Nigerian President Muhammadu Buhari on Friday assented to the Companies and Allied Matters (CAMA) Bill 2020.

It’s the first reform of the CAMA, one of the most important pieces of business legislation in Africa’s most populous nation, since it was first introduced 30 years ago in 1990.

The 1990 CAMA had become a clog in the wheel of progress for new businesses with outdated laws that complicated the ease of business.

The reforms in the revised CAMA which were championed by the private sector have been widely applauded by the business community and tipped to improve the ease of doing business in Nigeria which ranked 131 of 190 countries surveyed by the World Bank in the 2020 ease of doing business index.

Here are 15 key reforms from the revised CAMA;

The revised CAMA allows single member/shareholder companies to be incorporated in Nigeria. Before now the minimum number of shareholders was two. This will prove particularly beneficial for Micro businesses who are owned by one person and hirtherto restricted from registering or forced to use proxy co-founders or directors. The new practice of single membership aligns with global trends such as in Singapore, India & the UK.

The new CAMA also makes it easier and cheaper for small and medium-sized enterprises to register in Nigeria, by reducing filing fees. The charge is now 0.35 percent of the value of the initial charge.

The new CAMA makes provisions for electronic filing, electronic share transfer and e-meetings for private companies. Certified true copies of electronically-filed documents are now admissible in court; possessing equal validity with the original documents.

The new CAMA also enhances minority shareholder protection, by prohibiting a person from simultaneously holding the positions of Chairman and CEO of a private company. It also prohibits anyone from serving as a director in more than 5 public companies.

The new CAMA allows for the creation of “limited liability partnerships” (LLP) and “limited partnerships” (LP) – which combine the tax benefits of a partnership with the greater liability protection of the owners of a private company. The need for Consent of the Attorney General for companies limited by Guarantee has also been deleted.

The new CAMA now requires the disclosure of persons with significant control/shareholding in companies, as well as the capacity of shareholding, and also nominees of interested persons, in a register of beneficial owners, to enhance corporate accountability and transparency.

The new CAMA permits remote general meetings for private companies. Small companies (as defined by the Act) and single shareholder companies are also now exempted from the requirement of having to hold Annual General Meetings (AGM).

With the new CAMA, having a Company Secretary is now optional for private companies.

Procuring a company seal is no longer a mandatory requirement for companies, in line with international best practice.

The new CAMA replaces authorised share capital with minimum share capital, to reduce the cost of incorporating companies.

Statutory audit of accounts is now optional for Incorporated companies that are yet to commence operations or with turnover of less than N10 million and balance sheet size of not more than N5 million for a financial year. This exempts banks & insurance companies or as prescribed by CAC.

The new CAMA contains rescue provisions for insolvent companies.

Applicants can now sign their statement of compliance and no longer have need for lawyers for the process.

The new law also means Incorporated Trustees can now merge.

CAC has been empowered to cancel name conflicts or fraud, rather than having to go to court.

1. The Federal Executive Council on Wednesday, July 22, 2020, approved the establishment of the Nigerian Youth Investment Fund, N-YIF. The Youth Fund is dedicated to investing in the innovative ideas, skills, talents, and enterprise of the Nigerian Youth and aimed at turning them into Entrepreneurs, Wealth Creators, and Employers of labor contributing to national development. President Buhari led the Federal Government to consider Nigerian youth as a resource to be harnessed and not a problem, hence the initiation of this Fund. 2. The Fund will serve as a catalyst to unleash the potential of the youth and enable many of them to build businesses that will employ and in turn empower others. A multiplier effect of economic expansion and growth required to thrive in an increasingly competitive and connected world where adding value is the only sustainable pathway to success is expected to be achieved.

3. A minimum of N25 billion each year in the next 3 years, totaling N75Billion will be required to ring fence the N-YIF. For the remaining part of 2020 an initial sum of N12.5 billion will be needed to kick start the N-YIF. It is expected that successive governments will keep the Fund, akin to a Youth Bank, alive.

4. The Nigerian Youth Investment Fund (N-YIF) is a ringfenced Fund that will strictly cater to the investment needs of persons between the ages of 18 and 35 years old. It is a restricted Fund that can only be used for the set purpose of Youth Investment.

5. N-YIF joins a slew of Youth-oriented programmes by President Buhari to combat youth unemployment with the objective of driving innovation, fueling the creation of entrepreneurship and support youth SMEs.

6. N-YIF provides a single window of Investment Fund for the youth thereby creating a common bucket for all Nigerian youth to access Government support. Providing a less cumbersome access to credit and finance for the average Nigerian youth with an approved work plan or business idea will help lift thousands of the youth out of poverty and birth a whole generation of entrepreneurs.

7. The fund aims to reach 500,000 youth annually between 2020 and 2023. Each fund approval will range from N250, 000 to N50, 000,000, with a spread across group applications, individual applications, working capital loans set at 1 year and term loans set at 3 years with single digit interest rate of 5%. The funding will be a single digit facility with a moratorium for a year and payable over a designated period. Some businesses may have longer repayment cycles but again the criteria will be clear and appliance to all.

8. Disbursement will be through various channels, which will include Micro Credit Organizations across the country under the Central Bank of Nigeria supported by BOI, Fintech Organizations and Venture Capital Organizations, registered with the CBN.

9. N-YIF will use proven disbursement frameworks but with special conditions with respect to the youth. There will also be a residual advisory facility for applicants and beneficiaries.

10. Usually, Youth funds focus aggressively and singularly on only rapid growth businesses. But N-YIF will invest in businesses that have deeper value than only money. Such businesses must however be viable and able to fulfill all criteria to ensure the fund does continues to expand and serve like a production factory for businesses, but it will encourage creative arts, culture focused businesses because Nigeria needs to start rediscovering the beauty and depth of its culture.

11. The Fund will have a converted analytics framework so that it is possible to see where investments are flowing and calibrate according to the local and global a market demand. The evidence presented in terms of what some amazing youths had achieved locally and globally contributed to the berthing of this fund.

12. Youth seeking to benefit from the fund must have a fundable business idea, registered business, be a citizen of Nigeria, present recognized means of identification and guarantors. The safeguards built around some specifics being crafted around the fund will ensure that potential beneficiaries do not need to know anyone or be “connected” to access the fund. We must prove to our youths that equity is possible regardless of gender, ethnicity or religion. You simply have to be a Nigerian within that bracket with a bankable business plan. Investment will be supported on the strength of the business case and will follow a scoring template and a transparent evaluation process driven largely by technology. We will have a template that will be used to engage and accommodate the not too literate youth who also have brilliant ideas.

