1. The Federal Executive Council on Wednesday, July 22, 2020, approved the establishment of the Nigerian Youth Investment Fund, N-YIF. The Youth Fund is dedicated to investing in the innovative ideas, skills, talents, and enterprise of the Nigerian Youth and aimed at turning them into Entrepreneurs, Wealth Creators, and Employers of labor contributing to national development. President Buhari led the Federal Government to consider Nigerian youth as a resource to be harnessed and not a problem, hence the initiation of this Fund. 2. The Fund will serve as a catalyst to unleash the potential of the youth and enable many of them to build businesses that will employ and in turn empower others. A multiplier effect of economic expansion and growth required to thrive in an increasingly competitive and connected world where adding value is the only sustainable pathway to success is expected to be achieved.

3. A minimum of N25 billion each year in the next 3 years, totaling N75Billion will be required to ring fence the N-YIF. For the remaining part of 2020 an initial sum of N12.5 billion will be needed to kick start the N-YIF. It is expected that successive governments will keep the Fund, akin to a Youth Bank, alive.

4. The Nigerian Youth Investment Fund (N-YIF) is a ringfenced Fund that will strictly cater to the investment needs of persons between the ages of 18 and 35 years old. It is a restricted Fund that can only be used for the set purpose of Youth Investment.

5. N-YIF joins a slew of Youth-oriented programmes by President Buhari to combat youth unemployment with the objective of driving innovation, fueling the creation of entrepreneurship and support youth SMEs.

6. N-YIF provides a single window of Investment Fund for the youth thereby creating a common bucket for all Nigerian youth to access Government support. Providing a less cumbersome access to credit and finance for the average Nigerian youth with an approved work plan or business idea will help lift thousands of the youth out of poverty and birth a whole generation of entrepreneurs.

7. The fund aims to reach 500,000 youth annually between 2020 and 2023. Each fund approval will range from N250, 000 to N50, 000,000, with a spread across group applications, individual applications, working capital loans set at 1 year and term loans set at 3 years with single digit interest rate of 5%. The funding will be a single digit facility with a moratorium for a year and payable over a designated period. Some businesses may have longer repayment cycles but again the criteria will be clear and appliance to all.

8. Disbursement will be through various channels, which will include Micro Credit Organizations across the country under the Central Bank of Nigeria supported by BOI, Fintech Organizations and Venture Capital Organizations, registered with the CBN.

9. N-YIF will use proven disbursement frameworks but with special conditions with respect to the youth. There will also be a residual advisory facility for applicants and beneficiaries.

10. Usually, Youth funds focus aggressively and singularly on only rapid growth businesses. But N-YIF will invest in businesses that have deeper value than only money. Such businesses must however be viable and able to fulfill all criteria to ensure the fund does continues to expand and serve like a production factory for businesses, but it will encourage creative arts, culture focused businesses because Nigeria needs to start rediscovering the beauty and depth of its culture.

11. The Fund will have a converted analytics framework so that it is possible to see where investments are flowing and calibrate according to the local and global a market demand. The evidence presented in terms of what some amazing youths had achieved locally and globally contributed to the berthing of this fund.

12. Youth seeking to benefit from the fund must have a fundable business idea, registered business, be a citizen of Nigeria, present recognized means of identification and guarantors. The safeguards built around some specifics being crafted around the fund will ensure that potential beneficiaries do not need to know anyone or be “connected” to access the fund. We must prove to our youths that equity is possible regardless of gender, ethnicity or religion. You simply have to be a Nigerian within that bracket with a bankable business plan. Investment will be supported on the strength of the business case and will follow a scoring template and a transparent evaluation process driven largely by technology. We will have a template that will be used to engage and accommodate the not too literate youth who also have brilliant ideas.

Shares of the Johannesburg-listed Shoprite have soared 10.16 percent in the space of hours from when it released its trading report that contained plans to exit Nigeria.

That’s the retailer’s biggest intraday jump in two months, according to Bloomberg data.

This could be interpreted as investors cheering the retailer’s announcement on Monday to sell all or a majority stake in its supermarkets in Nigeria after 15 years of operations.

It’s easy to see why investors are happy with Shoprite’s move to ditch its recently beleaguered Nigeria operations.

The Nigeria unit has been a drag on Africa’s biggest retailer, despite contributing far less than the South African operations where 78 percent of group sales were made during the year. Shoprite’s supermarkets in South Africa have contributed 75 percent to total group sales in the last five years, according to data compiled by BusinessDay.

To make things worse, sales in the Nigerian supermarkets have been declining since last year while the South African unit has managed to grow sales against the odds.

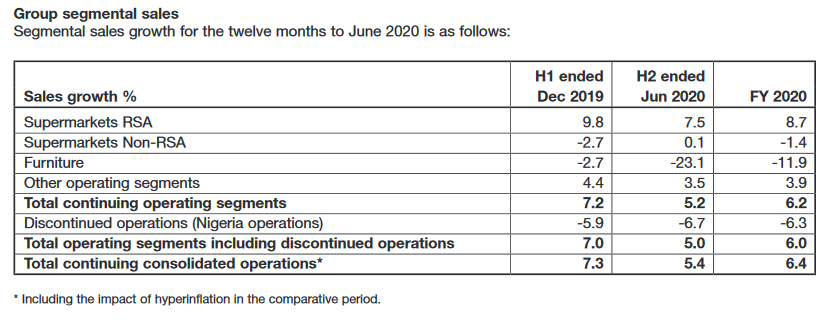

The South African unit saw sales rise by 8.7 percent, but in the Nigerian stores, sales declined by 6.3 percent in 2020. Shoprite’s unique calendar means the year 2020 ended in June.

While sales in Nigeria contracted by 5.9 percent and 6.7 percent in the first and second half of the year respectively, sales in South Africa grew by 9.8 percent and 7.5 percent in the first and second half of the year respectively.

Africa’s two largest economies, Nigeria and South Africa, have both reeled in the past year amid sluggish economic growth that has been compounded by the COVID-19 pandemic. Consumer purchasing power has dwindled in both countries but the data shows Shoprite is faring better in its home country than in Nigeria.

A spin-off of its beleaguered Nigerian operations may put the Group in better financial standing as it eliminates the burden placed on group sales by the Nigerian unit.

Here’s what the company said in its trading report about why it is exiting its Nigerian operations.

“Following approaches from various potential investors, and in line with our re-evaluation of the Group’s operating model in Nigeria, the Board has decided to initiate a formal process to consider the potential sale of all, or a majority stake, in Retail Supermarkets Nigeria Limited, a subsidiary of Shoprite International Limited.

“As such, Retail Supermarkets Nigeria Limited may be classified as a discontinued operation when Shoprite reports its results for the year.”

The company said it would give any further updates at the appropriate time.

The retailer joins Mr. Price, another South African company that recently announced it would also exit Nigeria and focus on the South African domestic market after they closed 4 of the 5 retail outlets in Nigeria.

