Nigeria’s currency, Naira on Wednesday weakened further by 0.12 percent following strong demand for and shortage of dollars at the Investors and Exporters (I&E) Forex window. (FX)

The foreign exchange daily turnover declined significantly by 70.96 percent to $11.85 million on Wednesday compared with $40.80 million recorded on Tuesday.

Consequently, after trading on Wednesday naira/dollar exchange rate closed at N411.00k as against N410.50k quoted on the previous day at the FX I&E window, data from the FMDQ showed.

Currency traders who participated in the trading on Wednesday maintained bids at between N405.00k and N438.00k/$.

Exchange rate remained flat at N485 at the Bureau De Change (BDC) segment of the foreign exchange market and the parallel market.

At the money market, the Nigeria treasury bills secondary market closed on a flat note on Wednesday, with the average yield across the curve remaining unchanged at 3.97 percent, according to a report by FSDH research. Average yields across short-term, medium-term, and long-term maturities closed at 2.40 percent, 3.30 percent, and 5.46 percent, respectively.

The Overnight (O/N) rate decreased by 0.25 percent to close at 13.50 percent on Wednesday as against the last close of 13.75 percent on Tuesday, and the Open Buy Back (OBB) rate decreased by 0.83 percent to close at 12.67 percent from 13.50 percent on the previous day. FX

“We expect money market rates to remain at elevated levels due to a possible OMO auction by the CBN,” analysts at FSDH said.

In the Open Market Operation (OMO) bills market, the average yield across the curve increased by 13 bps to close at 6.46 percent on Wednesday as against the last close of 6.33 percent the previous day.

Selling pressure was seen across medium-term and long-term maturities with average yields rising by 22 bps and 13 bps, respectively. However, the average yield across short-term maturities closed flat at 4.20 percent.

Yields on 15 bills advanced with the 28-Sep-21 maturity bill registering the highest yield increase of 62 bps, while yields on 11 bills remained unchanged.

The Debt Management Office (DMO) has released its FGN Bonds Issuance Calendar for the second quarter of 2021, indicating plans to raise funds in the range of N450 billion-N540 billion to finance the budget deficit over the next three months.

Furthermore, the DMO is expected to offer bonds during the quarter through re-opening of 10-year (N150 billion – N180 billion), 15-year (N150 billion – N180 billion), 25-year (N100 billion – N120 billion), and 30-year (N50 billion – N60 billion) tenors.

FGN bonds secondary market closed on a mildly negative note on Wednesday as the average bond yield across the curve cleared higher by 3 bps to close at 6.80 percent from 6.77 percent on the previous day.

Emerging data about Nigeria’s Foreign exchange inflows into the Investors and Exporters (I&E) forex window indicate that the Central Bank (CBN) is keeping its word to reduce its intervention in the dynamics of the market.

Inflows into the market dropped to six months low following significant decline by 99.3 percent in interventions by the Central Bank of Nigeria (CBN), which hitherto was a dominant player in the market.

Godwin Emefiele, the CBN governor, said at the last Monetary Policy Committee (MPC) meeting briefing that since January the CBN had not intervened in the I&E window.

The market has always operated within a band of around N409 to the dollar. At some point, it attained N412 and N413, and began to move, and that it is how it is supposed to move, he said. “The CBN job is to moderate the market in line with where we think exchange rate should be,” Emefiele had said.

Data from the FMDQ captured in a report by FSDH Research show that total foreign exchange inflow into the window decreased by 39.48 percent to $565.9 million in February 2021, compared to $935.2 million in September 2020.

The inflows comprised of Foreign Direct Investment (FDI), which fell to $7.5 million in February 2021 from $30.8 million in September 2020; Foreign Portfolio Investment (FPI) $17.9 million in February 2021 ($36.8m in September 2020), other corporate $9.3 million in February 2021 ($22.4m in September 2020), and the CBN $2.9 million in February 2021 ($434.5m in September 2020).

Others include inflows from exporters, which dropped to $175.7 million in February 2021 from ($206.8m in September 2020), individuals $2.5 million in February 2021 from ($29.4m in September 2020), and non-bank corporate, which declined from $350.1 million September 2020, to $175.5 million in February 2021.

Inflows from the CBN fell by 99.3 percent from $434.5 million in September 2020 to $2.9 million in February 2021.

Despite the positive GDP growth in the fourth quarter of 2020, inflows from FDI and FPI remain low in the first two months of 2021.