The Enugu state Governor, His Excellency, Rt. Hon. Ifeanyi Ugwuanyi, through ENUGU STATE SME Agency have partnered with Lidya (@lidyadotco) to provide collateral-free working capital— Enugu SME Business Support Loan (ESBSL) for SMEs and MSMEs.

You asked for loan, we brought instant access to working capital from your mobile phone!

Remember, this loan are for those that qualify for it. Kindly visit www.enugusme.en.gov.ng/lidya to learn about the Terms and Conditions for the loan and apply.

Signed Hon. Arinze Chilo-Offiah (@Arinze Chilo-Offiah) Special Adviser, SME Development Head, Enugu SME Center

Shares of the Johannesburg-listed Shoprite have soared 10.16 percent in the space of hours from when it released its trading report that contained plans to exit Nigeria.

That’s the retailer’s biggest intraday jump in two months, according to Bloomberg data.

This could be interpreted as investors cheering the retailer’s announcement on Monday to sell all or a majority stake in its supermarkets in Nigeria after 15 years of operations.

It’s easy to see why investors are happy with Shoprite’s move to ditch its recently beleaguered Nigeria operations.

The Nigeria unit has been a drag on Africa’s biggest retailer, despite contributing far less than the South African operations where 78 percent of group sales were made during the year. Shoprite’s supermarkets in South Africa have contributed 75 percent to total group sales in the last five years, according to data compiled by BusinessDay.

To make things worse, sales in the Nigerian supermarkets have been declining since last year while the South African unit has managed to grow sales against the odds.

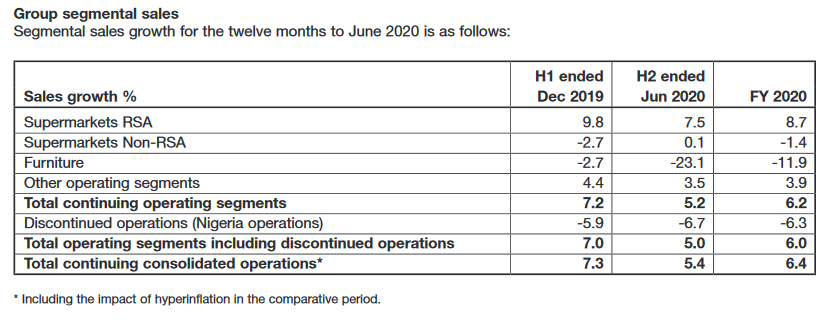

The South African unit saw sales rise by 8.7 percent, but in the Nigerian stores, sales declined by 6.3 percent in 2020. Shoprite’s unique calendar means the year 2020 ended in June.

While sales in Nigeria contracted by 5.9 percent and 6.7 percent in the first and second half of the year respectively, sales in South Africa grew by 9.8 percent and 7.5 percent in the first and second half of the year respectively.

Africa’s two largest economies, Nigeria and South Africa, have both reeled in the past year amid sluggish economic growth that has been compounded by the COVID-19 pandemic. Consumer purchasing power has dwindled in both countries but the data shows Shoprite is faring better in its home country than in Nigeria.

A spin-off of its beleaguered Nigerian operations may put the Group in better financial standing as it eliminates the burden placed on group sales by the Nigerian unit.

Here’s what the company said in its trading report about why it is exiting its Nigerian operations.

“Following approaches from various potential investors, and in line with our re-evaluation of the Group’s operating model in Nigeria, the Board has decided to initiate a formal process to consider the potential sale of all, or a majority stake, in Retail Supermarkets Nigeria Limited, a subsidiary of Shoprite International Limited.

“As such, Retail Supermarkets Nigeria Limited may be classified as a discontinued operation when Shoprite reports its results for the year.”

The company said it would give any further updates at the appropriate time.

The retailer joins Mr. Price, another South African company that recently announced it would also exit Nigeria and focus on the South African domestic market after they closed 4 of the 5 retail outlets in Nigeria.

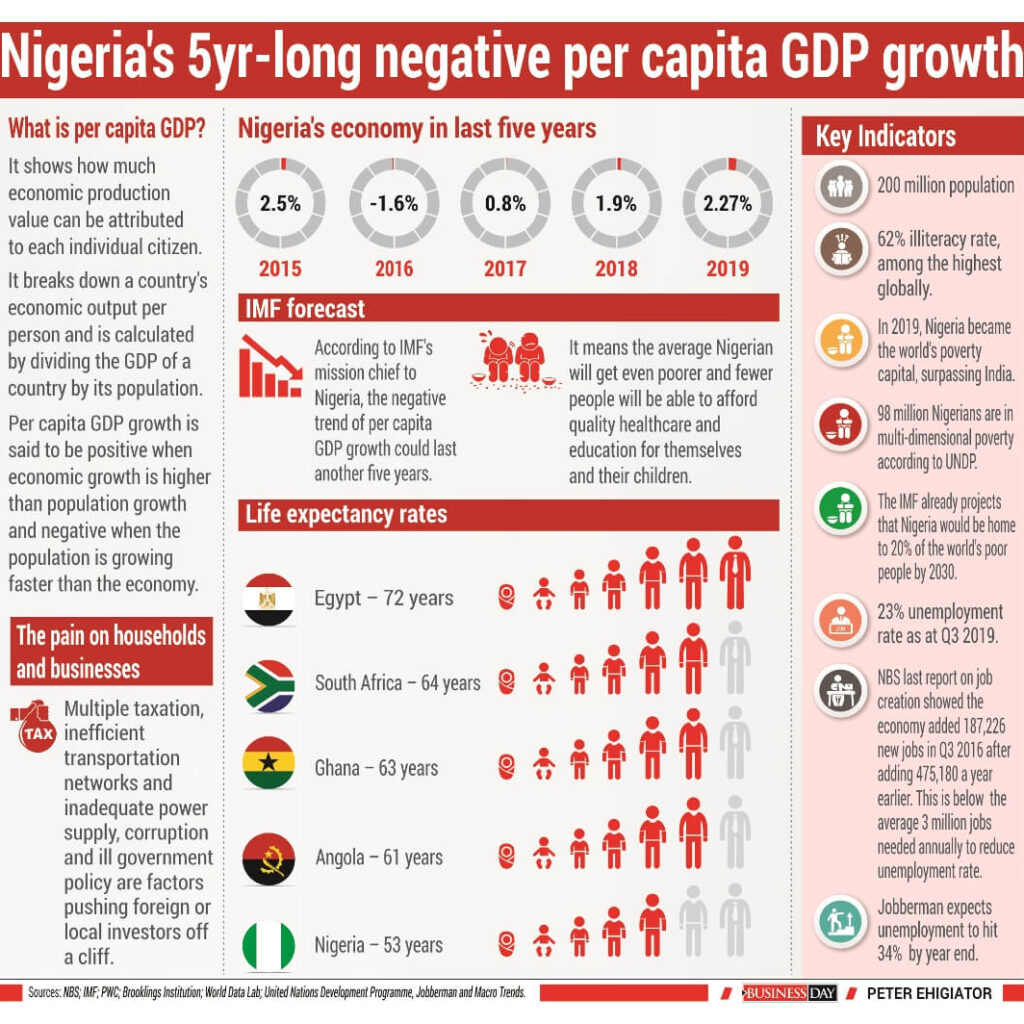

Five straight years of negative Per Capita GDP growth is unprecedented in Nigeria, at least, since the turn of democracy in 1999. But that is what has happened between 2015 and 2019.