Africa’s largest food retailer, Shoprite Group of Companies, said in its operational and voluntary trading update released on Monday that it will discontinue its operations in Nigeria, 15 years after the company’s first store was opened in Lagos in December 2005. The South African company with more than 2,934 outlets in 15 countries across Africa said a formal process to consider the potential sale of all or a majority stake in its supermarkets in Nigeria has been initiated. The publicly listed company said in a trading statement for the 52 weeks to end June that investors’ interest in its business in Nigeria as well its re-evaluation of the Group’s operating model in the largest economy in Africa are the reasons for wanting to discontinue its operation in Nigeria. “Following approaches from various potential investors, and in line with our re-evaluation of the Group’s operating model in Nigeria, the Board has decided to initiate a formal process to consider the potential sale of all, or a majority stake, in Retail Supermarkets Nigeria Limited,” Shoprite said.

As such, Shoprite said the Retail Supermarkets Nigeria Limited may be classified as a discontinued operation when Shoprite reports its results for the year. It also added that “further updates will be provided to the market at the appropriate time”. Analysis of the Group’s 52 weeks’ trading performance to end June 28, 2020, revealed that sales in Nigeria, Africa’s most populous country, dropped to -6.7 percent in the first half of 2020, a worse performance, when compared to the -5.9 percent reported in the half-year, ended December 2019. In the same period under review, the sales recorded for Shoprite in South Africa stood at 7.5 percent in H1 2020, a 2.3 percentage points decline when compared to the 9.8 percent reported in H1 ended December 2019. “As a result of lockdown, customer visits for the year declined by 7.4 percent (to stores in SA), however, average basket spends increased by 18.4 percent,” the Group said in the trading statement seen by BusinessDay. Meanwhile, Shoprite is not the only South African retailer that has struggled in the Nigerian market as Mr Price had recently exited the market after Woolworths did the same six years ago. To a large extent, the success or failure of businesses mirrors the macroeconomic realities of a country. When businesses thrive, there appears to be economic prosperity in a country and vice versa. For Africa’s largest economy which for a larger part of the last five years has suffered stunted economic growth, the scenario appears not different.

According to analysts, the exit of the South African retailers due to poor market performance mirrors Nigeria’s slow economic growth which has remained lower than the country’s population growth rate in the last five years. Since 2017 when oil-dependent Nigeria emerged from its economic recession, not only has the country’s economic growth been sluggish but only a few sectors triggered the expansion, further undermining the country’s capacity to increase its per capita income level. A survey by BusinessDay shows that the low purchasing power of Nigerians fuelled by the country’s poor economic performance has not only affected South African companies but most firms producing fast-moving consumer goods. Market analysts have unanimously agreed that food manufacturers and fast-moving consumer goods (FMCG) companies had been walking on thin ice before the advent of COVID-19 that ravaged economies across the globe. The number of consumer goods firms that failed to turn a profit in the first half of 2020 jumped to a level that was last seen after the 2016 recession. According to analysts, the downturn caused by the coronavirus pandemic that has disrupted businesses across Nigeria and the country’s underlying economic challenges were the drivers of the companies’ poor performance. “With the harsh operating environment, it is normal to get these kinds of results,” Gbolahan Ologunduro, equity research analyst at CSL Stockbrokers Limited, said. Unilever Nigeria plc recorded a loss of N519.11 million as of June 2020, from 2019’s profit of N3.51 billion – the company’s first loss in five years. The story is the same for International Breweries and Nigerian Breweries as the former posted a loss of N9.35 billion in June 2020 while the latter recorded an operating profit that dipped by 38.85 percent to N24.46 billion in June.

Barring any unforeseen events, the coast is clear for Akinwumi Adesina’s re-election next month as president of African Development Bank (AfDB), following his vindication by an Independent Review Panel that probed his previous exonerations by other organs of the bank.

If not for the coronavirus outbreak, Adesina’s re-election would have been held on May 28, until it was postponed to hold between August 25 and 27, while investigations were concluded. However, the verdict Tuesday, of an Independent Review Panel, which exonerated Adesina of any ethical wrongdoings, had cleared the path for Nigeria’s former minister of agriculture to return to the bank for another five-year term.

The Independent Review Panel set up by Bureau of the Board of Governors of the bank, following a complaint by the United States, had the task of reviewing the process by which two organs of the bank – the Ethics Committee of the Board, and the Bureau of the Board of Governors – had previously exonerated him.

The Independent Review Panel in its report stated that it “concurs with the (Ethics) Committee in its findings in respect of all the allegations against the President and finds that they were properly considered and dismissed by the Committee.”

The Panel also once again vindicated Adesina by stating, “It has considered the President’s submissions on their face and finds them consistent with his innocence and to be persuasive.”

The three-member Independent Review Panel included Mary Robinson, who is a former President of the Republic of Ireland; Hassan B. Jallow, chief justice of the Supreme Court of Gambia, and Leonard F. McCarthy, a former Director of Public Prosecutions in South Africa.

It would be recalled that in January 2020, 16 allegations of ethical misconduct were levelled against Adesina by a group of whistle-blowers. The allegations, which were reviewed by the Bank’s Ethics Committee of the Board of Directors in March, were described as “frivolous and without merit.” The findings and rulings of the Ethics Committee were subsequently upheld by the apex Bureau of the Board of Governors in May, which cleared Adesina of any wrongdoing.

The conclusions of the Independent Review Panel are decisive and now clear the way for Governors of the Bank to re-elect Adesina to a second five-year term as President during annual meetings of the Bank scheduled for August 25-27.

In the weeks following Adesina’s travails, there was a wave of solidarity across the continent, and unsurprisingly from Nigeria, his home country. Olusegun Obasanjo, a former Nigerian president, in a letter to some former leaders on the African continent, had reached out to rally their support for Adesina, also, Zainab Ahmed, Nigeria’s minister of finance, wrote a letter to the chairman of AfDB’s Board of Governors, pointing at external influences undermining the bank’s laid down processes were rejected.

Former President Obasanjo, had in a letter dated May 26, extolled Adesina’s work at the AfDB, saying he had “performed very well in this position over the past five years”. Obasanjo in the letter also stated that Adesina had “taken the bank to great heights. In 2020, he led the bank to achieve a historic general capital increase, raising the capital of the bank from $93bn to $208bn”, further described as the highest in the history of the bank since its establishment in 1964.

He explained that despite these achievements and Adesina’s endorsement for a second term by the whole of Africa, “there are some attempts led by some non-regional member countries of the bank to frustrate his re-election.”

Obasanjo’s letter was copied to Boni Yayi, former President of Benin Republic, Festus Mogae, former President of Botswana; Hailemariam Desalegn, former Prime Minister of Ethiopia; John Kufour, former President of Ghana; Ellen Johnson Sirleaf, former President of Liberia; Joyce Banda, former President of Malawi.