This suggests low investors’ confidence amid uncertainty relating to foreign exchange management and insecurity concerns, analysts at FSDH said.

Despite rising crude oil prices, Nigeria’s External Reserves have lost 5.7 percent of its value from January 25 to March 17, 2021, according to the report.

Challenged oil inflows due to OPEC’s cuts, weaker foreign investment inflows, high demand for foreign currency to finance imports and other needs and possible clearance of FX backlogs are factors that continue to weaken External Reserves.

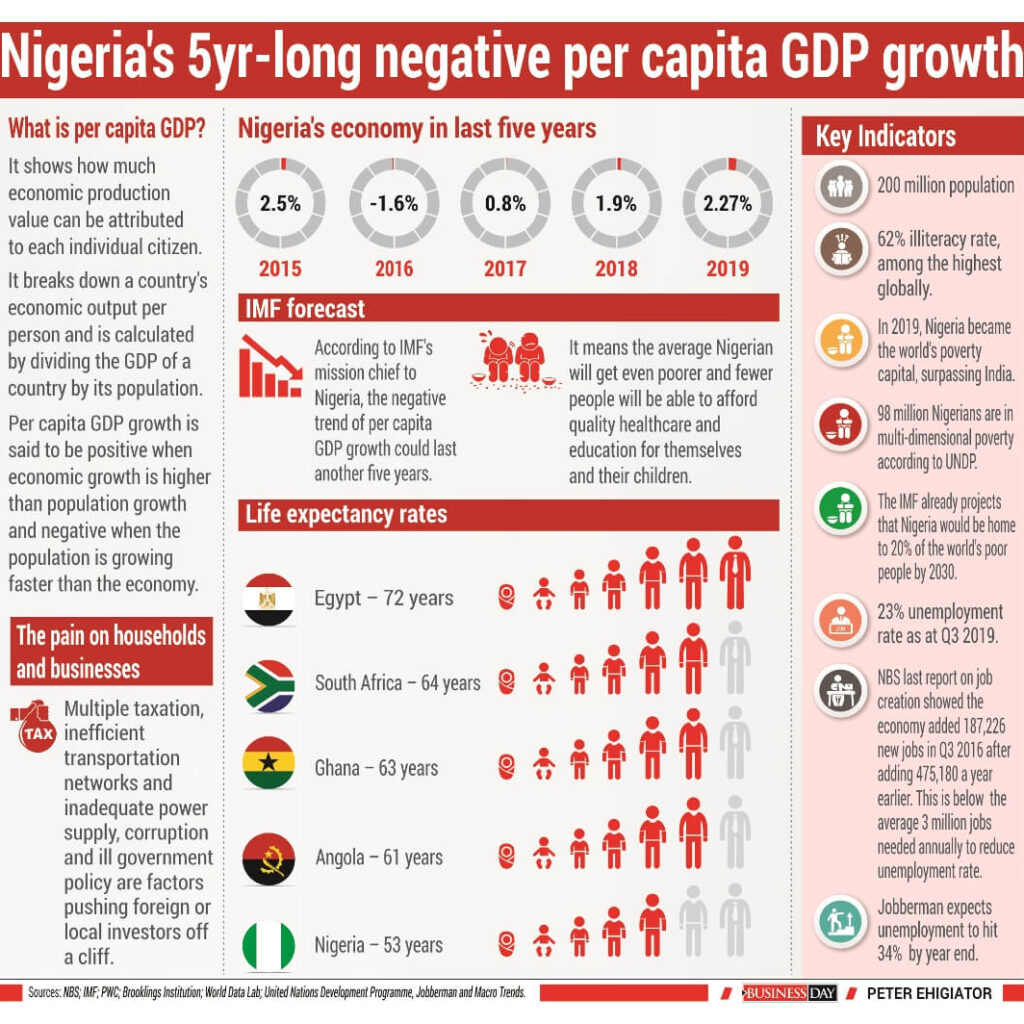

Five straight years of negative Per Capita GDP growth is unprecedented in Nigeria, at least, since the turn of democracy in 1999. But that is what has happened between 2015 and 2019.

For many Nigerians, connecting the dots between five years of an economy not expanding as fast as population is not so straightforward, not with an illiteracy rate of 62 percent, one of the highest globally.

What is unmistakeable, however, is the pain those five years of negative Per Capita GDP has wrecked on households and businesses, whether they understand what is happening or not.