For many Nigerians, connecting the dots between five years of an economy not expanding as fast as population is not so straightforward, not with an illiteracy rate of 62 percent, one of the highest globally.

What is unmistakeable, however, is the pain those five years of negative Per Capita GDP has wrecked on households and businesses, whether they understand what is happening or not.

Take the case of Jide Ibrahim (not real name) for example. Ibrahim’s highest qualification is a Bachelor’s degree in Human Kinetics from the Lagos State University (LASU). He worked at Woolworth, a South African clothing retailer, which closed its three stores in Nigeria in 2013.

It is been seven years and he is yet to pin down another job. His lack of job has forced some changes. He has had to move away from his two-bedroom apartment somewhere in Ikorodu to living with a friend in a one-bed apartment almost the size of a telephone booth within the same area.

When asked how he felt when he was laid off, he heaped the blame on Woolworth, saying the company unfairly asked people to leave after milking Nigeria dry.

“These foreign companies just use you and dump you,” Ibrahim said.

Little did he know that his lay off was no fault of Woolworth, but of the high cost of operating a business in Nigeria, which sucked the life out of the South African retailer and sent it scrambling back from where it came.

Hear what Woolworth’s CEO, Ian Moir, said about the exit at the time: “When an investment no longer generates viable returns, difficult decisions have to be made to contain costs.”

High rental costs and duties and complex supply chain processes made trading in Nigeria highly challenging, according to Moir.

Woolworth’s 18-month foray into Nigeria is peculiar for a company that has been operating in South Africa for decades – since 1931 in fact – and has operations in various African countries and elsewhere. The remaining 59 stores in 11 African countries were not affected by the Nigeria decision.

Since that time, Woolworth has expanded to 64 stores and is in 13 African countries.

Woolworth’s experience is not unique; several companies have had to close shop in Nigeria due to the country’s difficult business environment.

Though strides have been made to improve the business environment, the country sits at a lowly 131 of 180 countries surveyed by the World Bank.

Challenges from tax multiplicity to inefficient transportation networks and lack of adequate power have been unbearable to businesses. Over regulation and corruption in government are also chief culprits in pushing businesses, foreign or local, off the cliff.

This shows Ibrahim’s anger should be channelled towards the Nigerian government, which has failed to create an enabling environment for businesses to succeed.

On the evidence of the declining flows of FDI into the country since 2014 and tales of woes by local businesses, the government has not been able to significantly improve the business environment.

Since 2008, when Nigeria attracted a record $8 billion FDI following a wave of privatisation, the country got $3 billion on average between 2009 and 2015, and $1 billion a year since then, according to the NBS, effectively trailing smaller peers like Ghana.

Considering the size of Nigeria’s population, a billion dollars works out to $5 per head.

Foreign companies are not the only businesses to have walked out on Nigeria, even local companies have struggled.

The Manufacturers Association of Nigeria (MAN) said about 272 firms were forced out of business in 2016 alone, 50 of which were manufacturing companies, amid stifling government regulation. The manufacturers say that led to 180,000 job losses in the period.

Surely, Ibrahim and the over 20 million Nigerians without jobs, should hold the government more accountable for the damage done to their lives by bad policies. The lack of jobs has helped poverty thrive.

Nigeria, home to 87 million poor people, became the world’s poverty capital in 2019, overtaking India, according to a Brooklings Institution report.

Another set of statistics by the World Data Lab estimates that 90 million Nigerians live under $1.90 a day, while the United Nations Development Programme reported that 98 million Nigerians were in multi-dimensional poverty.

Yet the pain of a floundering economy growing slower than population also shows it is no respecter of persons. The rich have perhaps suffered just as much.

Take Aliko Dangote, Nigeria’s richest man, who doubles as the continent’s wealthiest person. Dangote is no longer worth half as much as he was in 2014.

Despite remaining the richest African for almost a decade, his fortune is down a staggering 72 percent to $7 billion from $25 billion in 2014, according to Forbes data.

What is Per Capita GDP and why is it important?

At its most basic interpretation, Per Capita GDP shows how much economic production value can be attributed to each individual citizen. It breaks down a country’s economic output per person and is calculated by dividing the GDP of a country by its population.

Per Capita GDP growth is said to be positive when economic growth is higher than population growth and negative when the population is growing faster than the economy.

The per capita metric is a popular measure of the standard of living, prosperity, and overall well-being in a country. A high Per capita GDP indicates a high standard of living while a low one indicates that a country is struggling to supply its inhabitants with everything they need.

Luxembourg, a small European country surrounded by Belgium, France and Germany, has the highest GDP per capita globally with $113,196 as at 2019, according to IMF data.

Switzerland ($83,716) and Norway ($77,975) make up the top three countries with the highest GDP per capita.

On the flip side, war-torn South Sudan ($275), Burundi ($309) and Eritrea ($342) make up countries with the lowest Per Capita GDP in the world. Nigeria ranks 138 with $2,222, behind Ghana with $2,223.

Five years of negative Per capita GDP

Nigeria’s relatively low Per Capita GDP, which paints a dim picture of the living standards in the country, has been worsened by five straight years of contraction.

The last time Nigeria had a positive Per Capita GDP was in 2014, as the economy has struggled since a lengthy collapse in global oil prices that began in mid-2014. When not contracting, the economy has grown at a tepid 2 percent rate compared to average population growth rate of 2.6 percent.

The economy grew 2.5 percent in 2015 before contracting by 1.6 percent in 2016. As oil prices recovered, the economy turned the corner on its first recession in a quarter of a century by growing 0.8 percent in 2017 and a 1.9 percent growth in 2018. In 2019, the economy grew 2.27 percent, capping five years of an economy that didn’t grow fast enough to create new opportunities for a rapidly growing population.

Make it another five years

Prior to the COVID-19 pandemic, the IMF predicted that income per head will continue falling for another three years until at least 2023.