Others are Joaquim Chissano, former President of Mozambique; Tandja Mamadou; former President of Niger; Thabo Mbeki and Kgalema Motlanthe, both former Presidents of South Africa; Benjamin Mkapa and Jakaya Kikwete, both former Presidents of Tanzania; and Mohamed Marzouki; former President of Tunisia.

Ahmed, Nigeria’s minister of finance, on her part wrote Kaba Niala, chairman of AfDB’s Board of Governors, stating that the Nigerian Government had been following developments at the bank closely subsequent to the conclusion and submission of the formal report of the Ethics Committee.

She had protested that the call for an “independent investigation” of Adesina “is outside of the laid down rules, procedures and governing system of the Bank and its Articles as it relates to the Code of Conduct on Ethics for the President”.

While noting that the board of Governors must uphold the rule of law and respect the governance systems of the Bank, Ahmed stated that “If there are any governance issues that need improvement, these can be considered and amendments provided for adoption in line with laid down procedures.”

Crude oil is perhaps the most crucial commodity in the world, with the West Texas Intermediate (WTI) crude being the most traded commodity globally. The reason for this is not farfetched as oil is useful in just about every aspect of the economy, from production to transportation. Therefore, any economy that desires to grow will need oil for its activities.

The oil market might however be a bit confusing for many people who are not energy economists. In this piece, we try to explain the dynamics of the market and how it affects households and businesses from Nigeria to other parts of the world.

Types of Crude oil: How can crude oil be sweet or sour?

There are different varieties and grade of crude oil. Crude oil can be categorised based on viscosity and sulphur. Viscosity measures how light or thick the crude oil is at room temperature. Crude oil is classified as light if it is non-sticky and flows freely at room temperature while it is thick if it is sticky and does not flow freely at room temperature.

Crude oil can also be classified as sweet or sour based on the level of sulphur present in the content of the oil. When the sulphur is low, it means the crude oil is sweet and when the sulphur level in the oil is high, it means the crude oil is sour.

Based on this classification, WTI and Brent crude is light and sweet while Dubai crude is medium-level thick and sour. Another crude oil produced in Nigeria called Bonny Light crude is also light and sweet. Among the types or grades of crude oil, the most popular is the Brent crude. Brent oil is used as a benchmark for the oil market because of the ease at which it can be processed into a product such as petrol. That makes demand for Brent more consistent than others, making it a better indicator for the global oil price.

What has been the trend in crude oil prices in 2020?

The outbreak of the coronavirus has influenced the changes in the price of oil in 2020. The lockdowns, decline in industrial activities and travel restriction resulted in a reduction in the demand for crude oil. Therefore, industries that required crude oil for their operation did not demand much because of a decline in activities. There were also fewer cars on the road as a result of the stringent lockdown measures put in place by the government and jet fuel use was limited as there were travel restrictions. In January, Brent crude oil averaged $63.65 per barrel, but declined to $55.66 in February and further dropping to $32.01 by March as demand plummeted.

The price war between Saudi Arabia and Russia also played a big role in triggering the price downturn. Saudi Arabia could not convince Russia to cut oil production as other OPEC members agreed to do. OPEC decided to cut oil production to reduce oil supply which was running far ahead of demand but Russia, a major oil producer refused to cut back on production. This went on till April when Brent crude dropped to $18.38, the lowest in 18 years.

WTI also plunged to the negative territory for the first time in history, this means that since there was excess supply or production of oil and low demand for the commodity, producers ran out of storage facilities. Therefore, producers had to pay buyers to collect crude oil from them to make available more storage space.

In May, OPEC + after much agitations agreed to cut production to prevent further harm on the world economy. Brent oil price began to rise as world economies around the world re-opened business, coupled with the resumption of air travels.

Ever since May, Crude oil price has been gradually increasing. Brent oil price averaged $29.38 in May, rising to $40.27 per barrel in June and averaging $43.24 per barrel in July 2020.

Why crude oil matters to the Nigerian economy

Crude oil is the major product that earns revenue for Nigeria which implies that Nigeria is an oil dependent economy. Oil accounts for more than 80 per cent of export and foreign exchange earnings. Prior to the discovery of oil, Nigeria’s mainstay source of revenue was agriculture. However, with the discovery of crude oil in 1958, Nigeria shifted attention away from agriculture to crude oil.

However, because Nigeria relies heavily on the proceeds of crude oil, the state of the economy is dictated by the state of the price of crude oil and unfortunately, the price of crude oil is unstable. Nigeria is a net oil-exporting country. Nigeria both exports crude oil and imports the refined crude oil products (such as petroleum, kerosene, diesel, liquefied petroleum gas). During times where the price of crude of crude oil is high, then the economy is usually vibrant and at times when the price of crude oil is low, the economy shrinks.

There are certain economic indicators that reveal the health of an economy. These indicators are called macroeconomic variables, some of which include gross domestic products (GDP), inflation, unemployment and exchange rate. These indicators will show at a glance whether a nation is doing well or not.

When there is a fall in crude oil price in Nigeria, government revenue declines which in turn causes government expenditure to fall. This will result in a fall in economic activities or production hereby causing GDP to decline. The GDP is the total value of goods produced and services provided in a country during one year. As a result of the reliance on crude oil proceeds, when the price of crude oil fall, oil revenue and other indicators are also affected.

For instance, between 2014 and 2016, crude oil price crashed from $100.85 to $43.74. After the crash, Nigeria crude oil revenue fell from 6.997 trillion in 2016 to 4.1 trillion in 2017. As oil price increased from $54.71 in 2017 to $71.34 in 2018, consequently, crude oil revenue rose from 4.1 trillion in 2017 to as high as 9.4 trillion in 2018 according to CBN.