Take the case of Jide Ibrahim (not real name) for example. Ibrahim’s highest qualification is a Bachelor’s degree in Human Kinetics from the Lagos State University (LASU). He worked at Woolworth, a South African clothing retailer, which closed its three stores in Nigeria in 2013.

It is been seven years and he is yet to pin down another job. His lack of job has forced some changes. He has had to move away from his two-bedroom apartment somewhere in Ikorodu to living with a friend in a one-bed apartment almost the size of a telephone booth within the same area.

When asked how he felt when he was laid off, he heaped the blame on Woolworth, saying the company unfairly asked people to leave after milking Nigeria dry.

“These foreign companies just use you and dump you,” Ibrahim said.

Little did he know that his lay off was no fault of Woolworth, but of the high cost of operating a business in Nigeria, which sucked the life out of the South African retailer and sent it scrambling back from where it came.

Hear what Woolworth’s CEO, Ian Moir, said about the exit at the time: “When an investment no longer generates viable returns, difficult decisions have to be made to contain costs.”

High rental costs and duties and complex supply chain processes made trading in Nigeria highly challenging, according to Moir.

Woolworth’s 18-month foray into Nigeria is peculiar for a company that has been operating in South Africa for decades – since 1931 in fact – and has operations in various African countries and elsewhere. The remaining 59 stores in 11 African countries were not affected by the Nigeria decision.

Since that time, Woolworth has expanded to 64 stores and is in 13 African countries.

Woolworth’s experience is not unique; several companies have had to close shop in Nigeria due to the country’s difficult business environment.

Though strides have been made to improve the business environment, the country sits at a lowly 131 of 180 countries surveyed by the World Bank.

Challenges from tax multiplicity to inefficient transportation networks and lack of adequate power have been unbearable to businesses. Over regulation and corruption in government are also chief culprits in pushing businesses, foreign or local, off the cliff.

This shows Ibrahim’s anger should be channelled towards the Nigerian government, which has failed to create an enabling environment for businesses to succeed.

On the evidence of the declining flows of FDI into the country since 2014 and tales of woes by local businesses, the government has not been able to significantly improve the business environment.

Since 2008, when Nigeria attracted a record $8 billion FDI following a wave of privatisation, the country got $3 billion on average between 2009 and 2015, and $1 billion a year since then, according to the NBS, effectively trailing smaller peers like Ghana.

Considering the size of Nigeria’s population, a billion dollars works out to $5 per head.

Foreign companies are not the only businesses to have walked out on Nigeria, even local companies have struggled.

The Manufacturers Association of Nigeria (MAN) said about 272 firms were forced out of business in 2016 alone, 50 of which were manufacturing companies, amid stifling government regulation. The manufacturers say that led to 180,000 job losses in the period.

Surely, Ibrahim and the over 20 million Nigerians without jobs, should hold the government more accountable for the damage done to their lives by bad policies. The lack of jobs has helped poverty thrive.

Nigeria, home to 87 million poor people, became the world’s poverty capital in 2019, overtaking India, according to a Brooklings Institution report.

Another set of statistics by the World Data Lab estimates that 90 million Nigerians live under $1.90 a day, while the United Nations Development Programme reported that 98 million Nigerians were in multi-dimensional poverty.

Yet the pain of a floundering economy growing slower than population also shows it is no respecter of persons. The rich have perhaps suffered just as much.

Take Aliko Dangote, Nigeria’s richest man, who doubles as the continent’s wealthiest person. Dangote is no longer worth half as much as he was in 2014.

Despite remaining the richest African for almost a decade, his fortune is down a staggering 72 percent to $7 billion from $25 billion in 2014, according to Forbes data.

What is Per Capita GDP and why is it important?

At its most basic interpretation, Per Capita GDP shows how much economic production value can be attributed to each individual citizen. It breaks down a country’s economic output per person and is calculated by dividing the GDP of a country by its population.

Per Capita GDP growth is said to be positive when economic growth is higher than population growth and negative when the population is growing faster than the economy.

The per capita metric is a popular measure of the standard of living, prosperity, and overall well-being in a country. A high Per capita GDP indicates a high standard of living while a low one indicates that a country is struggling to supply its inhabitants with everything they need.

Luxembourg, a small European country surrounded by Belgium, France and Germany, has the highest GDP per capita globally with $113,196 as at 2019, according to IMF data.