However, with the pandemic, that forecast is grimmer. The trend of negative Per Capita GDP growth could last another five years, according to Jesmin Rahman, the International Monetary Fund’s (IMF) mission chief to Nigeria. That is worse than the initial projection.

“We are going to see the contraction in real Per Capita GDP pick up in the next five years,” Rahman says.

Rahman says it could take Nigeria at least three years before the economy grows at the modest 2 percent rate at which it expanded in 2019 prior to the COVID-19 pandemic.

Another five years of Per Capita GDP contraction is a painful squeeze for a country with gross domestic product per capita of just $2,222, meaning Nigerians will get even poorer than they are now for another five years as their incomes continue to shrink and the economy bleeds jobs.

It means more Nigerians will fall into a poverty pit. The IMF already projects that Nigeria would be home to 20 percent of the world’s poor people by 2030.

Another painful stretch of negative per capita GDP growth also means fewer people will be able to afford quality education for themselves and their children.

For instance, premium primary education alone in Lagos, Nigeria’s commercial capital, could cost anything between N700,000 ($1,944) to N1 million per annum ($2,777). That works out to an average of $2,360 (N849,600), higher than Nigeria’s per capita GDP of $2222.

Fewer people will also be able to afford quality healthcare in a country where the average life expectancy is just 53 years. Only four countries in the world have lower life expectancy rates and they are Sierra-Leone, Chad, Lesotho and Central Africa republic.

South Africa’s life expectancy is 63 years, at par with Ghana’s but lower than the World average of 70 years, according to United Nations World Population data.

Countries like Hong Kong, Japan, Singapore and have an average life expectancy of 83 years.

The job-seeker in Nigeria will also have fewer jobs to compete for with an even larger population of job seekers. Ibrahim may struggle to find a job for another five years.

Data from Jobberman, which recruits mainly white-collar employees and does not track those looking for non-skilled, blue-collar work, sees unemployment in the nation of more than 200 million soaring to 34 percent by the end of the year from 23 percent in 2019.

Other estimates suggest that the unemployment rate could hit 50 percent by 2021. The country’s unemployment rate quickened to a more than six-year high of 23 percent in 2019, the last time the NBS measured the rate.

Rising unemployment and higher inflation has meant the country’s misery index has deteriorated to be almost at par with failed countries from Syria to Lebanon.

As it stands, over 22 million employable Nigerians are out of work and another 15 million are underemployed. There’s little hope that the country can generate sufficient jobs for its people who are forecast to reach 400 million by 2050.

The last time the Nigerian Bureau of Statistics (NBS) published data on job creation it showed the economy added 187,226 new jobs in the third quarter of 2016 after adding 475,180 a year earlier.

As Nigerians get poorer over the course of the next five years, it may also mean more companies, especially small businesses, are at risk of failing as falling consumer purchasing power leads to a reduction in sales and revenues.

Though there is paucity of data on the failure rate among Nigerian start-ups, the one available estimate given by a Nigerian bank Stanbic IBTC claimed that over 80 percent of Nigerian start-ups fail within their first five years.

That will get worse if the economy continues to underperform population growth for another five years.

What experts say is the way out for sluggish economic growth

Jesmin Rahman

Rahman is IMF mission chief to Nigeria. She recommended a raft of fiscal policies that lift per capita GDP growth in Nigeria during a recent webinar hosted by the American Business Council.

Here is what she said: Nigeria has always been to me a fascinating country with huge potential; there’s nothing it doesn’t have. Nigeria has a huge population, and natural resources, yet this is a country that when you compare to its peers on social indicators and living standards, it is not where it should be.

Per capita income used to be $7,000 in mid-1980s since then it has gyrated in sync with oil prices. There are quite a few challenges Nigeria needs to tackle if this course is to be altered. At the current population growth rate of 2.6%, Nigeria’s population is projected at 400 million by 2050. The labor force is growing very rapidly much of which is getting absorbed in either the informal sector or not employed at all. Informal sector wages are very low. Basic literacy among the young population is also very low. Six of out ten out of school children are Nigerians so these are very sobering statistics.

When you look at poverty rate, it is around 40% and given the population projection, by 2030, the World Bank estimates that a fifth of the world’s poorest will be housed in Nigeria. When you add regional dimension, the situation is even scarier because you will the concentration of all of these low statistics in one part of the country.

To turn Nigeria’s population into human capital so the economy grows, Nigeria needs strong job growth and investment in social indicators; education, health and some of the very basic services.

My colleagues in the IMF did a basic estimate of how much it would cost the country to reach the SDGs and they came up with 18% of GDP which would come largely from government even though donor community would help. This reemphasises the importance of growth because without stronger growth to raise revenues, and without those revenues, it would be hard to provide for these very basic and much needed things.

The second challenge is to reduce the dependence on oil. In some ways the Nigerian economy has achieved diversification. Oil only counts for 10% of GDP and 1% of employment so you can say that’s a kind of diversification but the non-oil economy depends heavily on the oil prices through direct and indirect linkages and oil also accounts for 50% fiscal revenues and over 80% of exports. Oil is also important for FX inflows even though remittances help. Because of this, in order to have any form of meaningful diversification, Nigeria needs to move on these fronts as well: diversify fiscal revenues and exports in addition to diversifying GDP base.

Nigeria’s DNA is oil and unless diversification is seen on both fiscal and external fronts, this perception is unlikely to change and this perception needs to change if we are to avoid the big cycles.

Charles Robertson

Robertson, the global chief economist at Renaissance Capital, during a Financial Times summit as far back as 2018, said the country needs to grow by between 4-5 percent for per capita GDP to stop contracting.

“As Nigeria has grown at 2 per cent per capita since 1992, our medium-term base should be at least 4-6 per cent GDP growth,” Robertson said.

But Nigeria cannot match the 4-6 per cent per capita GDP growth of industrialising countries because adult literacy at 60 per cent is too low and electricity consumption is under half the minimum required level for sustained industrialisation, according to Robertson.

“To push headline GDP growth to 6.5-8.5 per cent would require an adult literacy campaign, a trebling of electricity consumption and a doubling of investment to GDP,” Robertson said.

John Ashbourne

Ashbourne, a senior emerging markets economist at economic consulting Capital Economics also shared the following views during the FT summit.

“The government needs to unlock private sector investment by improving the business environment and encouraging participation in the non-oil sector.

The country also desperately needs better infrastructure and reforms to the state-dominated oil sector.”

Razia Khan

Razia Khan, chief Africa economist at Standard Chartered bank also had these to say: “Nigeria has all the necessary building blocks to achieve much faster growth. With its low base, youthful population and scale, a growth rate exceeds the rate of population growth should be easily achievable.