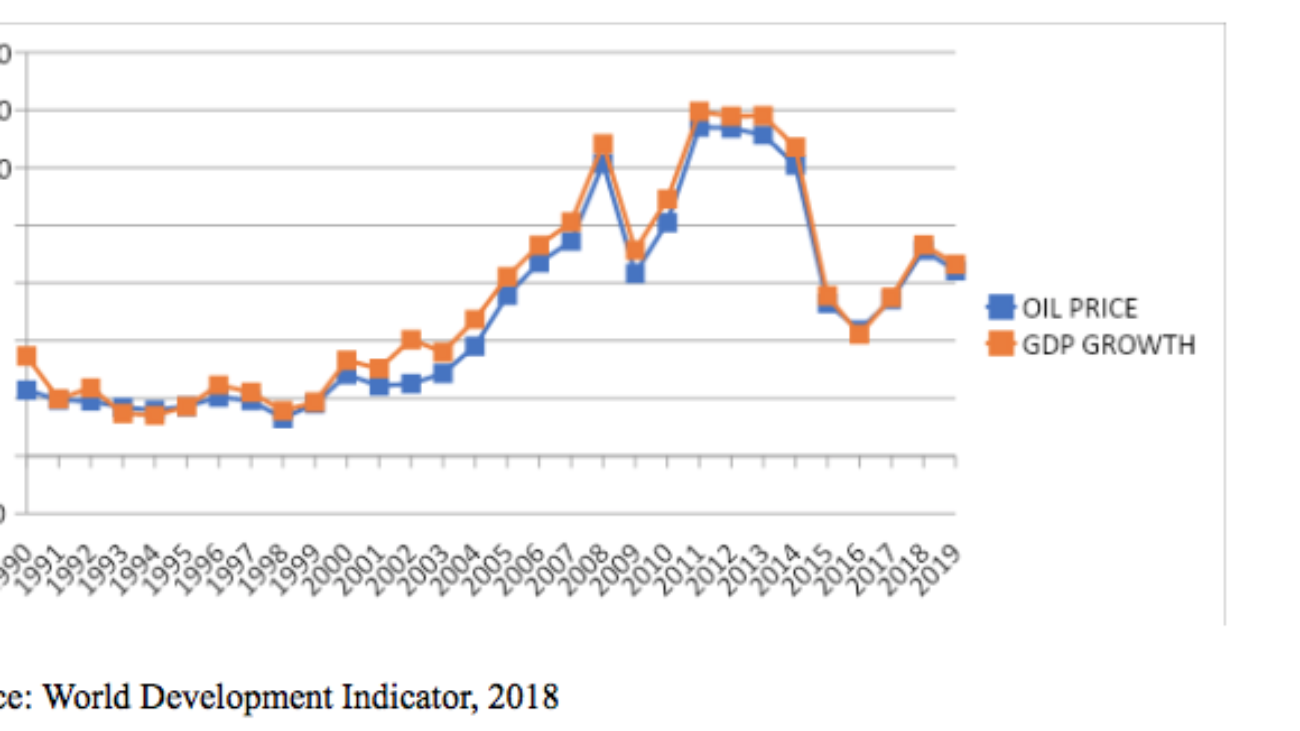

The figure below shows the trend of oil movement and GDP changes in Nigeria from 1990 to 2019. The graph shows that the growth rate of Nigeria and the oil price move together in the same direction. This implies that when oil price increases, the GDP experiences a boom also and when oil price drops, GDP also drops.

Source: World Development Indicator, 2018

This shows that the oil price dictates whether the Nigerian economy grows or not and since the price of oil is determined by factors outside the control of the country, it means Nigeria is at the mercy of whatever happens to oil price.

Nigeria benefited from the rising oil price from the year 2000 to 2007. During this period, oil price increased from $28.42 in 2000 to $74 U.S dollars in 2007. Consequently, the growth rates in Nigeria also show a rising trend.

There was an unexpected drop in oil price in 2014, oil price declined from $100.85 in 2014 to $43.74 in 2016, the growth rate also declined from 6.3 per cent in 2014 to -1.61 per cent sending the economy into a recession.

A recession is characterised by falling GDP, low production/manufacturing activities, rising unemployment, and falling prices of goods and services. Nigeria entered into a recession when the GDP growth rate for the second quarter of 2016 came out negative.

As earlier stated, when the GDP of a country is affected, all other indicators also will perform poorly. For instance, in 2016 when the GDP of Nigeria turned negative, inflation rate rose from 13.9% in the second quarter of 2016 to 14.2% in the last quarter of 2016. By 2017, inflation rose to 18.8% in the third quarter according to data from the National Bureau of Statistics (NBS). When inflation increases, it means the prices of goods and services would increase, hereby creating economic hardship.

The NBS also published data revealing that unemployment rate in Nigeria rose from 12.1% to 13.9% in the first and second quarter in 2016 respectively and by the last quarter of 2016, unemployment rate increased to 14.2%. This shows that oil movement influences the macroeconomic stability of oil dependent countries like Nigeria.

Inflation and unemployment increase during recession because of low economic activities. Firms lay off workers and employ less in order to cover their cost of operation.

The outbreak of the corona virus in 2020 has had severe consequences on the Nigerian economy in the last few months. While Nigeria was still dealing with the pandemic in its early stage, there was a sudden crash in the price of crude oil as a result of the price war between Saudi Arabia and Russia. Oil price which closed at about $60 per barrel as at December 2019 fell to as low as $18 per barrel as at April 2020. This twin shock further weakened the already fragile economy. Inflation rate increased from 12.26 percent in March to 12.34 percent in April, further rising to 12.40 by May and by June it stood a 12.56 per cent according to NBS.

How does oil price movement affects household and businesses in Nigeria?

Consumers and firms are not exempted from the influence of oil price movements. Recall that Nigeria is a major oil exporter and depends largely on crude oil sales for revenue. Therefore, a higher oil price is good news for the economy because export revenue will increase. The increase in revenue means the government is better able to implement its budget whether it’s paying workers’ salaries or implementing capital projects.

Consumers tend to spend more in a period of oil price booms, which is characterised by stable incomes and creation of direct and indirect jobs. Their demand for goods and services tend to rise in this period. The firms on the other hand will benefit from increased consumer spending which translates to higher sales of their products and services.

Conversely, when oil prices decline, there will be a decrease in export revenue and government expenditure. Lower oil prices also put the exchange rate at risk as it exposes the naira to pressure against the dollar. Given that oil exports account for over 80 percent of foreign exchange inflows into Nigeria, a period of low oil prices tends to lead to dollar shortages, naira devaluation and higher inflation. A devaluation of the naira is bad news for households and businesses as it often leads to higher inflation. Many manufacturers rely on imports to produce, so when the exchange rate weakens it means higher production costs for them and that is mostly followed by a hike in the price of the goods they sell which is negative for consumers.

The higher inflation triggered by an exchange rate depreciation squeezes households who are left to contend with lower purchasing power in the face of more expensive goods and services. This implies that households will have less income to spend on goods and services, therefore they will demand less.

The firms will also have less access to funds for investment and could lay off workers in an attempt to cover their operating costs. When firms cut back on expansion, it translates to lower economic growth.

Need for diversification

All the above prove that the Nigerian economy will continue experiencing macro-economic instability until it can find a way to depend less on oil sales for its revenue.

The government will need to invest more in the health and education of the Nigerian citizens. According to the United Nation Children’s Funds (UNICEF) in 2019, there are about 10.5 million out of school children in Nigeria and there are also those who are in school but receive substandard education. Bill Gates, the co-founder of the Bill and Melinda Foundation during his visit to Nigeria in 2018 said the only way Nigeria can escape poverty and enjoy sustained prosperity is by investing in the health and education of the people. He also stated that the life expectancy in Nigeria is one of the worst in the world. ‘‘The most important choice the government can make is to maximize its greatest resources, the Nigerian people. Nigeria will thrive when every Nigeria is able to thrive’’ He said.

The inadequate infrastructure in Nigeria would also make diversification difficult. The World Economic Forum Global Competitiveness Index in 2018 reported that Nigeria ranks 132 out of 137 in the quality of overall infrastructure, 127 out of 137 in quality roads and 136 0ut of 137 in quality of electricity supply. Productivity will only increase when the necessary infrastructure is in place.