Switzerland ($83,716) and Norway ($77,975) make up the top three countries with the highest GDP per capita.

On the flip side, war-torn South Sudan ($275), Burundi ($309) and Eritrea ($342) make up countries with the lowest Per Capita GDP in the world. Nigeria ranks 138 with $2,222, behind Ghana with $2,223.

Five years of negative Per capita GDP

Nigeria’s relatively low Per Capita GDP, which paints a dim picture of the living standards in the country, has been worsened by five straight years of contraction.

The last time Nigeria had a positive Per Capita GDP was in 2014, as the economy has struggled since a lengthy collapse in global oil prices that began in mid-2014. When not contracting, the economy has grown at a tepid 2 percent rate compared to average population growth rate of 2.6 percent.

The economy grew 2.5 percent in 2015 before contracting by 1.6 percent in 2016. As oil prices recovered, the economy turned the corner on its first recession in a quarter of a century by growing 0.8 percent in 2017 and a 1.9 percent growth in 2018. In 2019, the economy grew 2.27 percent, capping five years of an economy that didn’t grow fast enough to create new opportunities for a rapidly growing population.

Make it another five years

Prior to the COVID-19 pandemic, the IMF predicted that income per head will continue falling for another three years until at least 2023.

However, with the pandemic, that forecast is grimmer. The trend of negative Per Capita GDP growth could last another five years, according to Jesmin Rahman, the International Monetary Fund’s (IMF) mission chief to Nigeria. That is worse than the initial projection.

“We are going to see the contraction in real Per Capita GDP pick up in the next five years,” Rahman says.

Rahman says it could take Nigeria at least three years before the economy grows at the modest 2 percent rate at which it expanded in 2019 prior to the COVID-19 pandemic.

Another five years of Per Capita GDP contraction is a painful squeeze for a country with gross domestic product per capita of just $2,222, meaning Nigerians will get even poorer than they are now for another five years as their incomes continue to shrink and the economy bleeds jobs.

It means more Nigerians will fall into a poverty pit. The IMF already projects that Nigeria would be home to 20 percent of the world’s poor people by 2030.

Another painful stretch of negative per capita GDP growth also means fewer people will be able to afford quality education for themselves and their children.

For instance, premium primary education alone in Lagos, Nigeria’s commercial capital, could cost anything between N700,000 ($1,944) to N1 million per annum ($2,777). That works out to an average of $2,360 (N849,600), higher than Nigeria’s per capita GDP of $2222.

Fewer people will also be able to afford quality healthcare in a country where the average life expectancy is just 53 years. Only four countries in the world have lower life expectancy rates and they are Sierra-Leone, Chad, Lesotho and Central Africa republic.

South Africa’s life expectancy is 63 years, at par with Ghana’s but lower than the World average of 70 years, according to United Nations World Population data.

Countries like Hong Kong, Japan, Singapore and have an average life expectancy of 83 years.

The job-seeker in Nigeria will also have fewer jobs to compete for with an even larger population of job seekers. Ibrahim may struggle to find a job for another five years.

Data from Jobberman, which recruits mainly white-collar employees and does not track those looking for non-skilled, blue-collar work, sees unemployment in the nation of more than 200 million soaring to 34 percent by the end of the year from 23 percent in 2019.

Other estimates suggest that the unemployment rate could hit 50 percent by 2021. The country’s unemployment rate quickened to a more than six-year high of 23 percent in 2019, the last time the NBS measured the rate.

Rising unemployment and higher inflation has meant the country’s misery index has deteriorated to be almost at par with failed countries from Syria to Lebanon.

As it stands, over 22 million employable Nigerians are out of work and another 15 million are underemployed. There’s little hope that the country can generate sufficient jobs for its people who are forecast to reach 400 million by 2050.

The last time the Nigerian Bureau of Statistics (NBS) published data on job creation it showed the economy added 187,226 new jobs in the third quarter of 2016 after adding 475,180 a year earlier.

As Nigerians get poorer over the course of the next five years, it may also mean more companies, especially small businesses, are at risk of failing as falling consumer purchasing power leads to a reduction in sales and revenues.

Though there is paucity of data on the failure rate among Nigerian start-ups, the one available estimate given by a Nigerian bank Stanbic IBTC claimed that over 80 percent of Nigerian start-ups fail within their first five years.

That will get worse if the economy continues to underperform population growth for another five years.

