nigerian Economic Stimulus Plan (NESP) will quicken the recovery in 2021.

“More focus should also be on improving the business environment through reforms.”

Crude oil is perhaps the most crucial commodity in the world, with the West Texas Intermediate (WTI) crude being the most traded commodity globally. The reason for this is not farfetched as oil is useful in just about every aspect of the economy, from production to transportation. Therefore, any economy that desires to grow will need oil for its activities.

The oil market might however be a bit confusing for many people who are not energy economists. In this piece, we try to explain the dynamics of the market and how it affects households and businesses from Nigeria to other parts of the world.

Types of Crude oil: How can crude oil be sweet or sour?

There are different varieties and grade of crude oil. Crude oil can be categorised based on viscosity and sulphur. Viscosity measures how light or thick the crude oil is at room temperature. Crude oil is classified as light if it is non-sticky and flows freely at room temperature while it is thick if it is sticky and does not flow freely at room temperature.

Crude oil can also be classified as sweet or sour based on the level of sulphur present in the content of the oil. When the sulphur is low, it means the crude oil is sweet and when the sulphur level in the oil is high, it means the crude oil is sour.

Based on this classification, WTI and Brent crude is light and sweet while Dubai crude is medium-level thick and sour. Another crude oil produced in Nigeria called Bonny Light crude is also light and sweet. Among the types or grades of crude oil, the most popular is the Brent crude. Brent oil is used as a benchmark for the oil market because of the ease at which it can be processed into a product such as petrol. That makes demand for Brent more consistent than others, making it a better indicator for the global oil price.

What has been the trend in crude oil prices in 2020?

The outbreak of the coronavirus has influenced the changes in the price of oil in 2020. The lockdowns, decline in industrial activities and travel restriction resulted in a reduction in the demand for crude oil. Therefore, industries that required crude oil for their operation did not demand much because of a decline in activities. There were also fewer cars on the road as a result of the stringent lockdown measures put in place by the government and jet fuel use was limited as there were travel restrictions. In January, Brent crude oil averaged $63.65 per barrel, but declined to $55.66 in February and further dropping to $32.01 by March as demand plummeted.

The price war between Saudi Arabia and Russia also played a big role in triggering the price downturn. Saudi Arabia could not convince Russia to cut oil production as other OPEC members agreed to do. OPEC decided to cut oil production to reduce oil supply which was running far ahead of demand but Russia, a major oil producer refused to cut back on production. This went on till April when Brent crude dropped to $18.38, the lowest in 18 years.

WTI also plunged to the negative territory for the first time in history, this means that since there was excess supply or production of oil and low demand for the commodity, producers ran out of storage facilities. Therefore, producers had to pay buyers to collect crude oil from them to make available more storage space.

In May, OPEC + after much agitations agreed to cut production to prevent further harm on the world economy. Brent oil price began to rise as world economies around the world re-opened business, coupled with the resumption of air travels.

Ever since May, Crude oil price has been gradually increasing. Brent oil price averaged $29.38 in May, rising to $40.27 per barrel in June and averaging $43.24 per barrel in July 2020.

Why crude oil matters to the Nigerian economy

Crude oil is the major product that earns revenue for Nigeria which implies that Nigeria is an oil dependent economy. Oil accounts for more than 80 per cent of export and foreign exchange earnings. Prior to the discovery of oil, Nigeria’s mainstay source of revenue was agriculture. However, with the discovery of crude oil in 1958, Nigeria shifted attention away from agriculture to crude oil.

However, because Nigeria relies heavily on the proceeds of crude oil, the state of the economy is dictated by the state of the price of crude oil and unfortunately, the price of crude oil is unstable. Nigeria is a net oil-exporting country. Nigeria both exports crude oil and imports the refined crude oil products (such as petroleum, kerosene, diesel, liquefied petroleum gas). During times where the price of crude of crude oil is high, then the economy is usually vibrant and at times when the price of crude oil is low, the economy shrinks.

There are certain economic indicators that reveal the health of an economy. These indicators are called macroeconomic variables, some of which include gross domestic products (GDP), inflation, unemployment and exchange rate. These indicators will show at a glance whether a nation is doing well or not.

When there is a fall in crude oil price in Nigeria, government revenue declines which in turn causes government expenditure to fall. This will result in a fall in economic activities or production hereby causing GDP to decline. The GDP is the total value of goods produced and services provided in a country during one year. As a result of the reliance on crude oil proceeds, when the price of crude oil fall, oil revenue and other indicators are also affected.