“It needs to develop more institutions that are more resilient than tends to be the case in typical resource economies, for example a tax base independent of oil and a banking sector that can meet the borrowing needs of the private sector. Nigeria has failed to make a transition away from being an oil economy.”

Olusegun Omisakin

Omisakin is the Chief Economist and Director of Research & Development at the Nigerian Economic Summit Group (NESG). His views are as follows: “The effects of COVID-19 pandemic on global health and socio-economic conditions will remain for the foreseeable future.

“For Nigeria, economic policies have to remain broadly expansionary to hasten recovery. Implementation of the Medium-Term National Development Plans (MTNDP) and Nigerian Economic Stimulus Plan (NESP) will quicken the recovery in 2021.

“More focus should also be on improving the business environment through reforms.”

Africa’s largest food retailer, Shoprite Group of Companies, said in its operational and voluntary trading update released on Monday that it will discontinue its operations in Nigeria, 15 years after the company’s first store was opened in Lagos in December 2005. The South African company with more than 2,934 outlets in 15 countries across Africa said a formal process to consider the potential sale of all or a majority stake in its supermarkets in Nigeria has been initiated. The publicly listed company said in a trading statement for the 52 weeks to end June that investors’ interest in its business in Nigeria as well its re-evaluation of the Group’s operating model in the largest economy in Africa are the reasons for wanting to discontinue its operation in Nigeria. “Following approaches from various potential investors, and in line with our re-evaluation of the Group’s operating model in Nigeria, the Board has decided to initiate a formal process to consider the potential sale of all, or a majority stake, in Retail Supermarkets Nigeria Limited,” Shoprite said.

As such, Shoprite said the Retail Supermarkets Nigeria Limited may be classified as a discontinued operation when Shoprite reports its results for the year. It also added that “further updates will be provided to the market at the appropriate time”. Analysis of the Group’s 52 weeks’ trading performance to end June 28, 2020, revealed that sales in Nigeria, Africa’s most populous country, dropped to -6.7 percent in the first half of 2020, a worse performance, when compared to the -5.9 percent reported in the half-year, ended December 2019. In the same period under review, the sales recorded for Shoprite in South Africa stood at 7.5 percent in H1 2020, a 2.3 percentage points decline when compared to the 9.8 percent reported in H1 ended December 2019. “As a result of lockdown, customer visits for the year declined by 7.4 percent (to stores in SA), however, average basket spends increased by 18.4 percent,” the Group said in the trading statement seen by BusinessDay. Meanwhile, Shoprite is not the only South African retailer that has struggled in the Nigerian market as Mr Price had recently exited the market after Woolworths did the same six years ago. To a large extent, the success or failure of businesses mirrors the macroeconomic realities of a country. When businesses thrive, there appears to be economic prosperity in a country and vice versa. For Africa’s largest economy which for a larger part of the last five years has suffered stunted economic growth, the scenario appears not different.

According to analysts, the exit of the South African retailers due to poor market performance mirrors Nigeria’s slow economic growth which has remained lower than the country’s population growth rate in the last five years. Since 2017 when oil-dependent Nigeria emerged from its economic recession, not only has the country’s economic growth been sluggish but only a few sectors triggered the expansion, further undermining the country’s capacity to increase its per capita income level. A survey by BusinessDay shows that the low purchasing power of Nigerians fuelled by the country’s poor economic performance has not only affected South African companies but most firms producing fast-moving consumer goods. Market analysts have unanimously agreed that food manufacturers and fast-moving consumer goods (FMCG) companies had been walking on thin ice before the advent of COVID-19 that ravaged economies across the globe. The number of consumer goods firms that failed to turn a profit in the first half of 2020 jumped to a level that was last seen after the 2016 recession. According to analysts, the downturn caused by the coronavirus pandemic that has disrupted businesses across Nigeria and the country’s underlying economic challenges were the drivers of the companies’ poor performance. “With the harsh operating environment, it is normal to get these kinds of results,” Gbolahan Ologunduro, equity research analyst at CSL Stockbrokers Limited, said. Unilever Nigeria plc recorded a loss of N519.11 million as of June 2020, from 2019’s profit of N3.51 billion – the company’s first loss in five years. The story is the same for International Breweries and Nigerian Breweries as the former posted a loss of N9.35 billion in June 2020 while the latter recorded an operating profit that dipped by 38.85 percent to N24.46 billion in June.

Barring any unforeseen events, the coast is clear for Akinwumi Adesina’s re-election next month as president of African Development Bank (AfDB), following his vindication by an Independent Review Panel that probed his previous exonerations by other organs of the bank.

If not for the coronavirus outbreak, Adesina’s re-election would have been held on May 28, until it was postponed to hold between August 25 and 27, while investigations were concluded. However, the verdict Tuesday, of an Independent Review Panel, which exonerated Adesina of any ethical wrongdoings, had cleared the path for Nigeria’s former minister of agriculture to return to the bank for another five-year term.

The Independent Review Panel set up by Bureau of the Board of Governors of the bank, following a complaint by the United States, had the task of reviewing the process by which two organs of the bank – the Ethics Committee of the Board, and the Bureau of the Board of Governors – had previously exonerated him.

The Independent Review Panel in its report stated that it “concurs with the (Ethics) Committee in its findings in respect of all the allegations against the President and finds that they were properly considered and dismissed by the Committee.”

The Panel also once again vindicated Adesina by stating, “It has considered the President’s submissions on their face and finds them consistent with his innocence and to be persuasive.”

The three-member Independent Review Panel included Mary Robinson, who is a former President of the Republic of Ireland; Hassan B. Jallow, chief justice of the Supreme Court of Gambia, and Leonard F. McCarthy, a former Director of Public Prosecutions in South Africa.

It would be recalled that in January 2020, 16 allegations of ethical misconduct were levelled against Adesina by a group of whistle-blowers. The allegations, which were reviewed by the Bank’s Ethics Committee of the Board of Directors in March, were described as “frivolous and without merit.” The findings and rulings of the Ethics Committee were subsequently upheld by the apex Bureau of the Board of Governors in May, which cleared Adesina of any wrongdoing.

The conclusions of the Independent Review Panel are decisive and now clear the way for Governors of the Bank to re-elect Adesina to a second five-year term as President during annual meetings of the Bank scheduled for August 25-27.

In the weeks following Adesina’s travails, there was a wave of solidarity across the continent, and unsurprisingly from Nigeria, his home country. Olusegun Obasanjo, a former Nigerian president, in a letter to some former leaders on the African continent, had reached out to rally their support for Adesina, also, Zainab Ahmed, Nigeria’s minister of finance, wrote a letter to the chairman of AfDB’s Board of Governors, pointing at external influences undermining the bank’s laid down processes were rejected.