The agricultural sector is also a viable sector. The increase in agricultural activities will invariably lead to the development of other sectors that have linkages to the agricultural sector such as the manufacturing and textile industries due to the supply of raw materials from agriculture to feed these industries. The tourism industry is another viable industry that could be harnessed to drive economic diversification since Nigeria is endowed with rich natural ecosystems and cultural diversity.

The telecommunication industry in Nigeria has one of the largest telecoms in Africa. The effective exploitation of this sector will bring about efficiency and productivity in the telecom sector and eventually enhance economic growth.

Again, the need for inter-African trade has been stressed by the World Bank as it says the African Continental Free Trade Area (AfCFTA) could boost regional income by 7 percent or $450 billion, speed up wage growth for women, and lift 30 million people out of extreme poverty by 2035, if implemented fully.

The World Bank said in a new report on Monday.

In addition, experts say the trade pact will position Nigeria’s firm to compete better in the continental and global markets.

AfCFTA represents a major opportunity for countries to boost growth, reduce poverty, and broaden economic inclusion.

The report suggests that achieving these gains will be particularly important given the economic damage caused by the COVID-19 (coronavirus) pandemic, which is expected to cause up to $79 billion in output losses in Africa in 2020. The pandemic has already caused major disruptions to trade across the continent, including in critical goods such as medical supplies and food.

Most of AfCFTA’s income gains are likely to come from measures that cut red tape and simplify customs procedures. Tariff liberalisation accompanied by a reduction in non-tariff barriers—such as quotas and rules of origin—would boost income by 2.4 percent, or about $153 billion.

The remainder—$292 billion—would come from trade-facilitation measures that reduce red tape, lower compliance costs for businesses engaged in trade, and make it easier for African businesses to integrate into global supply chains.

It could be recalled that initially, the Manufacturers Association of Nigeria (MAN) was the biggest opposition to the AfCFTA, arguing that ratifying the agreement could kill industries in Nigeria. MAN had said it was important for Nigeria to position local manufacturers for competitiveness first before ratifying the AfCFTA.

However, the association later made a U-turn, saying African nations needed to trade more with one another.

“MAN recognises the imperativeness of creating a beneficial free trade area for export of the products of members and has strongly worked assiduously to promote the articulation of evidence-based positions on AfCFTA,” Mansur Ahmed, president of MAN, said at a South-West sensitisation workshop in Lagos in February 2020.

The Lagos Chamber of Commerce and Industry (LCCI) is backing the trade deal, arguing that if smaller African countries are not afraid of it, Nigeria with 200 million people and humongous $430 billion GDP, must grab it with both hands.

Muda Yusuf, director-general, LCCI, told BusinessDay in 2019 that multinationals would be the biggest beneficiaries when the AfCFTA started.

“Mostly multinationals and large enterprises are in a better position to gain from AfCFTA because their economies of scale will improve. They have the big market and the capacity,” Yusuf had said.

“The continental trade is more about economies of scale and the amount of what you produce. The higher you produce, the lower the unit cost, which is why small companies will benefit but not as much as large firms,” he further said.

AfCFTA seeks to liberalise trade among African countries. It is targeted at a ‘borderless’ Africa, with an eye on a single market for goods and services on the continent. It was supposed to start in July 1, 2020, but has been postponed to January 2021 owing to COVID-19 pandemic.

Experts believe AfCFTA is easily the largest trade agreement since the World Trade Organisation (WTO) in 1994 and a flagship project of Africa’s Agenda 2063, targeted at creating a single market for 1.2 billion people and exposing each country to a $3.4 trillion market opportunity on the continent.

The AfCFTA is expected to raise Africa’s nominal GDP to $6.7 trillion by 2030 if all the countries sign up.

The treaty liberalises 90 percent of products manufactured in Africa, meaning that a country can only protect 10 percent of its local industries.

Bismark Rewane, CEO, Financial Derivatives, said the AfCFTA would favour Nigeria, Kenya, Egypt and Ghana, among others, but warned that any government that was not effective would fail within the AfCFTA environment.

“Nigeria will benefit. But it will forced to be effective because if not, people can easily go to Cotonou to set up plants,” he told Channels TV in 2019, adding that government failures would be glaring under the trade arrangement.

Over the past 10 years, Nestle Nigeria plc, Dangote Sugar Nigeria plc, and Guaranty Trust Bank have generated more profit from their shareholders investments than peers as evidenced in the consistent and superior return on equity, according to a recent report by Coronation Asset Management, titled ‘Navigating the Capital Market: the Investor’s Dilemma’.

The report studies the impact of the macroeconomic environment on earnings and valuations of Nigerian Stock Exchange (NSE) listed companies, and also beams its searchlight on investment returns, short-term government securities and inflations.

The return on equity (ROE) indicates how effective management is at using equity financing to fund operations and grow the company.

Over the past decade, companies have been operating in an unpredictable macroeconomic environment characterised by currency devaluation, deteriorating infrastructure, inflationary pressure, and volatility in oil price.

Some sectors have not recovered from the sharp drop in crude oil price of mid-2014 that stoked severe dollar scarcity and consequently tipped the country in its first recession in 25 years.

According to Coronation Research, GTBank, the largest lender by market value, had superior and consistent ROE in the last 10 years, which means it is a worthwhile investment.

The lender’s returns have been consistently higher in the benchmark Fair Value Equity Return (FVER), a parameter the investment house uses to gauge the efficient and profitability of an entity.

The analysis of the 2019 financial statement of top tier banks shows GTBank recorded ROE of 28.64 percent, which compares to Zenith Bank (24.80%); Access Bank (15.98%), and United Bank for Africa (14.90%).

Coronation Research, however, says the good news is that the trend (FVER) has been moving upwards.

For instance, Zenith Bank has joined GTBank as a strong performer (i.e. its RoE exceeds the FVER) over the past three years, while Access Bank joined this fortunate group last year.

The report observes that among the pure-play food manufacturing companies there is the remarkable exception of Nestle Nigeria, which has recorded an average RoE of 74 percent over the past 10 years.

Analysts at Coronation Research attribute the success of the consumer goods giant to its product portfolio that has won consistent loyalty from Nigerian consumers; its operating margins have been high and consistent, thanks to a high degree of local sourcing; it pays almost all its Net Profits as dividends, keeping its equity level low.

The analysts say majority of Nigerian listed companies do not return what they consider an adequate – 20.53 percetn – RoE; but they add that there are notable exceptions and several bank stocks deliver returns above this level, while other bank stocks are trending towards this level.

The report notes that many industrial companies have reported steeply declining returns over the past 10 years, disappointing a generation of investors in Nigerian industry.

Interestingly, the listed brewers are hardest hit from the economic downturn as ROEs of two out of the three dominant players in the industry have been declining in the last 10 years.

Aside macroeconomic uncertainties, the brewery industry was reeling from stiff competition; this happened when International Breweries launched top brands into the market in 2013. Peer rivals found it practically difficult to grow revenue.