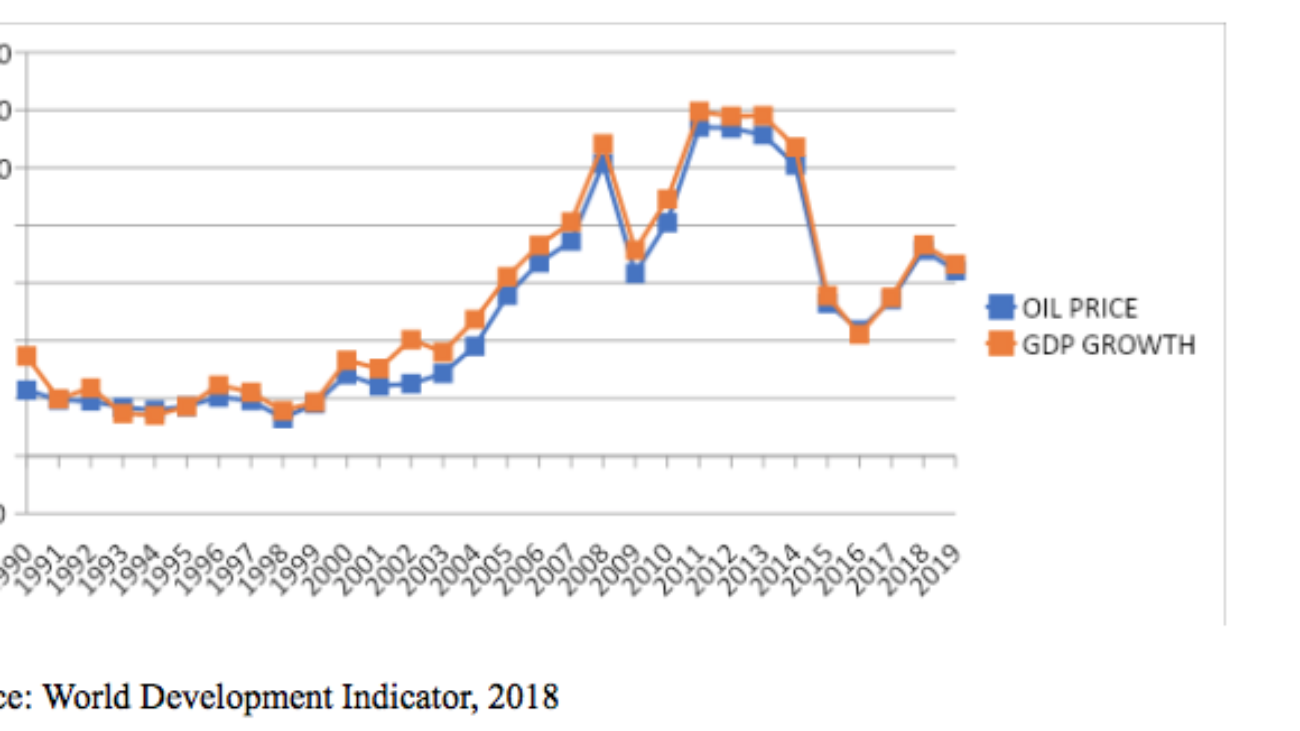

For instance, between 2014 and 2016, crude oil price crashed from $100.85 to $43.74. After the crash, Nigeria crude oil revenue fell from 6.997 trillion in 2016 to 4.1 trillion in 2017. As oil price increased from $54.71 in 2017 to $71.34 in 2018, consequently, crude oil revenue rose from 4.1 trillion in 2017 to as high as 9.4 trillion in 2018 according to CBN.

The figure below shows the trend of oil movement and GDP changes in Nigeria from 1990 to 2019. The graph shows that the growth rate of Nigeria and the oil price move together in the same direction. This implies that when oil price increases, the GDP experiences a boom also and when oil price drops, GDP also drops.

Source: World Development Indicator, 2018

This shows that the oil price dictates whether the Nigerian economy grows or not and since the price of oil is determined by factors outside the control of the country, it means Nigeria is at the mercy of whatever happens to oil price.

Nigeria benefited from the rising oil price from the year 2000 to 2007. During this period, oil price increased from $28.42 in 2000 to $74 U.S dollars in 2007. Consequently, the growth rates in Nigeria also show a rising trend.

There was an unexpected drop in oil price in 2014, oil price declined from $100.85 in 2014 to $43.74 in 2016, the growth rate also declined from 6.3 per cent in 2014 to -1.61 per cent sending the economy into a recession.

A recession is characterised by falling GDP, low production/manufacturing activities, rising unemployment, and falling prices of goods and services. Nigeria entered into a recession when the GDP growth rate for the second quarter of 2016 came out negative.