Former President Obasanjo, had in a letter dated May 26, extolled Adesina’s work at the AfDB, saying he had “performed very well in this position over the past five years”. Obasanjo in the letter also stated that Adesina had “taken the bank to great heights. In 2020, he led the bank to achieve a historic general capital increase, raising the capital of the bank from $93bn to $208bn”, further described as the highest in the history of the bank since its establishment in 1964.

He explained that despite these achievements and Adesina’s endorsement for a second term by the whole of Africa, “there are some attempts led by some non-regional member countries of the bank to frustrate his re-election.”

Obasanjo’s letter was copied to Boni Yayi, former President of Benin Republic, Festus Mogae, former President of Botswana; Hailemariam Desalegn, former Prime Minister of Ethiopia; John Kufour, former President of Ghana; Ellen Johnson Sirleaf, former President of Liberia; Joyce Banda, former President of Malawi.

Others are Joaquim Chissano, former President of Mozambique; Tandja Mamadou; former President of Niger; Thabo Mbeki and Kgalema Motlanthe, both former Presidents of South Africa; Benjamin Mkapa and Jakaya Kikwete, both former Presidents of Tanzania; and Mohamed Marzouki; former President of Tunisia.

Ahmed, Nigeria’s minister of finance, on her part wrote Kaba Niala, chairman of AfDB’s Board of Governors, stating that the Nigerian Government had been following developments at the bank closely subsequent to the conclusion and submission of the formal report of the Ethics Committee.

She had protested that the call for an “independent investigation” of Adesina “is outside of the laid down rules, procedures and governing system of the Bank and its Articles as it relates to the Code of Conduct on Ethics for the President”.

While noting that the board of Governors must uphold the rule of law and respect the governance systems of the Bank, Ahmed stated that “If there are any governance issues that need improvement, these can be considered and amendments provided for adoption in line with laid down procedures.”

Crude oil is perhaps the most crucial commodity in the world, with the West Texas Intermediate (WTI) crude being the most traded commodity globally. The reason for this is not farfetched as oil is useful in just about every aspect of the economy, from production to transportation. Therefore, any economy that desires to grow will need oil for its activities.

The oil market might however be a bit confusing for many people who are not energy economists. In this piece, we try to explain the dynamics of the market and how it affects households and businesses from Nigeria to other parts of the world.

Types of Crude oil: How can crude oil be sweet or sour?

There are different varieties and grade of crude oil. Crude oil can be categorised based on viscosity and sulphur. Viscosity measures how light or thick the crude oil is at room temperature. Crude oil is classified as light if it is non-sticky and flows freely at room temperature while it is thick if it is sticky and does not flow freely at room temperature.

Crude oil can also be classified as sweet or sour based on the level of sulphur present in the content of the oil. When the sulphur is low, it means the crude oil is sweet and when the sulphur level in the oil is high, it means the crude oil is sour.

Based on this classification, WTI and Brent crude is light and sweet while Dubai crude is medium-level thick and sour. Another crude oil produced in Nigeria called Bonny Light crude is also light and sweet. Among the types or grades of crude oil, the most popular is the Brent crude. Brent oil is used as a benchmark for the oil market because of the ease at which it can be processed into a product such as petrol. That makes demand for Brent more consistent than others, making it a better indicator for the global oil price.

What has been the trend in crude oil prices in 2020?

The outbreak of the coronavirus has influenced the changes in the price of oil in 2020. The lockdowns, decline in industrial activities and travel restriction resulted in a reduction in the demand for crude oil. Therefore, industries that required crude oil for their operation did not demand much because of a decline in activities. There were also fewer cars on the road as a result of the stringent lockdown measures put in place by the government and jet fuel use was limited as there were travel restrictions. In January, Brent crude oil averaged $63.65 per barrel, but declined to $55.66 in February and further dropping to $32.01 by March as demand plummeted.

The price war between Saudi Arabia and Russia also played a big role in triggering the price downturn. Saudi Arabia could not convince Russia to cut oil production as other OPEC members agreed to do. OPEC decided to cut oil production to reduce oil supply which was running far ahead of demand but Russia, a major oil producer refused to cut back on production. This went on till April when Brent crude dropped to $18.38, the lowest in 18 years.

WTI also plunged to the negative territory for the first time in history, this means that since there was excess supply or production of oil and low demand for the commodity, producers ran out of storage facilities. Therefore, producers had to pay buyers to collect crude oil from them to make available more storage space.

In May, OPEC + after much agitations agreed to cut production to prevent further harm on the world economy. Brent oil price began to rise as world economies around the world re-opened business, coupled with the resumption of air travels.

Ever since May, Crude oil price has been gradually increasing. Brent oil price averaged $29.38 in May, rising to $40.27 per barrel in June and averaging $43.24 per barrel in July 2020.

Why crude oil matters to the Nigerian economy

Crude oil is the major product that earns revenue for Nigeria which implies that Nigeria is an oil dependent economy. Oil accounts for more than 80 per cent of export and foreign exchange earnings. Prior to the discovery of oil, Nigeria’s mainstay source of revenue was agriculture. However, with the discovery of crude oil in 1958, Nigeria shifted attention away from agriculture to crude oil.

However, because Nigeria relies heavily on the proceeds of crude oil, the state of the economy is dictated by the state of the price of crude oil and unfortunately, the price of crude oil is unstable. Nigeria is a net oil-exporting country. Nigeria both exports crude oil and imports the refined crude oil products (such as petroleum, kerosene, diesel, liquefied petroleum gas). During times where the price of crude of crude oil is high, then the economy is usually vibrant and at times when the price of crude oil is low, the economy shrinks.

There are certain economic indicators that reveal the health of an economy. These indicators are called macroeconomic variables, some of which include gross domestic products (GDP), inflation, unemployment and exchange rate. These indicators will show at a glance whether a nation is doing well or not.

When there is a fall in crude oil price in Nigeria, government revenue declines which in turn causes government expenditure to fall. This will result in a fall in economic activities or production hereby causing GDP to decline. The GDP is the total value of goods produced and services provided in a country during one year. As a result of the reliance on crude oil proceeds, when the price of crude oil fall, oil revenue and other indicators are also affected.

For instance, between 2014 and 2016, crude oil price crashed from $100.85 to $43.74. After the crash, Nigeria crude oil revenue fell from 6.997 trillion in 2016 to 4.1 trillion in 2017. As oil price increased from $54.71 in 2017 to $71.34 in 2018, consequently, crude oil revenue rose from 4.1 trillion in 2017 to as high as 9.4 trillion in 2018 according to CBN.