The Fast Goods Consumer Goods Companies (FMCGs) have seen operating margins deteriorate due to hike in utilities and spiralling inflation that erodes the purchasing power of consumers. Because they had hiked the price of product in 2017 to compensate for rising production cost caused by dollar scarcity, it would be practically difficult for them to pass rising cost to beleaguered consumers in form of higher price.

The coronavirus pandemic that ravaged economies across the globe and disrupted the demand and supply side of the market, as government imposed lockdown policies, has dealt a great blow to the industry.

The earnings seasons have kicked off, showing play food companies that have released half-year results falling off the cliff.

Coronation Research notes that many companies with high shareholder returns have failed to deliver stock price returns of the same order.

“This is because the market has been de-rating these stocks, over time paying lower and lower multiples for their earnings. We cite several bank stocks as examples,” notes the report.

To shareholders who have invested in an entity with cash that would have been deployed in other investments, profit is the only thing to them.

Investors’ apathy towards the Nigerian equity market has heightened as they have been dumping shares due to lack of policy direction on the part of President Muhammadu Buhari-led government and poor macroeconomic indices.

The crash in oil price due to the coronavirus pandemic and rift between Saudi Arabia and Russia have elicited stock market rout as sentiments towards the equity market weakened to a record low.

In all, the All Share Index closed H1-2020 (July 24) at 24,474.62pts, with YTD loss pegged at 8.18 percent.

As a lot of Nigerian businesses tap the low-interest environment to ramp up borrowing to offset liquidity challenges fuelled by the effect of COVID-19, there’s a growing worry that the risk of low economic growth is going to constrain future revenues and increase the burden of debt servicing for firms.

In an economy hit by a double challenge of COVID-19 and collapsing oil price, slow economic activities, declining revenue, job losses and dampened purchasing power are expected to affect the bottom line of most companies and, even worse, make many handicapped to repay their debt.

Ayorinde Akinloye, a research analyst at CSL Stockbrokers, said the biggest risk for many companies would be the inability to generate adequate cash flow to pay back on maturity because of the slowdown in business.

“It is not about having funds, it’s about if there is demand. What use is producing when you cannot sell?” Akinloye asked.

Andrew S. Nevin, partner and chief economist at PwC, said “the economic impact of Covid–19 is just starting”.

“The reality is, we are now seeing the impact down the line in various industries,” Nevin said. “For us in Nigeria, it’s going to be hard to get our economy restored to normal without regretting the trade ties and investment from groups around the world, but that still looks a long way off.“

He said companies and government at all levels need to prepare for a long period of difficult economic times.

Due to the high liquidity challenges of most Nigerian companies amid the decline in business activities, about 27 firms issued commercial papers, bonds and rights issues in the first six months of 2020, as compiled from FMDQ data.

While Nigerian companies took advantage of the low-interest rate environment to raise capital, corporates most preferred the short–term commercial paper (CP) to bonds and rights issue due to the low cost of finance and the short maturity period, according to BusinessDay analysis.

Out of a total of N658.5 billion debt issued in the first half of 2020, commercial papers accounted for 70.86 percent as against the 23.95 percent raised through corporate bonds and 5.19 percent rights issue.

“It presents an opportunity for companies to raise cheap capital and those that have existing bonds raised some two or three years ago when rates were about 15-18 percent can call the bond,” said Yinka Ademuwagun, research analyst at United Capital.

While interest rates in Nigeria have always been high due to the monetary system in vogue since 2009 which sought to use FGN bonds/T-bills and OMO bills as means of attracting US dollars into the country to stabilise the naira, the recent OMO policy by the Central Bank (CBN) which prevents domestic investors from participating in the auction is the key driver of the low interest enjoyed today.

Yields on both T-bills and bonds instruments have hit a bottom record from a double interest rate enjoyed some four years ago, and according to industry analysts, the low yield environment is an opportunity ready to be tapped.

“The current state of the economy will affect the revenue stream of companies, and that is even the reason why they are raising funds because Covid-19 was a shock,” Ademuwagun said, projecting the Covid-19 shock to be short term.

According to ‘Covid-19: A Business Impact Series’, an advisory from KMPG business leaders, effective cash flow management is likely to be critical for many organisations during Covid-19 period as revenues fall and potentially, debtors delay payments or become insolvent.

In what could better describe the pains felt by the businesses due to the pandemic, consumer goods giant, Unilever, reported an underwhelming performance in the first half of the year, after its revenue plunged by more than 40 percent to N14 billion, compared to the N23.4 billion it reported the same period last year.

Across key product segments, revenue declined as both the food and home/personal care (HPC) businesses were down 28.5 percent and 43.3 percent, respectively, to N15.3bn and N12.1bn in H1 2020 from N21.4bn and N21.3bn, a pointer to how the pandemic has dealt a blow to the cash flows of businesses.

Similarly, revenues of Cadbury Nigeria declined by 18.2 percent to N15.9bn in the first half of 2020, from a high of N19.5bn the same period last year.

To at least tame the impact of the crisis on their businesses, many companies, particularly those in the fast-moving consumer goods space, have increased their books of trade receivables, giving stock of goods on credit to customers with the hope they would pay back at a later date after the goods are sold.

Irrespective, the move still doesn’t hold much water due to weak purchasing power of consumers whom the goods are meant to be sold to, thereby resulting in increasing firms’ books on goods returned inwards.

For Unilever, its impairment loss on trade receivables surged by more than 3,000 percent, from N17.4 million in June 2019 to N597.2 million.

More than 35,640 customers of Nigerian banks have restructured loans worth N7.8 trillion after the pandemic crippled business activities, Godwin Emefiele, CBN governor, said during the apex bank’s July Monetary Policy Committee meeting where members voted to leave benchmark interest rate and other key parameters unchanged.

Emiefele said that plans were underway to expand the forbearance levels for businesses, particularly those hard–hit by the impact of the virus, to as much as 65 percent.

This, however, might still not be enough to get the fundamentals of these businesses to their pre-pandemic levels, according to analysts who spoke to BusinessDay.

To a large extent, the success or failure of businesses mirrors macroeconomic realities of a country. When businesses thrive, there appears to be economic prosperity in a country, and vice versa.

For Africa’s largest economy which for a larger part of the last five years has suffered stunted economic growth at an average of 2 percent, the scenario appears not different.

Since 2017 when oil-dependent Nigeria emerged from its economic recession, not only has the country’s economic growth been sluggish but only a few sectors triggered the expansion, further undermining the country’s capacity to create enough jobs to meet the growing number of labour market entrants.

Africa’s top oil exporter which relies on crude sales for around 90 percent of foreign exchange earnings and more than half of government revenue is projected to post as much as 5 percent contraction in 2020.

Analysts recommend government intervention in key sectors of the economy and right policy implementation as some of the stimuli needed to bail Africa’s largest economy from posting its worst recession in decades.

But Nigeria’s planned fiscal and monetary policy stimulus targeted at addressing the economic challenges of Covid-19 are modest compared to its peers, according to the World Bank.