As earlier stated, when the GDP of a country is affected, all other indicators also will perform poorly. For instance, in 2016 when the GDP of Nigeria turned negative, inflation rate rose from 13.9% in the second quarter of 2016 to 14.2% in the last quarter of 2016. By 2017, inflation rose to 18.8% in the third quarter according to data from the National Bureau of Statistics (NBS). When inflation increases, it means the prices of goods and services would increase, hereby creating economic hardship.

The NBS also published data revealing that unemployment rate in Nigeria rose from 12.1% to 13.9% in the first and second quarter in 2016 respectively and by the last quarter of 2016, unemployment rate increased to 14.2%. This shows that oil movement influences the macroeconomic stability of oil dependent countries like Nigeria.

Inflation and unemployment increase during recession because of low economic activities. Firms lay off workers and employ less in order to cover their cost of operation.

The outbreak of the corona virus in 2020 has had severe consequences on the Nigerian economy in the last few months. While Nigeria was still dealing with the pandemic in its early stage, there was a sudden crash in the price of crude oil as a result of the price war between Saudi Arabia and Russia. Oil price which closed at about $60 per barrel as at December 2019 fell to as low as $18 per barrel as at April 2020. This twin shock further weakened the already fragile economy. Inflation rate increased from 12.26 percent in March to 12.34 percent in April, further rising to 12.40 by May and by June it stood a 12.56 per cent according to NBS.

How does oil price movement affects household and businesses in Nigeria?

Consumers and firms are not exempted from the influence of oil price movements. Recall that Nigeria is a major oil exporter and depends largely on crude oil sales for revenue. Therefore, a higher oil price is good news for the economy because export revenue will increase. The increase in revenue means the government is better able to implement its budget whether it’s paying workers’ salaries or implementing capital projects.

Consumers tend to spend more in a period of oil price booms, which is characterised by stable incomes and creation of direct and indirect jobs. Their demand for goods and services tend to rise in this period. The firms on the other hand will benefit from increased consumer spending which translates to higher sales of their products and services.

Conversely, when oil prices decline, there will be a decrease in export revenue and government expenditure. Lower oil prices also put the exchange rate at risk as it exposes the naira to pressure against the dollar. Given that oil exports account for over 80 percent of foreign exchange inflows into Nigeria, a period of low oil prices tends to lead to dollar shortages, naira devaluation and higher inflation. A devaluation of the naira is bad news for households and businesses as it often leads to higher inflation. Many manufacturers rely on imports to produce, so when the exchange rate weakens it means higher production costs for them and that is mostly followed by a hike in the price of the goods they sell which is negative for consumers.

The higher inflation triggered by an exchange rate depreciation squeezes households who are left to contend with lower purchasing power in the face of more expensive goods and services. This implies that households will have less income to spend on goods and services, therefore they will demand less.

The firms will also have less access to funds for investment and could lay off workers in an attempt to cover their operating costs. When firms cut back on expansion, it translates to lower economic growth.

Need for diversification

All the above prove that the Nigerian economy will continue experiencing macro-economic instability until it can find a way to depend less on oil sales for its revenue.

The government will need to invest more in the health and education of the Nigerian citizens. According to the United Nation Children’s Funds (UNICEF) in 2019, there are about 10.5 million out of school children in Nigeria and there are also those who are in school but receive substandard education. Bill Gates, the co-founder of the Bill and Melinda Foundation during his visit to Nigeria in 2018 said the only way Nigeria can escape poverty and enjoy sustained prosperity is by investing in the health and education of the people. He also stated that the life expectancy in Nigeria is one of the worst in the world. ‘‘The most important choice the government can make is to maximize its greatest resources, the Nigerian people. Nigeria will thrive when every Nigeria is able to thrive’’ He said.

The inadequate infrastructure in Nigeria would also make diversification difficult. The World Economic Forum Global Competitiveness Index in 2018 reported that Nigeria ranks 132 out of 137 in the quality of overall infrastructure, 127 out of 137 in quality roads and 136 0ut of 137 in quality of electricity supply. Productivity will only increase when the necessary infrastructure is in place.

The agricultural sector is also a viable sector. The increase in agricultural activities will invariably lead to the development of other sectors that have linkages to the agricultural sector such as the manufacturing and textile industries due to the supply of raw materials from agriculture to feed these industries. The tourism industry is another viable industry that could be harnessed to drive economic diversification since Nigeria is endowed with rich natural ecosystems and cultural diversity.

The telecommunication industry in Nigeria has one of the largest telecoms in Africa. The effective exploitation of this sector will bring about efficiency and productivity in the telecom sector and eventually enhance economic growth.