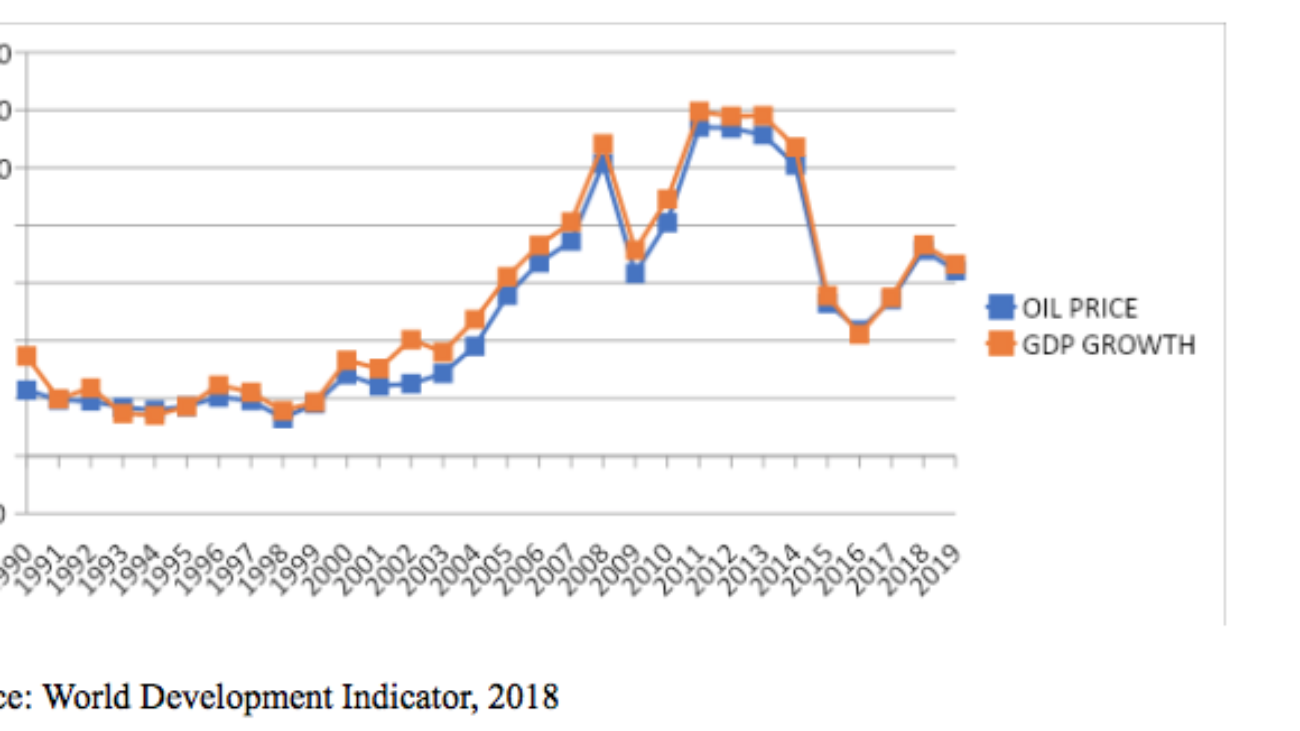

The figure below shows the trend of oil movement and GDP changes in Nigeria from 1990 to 2019. The graph shows that the growth rate of Nigeria and the oil price move together in the same direction. This implies that when oil price increases, the GDP experiences a boom also and when oil price drops, GDP also drops.

Source: World Development Indicator, 2018

This shows that the oil price dictates whether the Nigerian economy grows or not and since the price of oil is determined by factors outside the control of the country, it means Nigeria is at the mercy of whatever happens to oil price.

Nigeria benefited from the rising oil price from the year 2000 to 2007. During this period, oil price increased from $28.42 in 2000 to $74 U.S dollars in 2007. Consequently, the growth rates in Nigeria also show a rising trend.

There was an unexpected drop in oil price in 2014, oil price declined from $100.85 in 2014 to $43.74 in 2016, the growth rate also declined from 6.3 per cent in 2014 to -1.61 per cent sending the economy into a recession.

A recession is characterised by falling GDP, low production/manufacturing activities, rising unemployment, and falling prices of goods and services. Nigeria entered into a recession when the GDP growth rate for the second quarter of 2016 came out negative.

As earlier stated, when the GDP of a country is affected, all other indicators also will perform poorly. For instance, in 2016 when the GDP of Nigeria turned negative, inflation rate rose from 13.9% in the second quarter of 2016 to 14.2% in the last quarter of 2016. By 2017, inflation rose to 18.8% in the third quarter according to data from the National Bureau of Statistics (NBS). When inflation increases, it means the prices of goods and services would increase, hereby creating economic hardship.

The NBS also published data revealing that unemployment rate in Nigeria rose from 12.1% to 13.9% in the first and second quarter in 2016 respectively and by the last quarter of 2016, unemployment rate increased to 14.2%. This shows that oil movement influences the macroeconomic stability of oil dependent countries like Nigeria.

Inflation and unemployment increase during recession because of low economic activities. Firms lay off workers and employ less in order to cover their cost of operation.

The outbreak of the corona virus in 2020 has had severe consequences on the Nigerian economy in the last few months. While Nigeria was still dealing with the pandemic in its early stage, there was a sudden crash in the price of crude oil as a result of the price war between Saudi Arabia and Russia. Oil price which closed at about $60 per barrel as at December 2019 fell to as low as $18 per barrel as at April 2020. This twin shock further weakened the already fragile economy. Inflation rate increased from 12.26 percent in March to 12.34 percent in April, further rising to 12.40 by May and by June it stood a 12.56 per cent according to NBS.

How does oil price movement affects household and businesses in Nigeria?

Consumers and firms are not exempted from the influence of oil price movements. Recall that Nigeria is a major oil exporter and depends largely on crude oil sales for revenue. Therefore, a higher oil price is good news for the economy because export revenue will increase. The increase in revenue means the government is better able to implement its budget whether it’s paying workers’ salaries or implementing capital projects.

Consumers tend to spend more in a period of oil price booms, which is characterised by stable incomes and creation of direct and indirect jobs. Their demand for goods and services tend to rise in this period. The firms on the other hand will benefit from increased consumer spending which translates to higher sales of their products and services.