As a share of its 2018 GDP, Nigeria’s Covid-19 stimulus – whether as aid, grants, guarantees, CBN’s monetary liquidity injection, or interest rate – is less than that of Brazil, Angola, Mexico, Russia, South Africa, Ethiopia, Ghana, Kenya, Senegal, and Uganda, the Washington-based lender said in its recent Nigeria Development Update (NDU) report.

“Nigeria’s fiscal and monetary policy response has been modest by the standards of comparable countries, making it harder for the country to avoid recession,” the World Bank said in the report titled ‘Nigeria in Times of COVID-19: Laying Foundations for a Strong Recovery’.

The World Bank explained that the current challenges reflect long–standing shortfalls in human capital, infrastructure and public services, women’s economic inclusion, the business environment, access to finance, and governance.

Nigeria’s goal of ensuring 80 percent of Nigerian adults have access to financial services by the end of 2020 may no longer be visible as a result of the COVID-19 pandemic, which has adversely affected the revenue of many households and businesses.

However, stakeholders say collaboration may be the only opportunity the Central Bank of Nigeria (CBN) has to achieve the target, given the time left in 2020.

The stakeholders, who include the CBN, Mastercard, Carbon, MTN Nigeria, VerifyMe and Acumen, on Thursday, participated in BusinessDay Digital Dialogue Series with special focus on ‘Future of Payment and Financial Inclusion.’

As of July 23, Nigeria had 38,344 confirmed COVID-19 cases, 813 deaths and 15,815 people recovered. While the number continues to rise, the economic impact has been very devastating for many people and businesses. By April when the government began to enforce a nationwide lockdown, many online lenders said they were expecting massive defaults, a signal that all was not well with the majority of adults who had access to financial services.

But it was already predicted in a report by the Enhancing Financial Innovation and Access (EFInA), the organisation that conducts biennial reports on Nigeria’s financial inclusion industry. EFInA had noted at the beginning of the year that while more people became financially included between 2016 and 2018, it was not at the same pace with population growth rate. The COVID-19 has now exacerbated the situation, as experts note that much of the current 63.2 percent of the population with access to financial services have fallen behind.

Paul Oluikpe, associate head, Financial Inclusion Secretariat, CBN, says the current financial inclusion figures are being put together by EFInA and is likely to show that many people have fallen through the cracks in huge proportions as a result of the COVID-19 pandemic.

The bank also conducted a survey in which it found out that payment adoption was currently at 40 percent, savings at 24 percent, credit at 2 percent; pensions at 2 percent, insurance at 2 percent and financial exclusion at 36.8 percent, meaning that Nigeria is way behind other countries in financial inclusion.

“Hence, we have a -16 to -18 percent chance in reducing exclusion to 20 percent by 2025,” Oluikpe states. But the CBN says its agent programme, SANEF, is growing with about 350,000 agents added, with plans to increase the number to 500,000 already on.

The CBN however acknowledges that achieving the target is of great importance, as the cost of managing cash is very expensive and at the expense of the economy. Thus, in recent times it has increased its efforts to deepen its cashless policy.

In 2019, the apex bank granted Approval In Principle for Payment Service Bank licences to three organisations – Glomobile, 9Mobile and Unified Payments. MTN Nigeria on the other hand got a Super Agent Licence. The CBN has, however, withheld the PSB licence that would see telcos fully involved in offering financial services.

While many analysts have said the pace of financial inclusion could significantly improve with telcos’ full involvement in financial services, the CBN can also benefit from other collaborations. Elsa Muzzolini, general manager, commercials, Mobile Financial Services, MTN Nigeria, notes that there is more telcos can offer the sector.

“As part of the journey to achieving financial inclusion for all, I think we can do so much through collaboration and partnership with players in the fintech and the banking space, and as the number one telecommunications service provider in the country, that is core to our operations,” Muzzolini says.

Beyond telcos, the collaboration is starting to include non-bank financial services providers like Mastercard, which has a vast footprint of providing financial inclusion across the world. “5 years ago, we committed to bringing 500 million financially excluded individuals into the digital economy,” Ebehijie Momoh, senior vice president, Mastercard West Africa, states, noting, “We achieved that goal and are focused on bringing in a total of 1 billion individuals by 2025.”

Mastercard developed and implemented solutions that make it easier and more convenient for people to use alternative means of payment instead of cash. Momoh says collaboration with the government is critical as it would enable innovation.

Financial inclusion is also attracting impact investors who are identifying innovative start-ups providing financial services to the grassroots.

Meghan Curran, West Africa director, Acumen, says impact investing can help identify innovative business models and ways to create access to financial services. Acumen has provided funding to Nigerian fintech start-up Paga twice.

“Identity management enables fintech and is a key pillar to financial inclusion,” Esigie Aguele, CEO of VerifyMe, saying, “We are committed to working with the government to digitize Nigerians.”

The figures only refer to their annual remunerations as the highest-paid directors.

The responsibility of piloting a firm’s affairs and ensuring profitability often rests squarely on the shoulders of the Chief Executive Officer (CEO). Agreed, running a company is never a task that can be accomplished by just one person. But that notwithstanding, CEOs are the ones at the helm of affairs. As such, they take most of the blame for the lows, just as much as they take the credit for the highs.

It goes without saying that CEOs are also the highest-paid staff of every company. In Nigeria, the CEOs of the major companies are remunerated handsomely for their efforts. However, just as much as these companies have ranks in terms of asset size and profitability, so also do their CEOs’ earnings have ranks.

This article, therefore, looks at the highest-paid CEOs of companies listed on the Nigerian Stock Exchange. The focus here is on how much they earned in 2019.

Do note that the figures given here do not include what the CEOs might earn in dividends as shareholders of their respective companies. The figures only refer to their annual remunerations (executive compensation) as the highest-paid directors.

Ferdinand Moolman

Ferdinand Moolman, MTN Nigeria, N586 million

Ferdinand Moolman is Chief Executive Officer (CEO) of one of Nigeria’s biggest, non-oil foreign direct investment – MTN Nigeria Communications Plc. He was promoted to the position of CEO on December 1, 2015, as part of a major reshuffling of the telco’s operating structure which was aimed at strengthening operational oversight, leadership, governance, and regulatory compliance.

Before then, he was the Chief Financial Officer (CFO), a position he occupied immediately he was transferred from MTN Iran cell where he was the Chief Operating Officer (COO).

It makes a lot of sense that the CEO of the biggest company listed on the Nigerian bourse should be the highest-paid CEO in Nigeria.

Moolman earned N586 million in 2019, 2.5% up from the N571 million he took home in 2018.

Austin Avuru

Austin Avuru, Seplat, N440 million

Augustine Avuru, the co-founder and CEO of Seplat Petroleum Development Company Plc, is the highest-paid director in his company, and second highest in Nigeria for the year 2019.