What experts say is the way out for sluggish economic growth

Jesmin Rahman

Rahman is IMF mission chief to Nigeria. She recommended a raft of fiscal policies that lift per capita GDP growth in Nigeria during a recent webinar hosted by the American Business Council.

Here is what she said: Nigeria has always been to me a fascinating country with huge potential; there’s nothing it doesn’t have. Nigeria has a huge population, and natural resources, yet this is a country that when you compare to its peers on social indicators and living standards, it is not where it should be.

Per capita income used to be $7,000 in mid-1980s since then it has gyrated in sync with oil prices. There are quite a few challenges Nigeria needs to tackle if this course is to be altered. At the current population growth rate of 2.6%, Nigeria’s population is projected at 400 million by 2050. The labor force is growing very rapidly much of which is getting absorbed in either the informal sector or not employed at all. Informal sector wages are very low. Basic literacy among the young population is also very low. Six of out ten out of school children are Nigerians so these are very sobering statistics.

When you look at poverty rate, it is around 40% and given the population projection, by 2030, the World Bank estimates that a fifth of the world’s poorest will be housed in Nigeria. When you add regional dimension, the situation is even scarier because you will the concentration of all of these low statistics in one part of the country.

To turn Nigeria’s population into human capital so the economy grows, Nigeria needs strong job growth and investment in social indicators; education, health and some of the very basic services.

My colleagues in the IMF did a basic estimate of how much it would cost the country to reach the SDGs and they came up with 18% of GDP which would come largely from government even though donor community would help. This reemphasises the importance of growth because without stronger growth to raise revenues, and without those revenues, it would be hard to provide for these very basic and much needed things.

The second challenge is to reduce the dependence on oil. In some ways the Nigerian economy has achieved diversification. Oil only counts for 10% of GDP and 1% of employment so you can say that’s a kind of diversification but the non-oil economy depends heavily on the oil prices through direct and indirect linkages and oil also accounts for 50% fiscal revenues and over 80% of exports. Oil is also important for FX inflows even though remittances help. Because of this, in order to have any form of meaningful diversification, Nigeria needs to move on these fronts as well: diversify fiscal revenues and exports in addition to diversifying GDP base.

Nigeria’s DNA is oil and unless diversification is seen on both fiscal and external fronts, this perception is unlikely to change and this perception needs to change if we are to avoid the big cycles.

Charles Robertson

Robertson, the global chief economist at Renaissance Capital, during a Financial Times summit as far back as 2018, said the country needs to grow by between 4-5 percent for per capita GDP to stop contracting.

“As Nigeria has grown at 2 per cent per capita since 1992, our medium-term base should be at least 4-6 per cent GDP growth,” Robertson said.

But Nigeria cannot match the 4-6 per cent per capita GDP growth of industrialising countries because adult literacy at 60 per cent is too low and electricity consumption is under half the minimum required level for sustained industrialisation, according to Robertson.

“To push headline GDP growth to 6.5-8.5 per cent would require an adult literacy campaign, a trebling of electricity consumption and a doubling of investment to GDP,” Robertson said.

John Ashbourne

Ashbourne, a senior emerging markets economist at economic consulting Capital Economics also shared the following views during the FT summit.

“The government needs to unlock private sector investment by improving the business environment and encouraging participation in the non-oil sector.

The country also desperately needs better infrastructure and reforms to the state-dominated oil sector.”

Razia Khan

Razia Khan, chief Africa economist at Standard Chartered bank also had these to say: “Nigeria has all the necessary building blocks to achieve much faster growth. With its low base, youthful population and scale, a growth rate exceeds the rate of population growth should be easily achievable.

“It needs to develop more institutions that are more resilient than tends to be the case in typical resource economies, for example a tax base independent of oil and a banking sector that can meet the borrowing needs of the private sector. Nigeria has failed to make a transition away from being an oil economy.”

Olusegun Omisakin

Omisakin is the Chief Economist and Director of Research & Development at the Nigerian Economic Summit Group (NESG). His views are as follows: “The effects of COVID-19 pandemic on global health and socio-economic conditions will remain for the foreseeable future.

“For Nigeria, economic policies have to remain broadly expansionary to hasten recovery. Implementation of the Medium-Term National Development Plans (MTNDP) and Nigerian Economic Stimulus Plan (NESP) will quicken the recovery in 2021.

“More focus should also be on improving the business environment through reforms.”