Conversely, when oil prices decline, there will be a decrease in export revenue and government expenditure. Lower oil prices also put the exchange rate at risk as it exposes the naira to pressure against the dollar. Given that oil exports account for over 80 percent of foreign exchange inflows into Nigeria, a period of low oil prices tends to lead to dollar shortages, naira devaluation and higher inflation. A devaluation of the naira is bad news for households and businesses as it often leads to higher inflation. Many manufacturers rely on imports to produce, so when the exchange rate weakens it means higher production costs for them and that is mostly followed by a hike in the price of the goods they sell which is negative for consumers.

The higher inflation triggered by an exchange rate depreciation squeezes households who are left to contend with lower purchasing power in the face of more expensive goods and services. This implies that households will have less income to spend on goods and services, therefore they will demand less.

The firms will also have less access to funds for investment and could lay off workers in an attempt to cover their operating costs. When firms cut back on expansion, it translates to lower economic growth.

Need for diversification

All the above prove that the Nigerian economy will continue experiencing macro-economic instability until it can find a way to depend less on oil sales for its revenue.

The government will need to invest more in the health and education of the Nigerian citizens. According to the United Nation Children’s Funds (UNICEF) in 2019, there are about 10.5 million out of school children in Nigeria and there are also those who are in school but receive substandard education. Bill Gates, the co-founder of the Bill and Melinda Foundation during his visit to Nigeria in 2018 said the only way Nigeria can escape poverty and enjoy sustained prosperity is by investing in the health and education of the people. He also stated that the life expectancy in Nigeria is one of the worst in the world. ‘‘The most important choice the government can make is to maximize its greatest resources, the Nigerian people. Nigeria will thrive when every Nigeria is able to thrive’’ He said.

The inadequate infrastructure in Nigeria would also make diversification difficult. The World Economic Forum Global Competitiveness Index in 2018 reported that Nigeria ranks 132 out of 137 in the quality of overall infrastructure, 127 out of 137 in quality roads and 136 0ut of 137 in quality of electricity supply. Productivity will only increase when the necessary infrastructure is in place.

The agricultural sector is also a viable sector. The increase in agricultural activities will invariably lead to the development of other sectors that have linkages to the agricultural sector such as the manufacturing and textile industries due to the supply of raw materials from agriculture to feed these industries. The tourism industry is another viable industry that could be harnessed to drive economic diversification since Nigeria is endowed with rich natural ecosystems and cultural diversity.

The telecommunication industry in Nigeria has one of the largest telecoms in Africa. The effective exploitation of this sector will bring about efficiency and productivity in the telecom sector and eventually enhance economic growth.

As part of the Job Creation Schemes, the Enugu Fenix Power Champions under the Human Capital Development Loan, championed by His Excellency, Rt. Hon. Ifeanyi Ugwuanyi, was officially flagged off today, 28th July, 2020 at the Enugu SME Center under the leadership of Hon. Arinze Chilo-Offiah as he presents the 1st Batch of the Enugu Fenix Power Champions.

They have been trained and fully equipped to begin sales.

Enugu SME Center is creating jobs for ndi Enugu even in the covid-19 pandemic.

Signed Hon. Arinze Chilo-Offiah Special Adviser, SME Development Head, Enugu SME Center

Again, the need for inter-African trade has been stressed by the World Bank as it says the African Continental Free Trade Area (AfCFTA) could boost regional income by 7 percent or $450 billion, speed up wage growth for women, and lift 30 million people out of extreme poverty by 2035, if implemented fully.

The World Bank said in a new report on Monday.

In addition, experts say the trade pact will position Nigeria’s firm to compete better in the continental and global markets.

AfCFTA represents a major opportunity for countries to boost growth, reduce poverty, and broaden economic inclusion.

The report suggests that achieving these gains will be particularly important given the economic damage caused by the COVID-19 (coronavirus) pandemic, which is expected to cause up to $79 billion in output losses in Africa in 2020. The pandemic has already caused major disruptions to trade across the continent, including in critical goods such as medical supplies and food.

Most of AfCFTA’s income gains are likely to come from measures that cut red tape and simplify customs procedures. Tariff liberalisation accompanied by a reduction in non-tariff barriers—such as quotas and rules of origin—would boost income by 2.4 percent, or about $153 billion.

The remainder—$292 billion—would come from trade-facilitation measures that reduce red tape, lower compliance costs for businesses engaged in trade, and make it easier for African businesses to integrate into global supply chains.

It could be recalled that initially, the Manufacturers Association of Nigeria (MAN) was the biggest opposition to the AfCFTA, arguing that ratifying the agreement could kill industries in Nigeria. MAN had said it was important for Nigeria to position local manufacturers for competitiveness first before ratifying the AfCFTA.

However, the association later made a U-turn, saying African nations needed to trade more with one another.

“MAN recognises the imperativeness of creating a beneficial free trade area for export of the products of members and has strongly worked assiduously to promote the articulation of evidence-based positions on AfCFTA,” Mansur Ahmed, president of MAN, said at a South-West sensitisation workshop in Lagos in February 2020.

The Lagos Chamber of Commerce and Industry (LCCI) is backing the trade deal, arguing that if smaller African countries are not afraid of it, Nigeria with 200 million people and humongous $430 billion GDP, must grab it with both hands.

Muda Yusuf, director-general, LCCI, told BusinessDay in 2019 that multinationals would be the biggest beneficiaries when the AfCFTA started.

“Mostly multinationals and large enterprises are in a better position to gain from AfCFTA because their economies of scale will improve. They have the big market and the capacity,” Yusuf had said.

“The continental trade is more about economies of scale and the amount of what you produce. The higher you produce, the lower the unit cost, which is why small companies will benefit but not as much as large firms,” he further said.

AfCFTA seeks to liberalise trade among African countries. It is targeted at a ‘borderless’ Africa, with an eye on a single market for goods and services on the continent. It was supposed to start in July 1, 2020, but has been postponed to January 2021 owing to COVID-19 pandemic.

Experts believe AfCFTA is easily the largest trade agreement since the World Trade Organisation (WTO) in 1994 and a flagship project of Africa’s Agenda 2063, targeted at creating a single market for 1.2 billion people and exposing each country to a $3.4 trillion market opportunity on the continent.

The AfCFTA is expected to raise Africa’s nominal GDP to $6.7 trillion by 2030 if all the countries sign up.

The treaty liberalises 90 percent of products manufactured in Africa, meaning that a country can only protect 10 percent of its local industries.

Bismark Rewane, CEO, Financial Derivatives, said the AfCFTA would favour Nigeria, Kenya, Egypt and Ghana, among others, but warned that any government that was not effective would fail within the AfCFTA environment.

“Nigeria will benefit. But it will forced to be effective because if not, people can easily go to Cotonou to set up plants,” he told Channels TV in 2019, adding that government failures would be glaring under the trade arrangement.