Prior to becoming the Chief Executive Officer of Seplat in May 2010, he was Managing Director at Platform Petroleum Limited, a company he founded. He had spent over a decade at Nigerian National Petroleum Commission (NNPC), holding different positions including that of wellsite geologist, production seismologist, and reservoir engineer.

He had also worked as an exploration manager and technical manager with Allied Energy Resources in Nigeria, a pioneer deepwater operator, where he spent ten years before starting Platform Petroleum Limited in 2002. He is also a director of MPI, which is listed on NYSE Euronext Paris.

Avuru received N440 million as his remuneration in 2019, a shortfall of N44 million when compared to his 2018 earnings.

Recall that Seplat had announced Roger Brown as the incoming CEO that will take over when Avuru retires on July 31, 2020.

Segun Agbaje

Segun Agbaje, GTBank, N400 million

Segun Agbaje joined Guaranty Trust Bank as a pioneer staff in 1991 and rose through the ranks to become the Managing Director and Chief Executive Officer in 2011 after Tayo Aderinokun, the previous CEO, passed on.

As CEO, Agbaje took N400 million home in remunerations for the year 2019. This shows an increase of N16 million from his N384 million remuneration in 2018, and given the impressive results that the bank showed for the year, we can say that it was duly justified.

He was recently elected an independent member of the Board of PepsiCo, the American owners of popular beverage drinks Pepsi and Moutain Dew. As Nairametrics reported, Agbaje will officially assume his duties as a board member and audit committee member at PepsiCo by mid-July.

Yaw Nsarkoh

Yaw Nsarkoh, formerly with Unilever Nigeria Plc, N330 million

Yaw Nsarkoh has had a long career within the Unilever Group, occupying top positions like the African Regional Brand Manager, Production Manager for Unilever Ghana, among others.

He headed several regional headquarters of the global manufacturing company, especially in Africa. He also served as a Strategic Assistant to Unilever’s President for Asia, Africa, Central, and Eastern Europe.

He resigned from his position as Managing Director in December 2019, to take up new roles within the Unilever group across Europe. He was succeeded by Carl Raymond Cruz in January 2020. Prior to his departure, he earned N303 million in 2019, 8% less than the N330 million he earned in 2018.

Michael Puchercos

Michael Puchercos, formerly with Lafarge Africa Plc, N272 million

For the financial year ended December 31st, 2019, Michael Puchercos earned N272 million, marking an 18.7% increase when compared to the N229 million he earned in 2018.

Before his appointment as Lafarge Africa Plc’s CEO, he worked in various capacities within the cement industry for two decades. He was the President & Chief Executive Officer of Lafarge Halla Cement; Director of Strategy and Systems at Lafarge Gypsum; Chief Executive Officer of Bamburi Cement and Hima Cement; and Chairman of Mbeya Cement in Tanzania.

He resigned from Lafarge in January 2020 to join competitor brand, Dangote Cement Plc and was succeeded by Mr. Khaled Abdelaziz El Dokani, the former country CEO of Lafarge Holcim Iraq.

CEO, Nigerian Breweries Plc, Jordi Borrut Bel

Jordi Borrut Bel, Nigerian Breweries Plc, N271 million

Jordi Borrut Bel is the Chief Executive Officer and Managing Director of Nigerian Breweries Plc. Mr Bel is an experienced manager and has served in Heineken’s different subsidiaries across different countries. He was Managing Director at Brarudii SA, Manager-Project Distribution at Heineken Slovensko AS, Brand Manager at Heineken France SAS and Director-Sales & Distribution at Heineken España SA. His last position prior to coming to Nigerian was that of the Managing Director of Heineken Burundi.

Bel’s earnings experienced a quantum leap from N190 million in 2018 to N271 million in 2019, an increase of about 42%. He was the sixth highest-paid CEO in 2019.

Mauricio Alarcon – CEO Nestle Nigeria

Mauricio Alarcon, Nestle Nigeria Plc, N218 million

Seventh on the list is Mauricio Alarcon, the Chief Executive Officer of Nestle Nigeria Plc. Alarcon was appointed CEO in 2016, after a progressive 17 years career with the Nestle brand. He started as Area Sales Manager with Nestle Mexico and later became a Senior Brand Manager.

He worked as Marketing Advisor at Nestle Headquarters in Switzerland, Country Manager at Nestle Cote d’Ivoire and later became Managing Director of Nestle Atlantic Cluster between June 2016 and September 2016, overseeing Senegal, the Gambia, Guinea, and Cote d’Ivoire.

Alarcon earned N218 million in 2019, a slight increase from the N210 million in 2018 he earned in 2018, placing him 7th place in the list.

Lars Richter – CEO Julius Berger Nigeria Plc

Lars Richter, Julius Berger Nigeria Plc, N217 million

Presently, Lars Richter occupies the position of Managing Director & Director at Julius Berger Nigeria Plc, a position he was appointed to in 2018.

Before this appointment, he had garnered over 16 years’ experience in the construction industry, with 10 years spent in Nigeria, in different positions including Division manager, Project manager, and Project engineer.

Richter places 8th on this list, with an income of N217 million in 2019. This is quite a significant reduction from the N319 million he received in 2018 although there is no obvious justification for this.

Emeka Emuwa – CEO Union Bank of Nigeria

Emeka Emuwa, Union Bank of Nigeria, N172 million

Emuwa earned an annual net income of N172 million in 2019, the same as he did in 2018. He was appointed CEO of Union Bank of Nigeria in November 2012, after a progressive 25-year banking career at CitiBank across several African countries.

He started out as a Management Assistant at Citibank Nigeria Limited and was later promoted to the position of Country Head, Cameroon. At this time, he was also overseeing all the bank’s activities in the Central African region, including Congo and Gabon.

He occupied strategic positions in the company across several countries like Tanzania, Ghana, Niger, and Nigeria, serving as the CEO between 2005 and 2012, before he took up the appointment with Union Bank Plc.

Imrane Barry, Total Nigeria Plc

Imrane Barry, Total Nigeria Plc, N163 million

Total Nigeria Plc has Imrane Barry as its Managing Director. Imrane is not new to the Total group as he had previously served as Managing Director of Total Uganda in 2013, Total Cameroon SA in 2015 and Total Nigeria Plc in 2018. He also worked with other Total affiliates in Kenya and Ivory Coast, at SEP-Congo as the Technical and Transport Director, and in Paris as the Strategy and Development Senior Officer.

He was appointed Deputy Executive Vice-President of Total Africa & Middle East in 2012,

Before joining Total, Imrane worked in several capacities in Engineering and Construction Companies in Guinea Conakry, Cote d’Ivoire and Gabon.

Imrane took home N163 million as remunerations in 2019, 41% more than his 2018 earnings of N115 million.

Note that these figures were sourced from the companies’ FY 2019 audited financial statement. As such, the figures represent these CEOs’ income for the year 2019. As was explained in the article, a couple of the CEOs no longer occupy their positions, but since there has not been a full year financial statement explaining what their successors might be earning, these figures are the most recent.